Centurion Built a REIT. Now It Sells the Engine.

Centurion (SGX:OU8) at S$1.46 prices a dormitory operator. The CAREIT IPO turned it into a three-pillar living-sector platform. The market hasn't caught up.

Short-form deep dive, distilled analysis, ~15 mins read

On 25 September 2025, a small Singapore-listed dormitory operator did something unusual. It took fourteen of its best-stabilised assets, dropped them into a newly constituted real estate investment trust, and listed that trust on the same exchange where the parent had been trading for two decades. Centurion Accommodation REIT (SGX:8C8U) began trading at S$0.88 a unit. Centurion Corporation Limited (SGX:OU8), the sponsor, retained 42.9% of the new trust, kept full ownership of the trust's manager, and pocketed approximately S$520 million in cash for the assets it had handed over.

Eight months later, the trust is up. The sponsor’s share price is up. Both are up less than they should be if the market understood what just happened.

The easy version of this story is that Centurion’s share price has rallied from S$0.96 at the start of 2025 to S$1.46 at the 16 May 2026 close, a 52% move, and that the rally exhausted the mispricing. We disagree. The rally was the market crediting Centurion for executing the listing. It was not the market repricing what the listing structurally created: a Singapore-listed dormitory operator that now earns three streams of recurring income from one corporate vehicle, owns a directly-held bed count larger than the trust it sponsors, and still trades at 1.0x book and 11x trailing earnings, as if none of that had happened.

The rally was also not a smooth march upward. The market’s initial reading of the CAREIT IPO was bearish for the sponsor: OU8 drifted from S$1.50 in late September 2025 to roughly S$1.34 by late October 2025, even as CAREIT itself rose 16% from its S$0.88 issue price to S$1.02 in its first week of trading. The bear interpretation was straightforward — the best-occupancy assets had been carved out into CAREIT (the Initial Portfolio’s Singapore PBWA assets ran at 99.2% occupancy in FY2024 versus 94.0% for the broader sponsor group), leaving Centurion holding the residual lower-occupancy and ramping properties. Two things contradicted that read. Joint Chairman Han Seng Juan personally bought 300,000 OU8 shares at an average S$1.46 across 29 and 30 September 2025 — the family was buying, in size, into the drawdown. And the operating results since have vindicated the buyers: CAREIT beat its IPO forecast on every metric in its first reporting period, and Centurion’s own 1Q 2026 revenue rose 30% year on year. The asset-quality-dilution fear did not show up in the numbers. The recovery to S$1.46 since is partial credit for what the listing structurally created — but only partial.

We ran the look-through arithmetic on Centurion at the 16 May 2026 closing price of S$1.46. The sum of its three pillars, the directly-held portfolio of c.53,000 beds, the asset-management business running CAREIT, and the 42.9% unitholding in CAREIT itself, produces a fair value materially above the market price. The full numerical verdict, the segment-by-segment fair-value build, the forward earnings model, and the probability-weighted implied value are the subject of a companion institutional-length analysis published separately. Link below.

From one dormitory to three continents

Centurion as we know it today began in 2011, when a small Singapore-listed media-and-optical-storage company called SM Summit Holdings was reverse-acquired by Centurion Properties, a private vehicle controlled by two maternal cousins, Loh Kim Kang David and Han Seng Juan. Loh and Han had built their wealth in Singapore stockbroking, both spending years at UOB Kay Hian, both with stints at Hong Kong subsidiaries. The reverse takeover gave them a listed shell. What they put into it was a single purpose-built worker dormitory in Toh Guan, Singapore, with 5,300 beds.

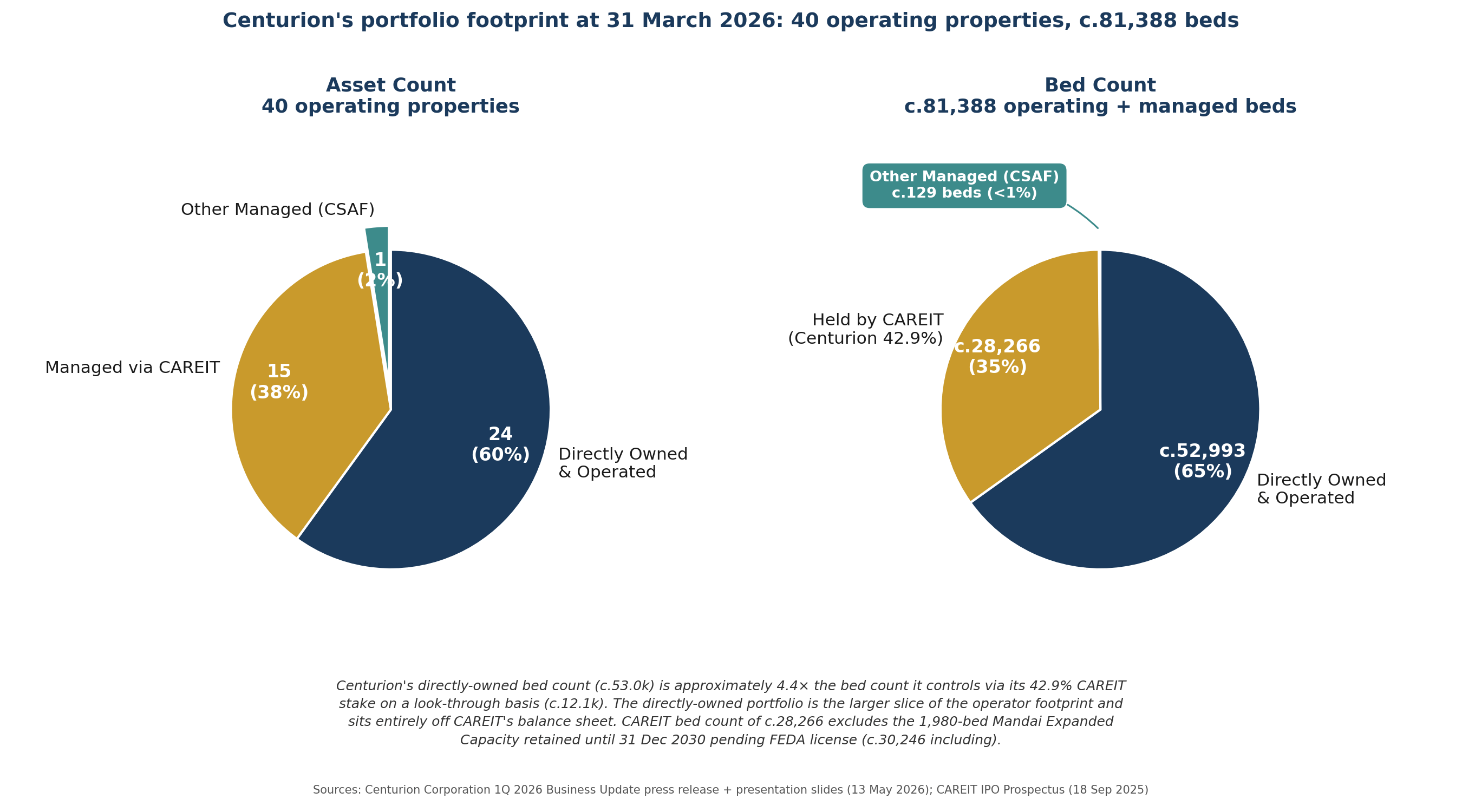

Fifteen years later, the portfolio is materially larger. As at 30 June 2025, before the CAREIT spin-off, the Centurion sponsor group held 70,291 beds across 37 operating purpose-built accommodation assets, comprising 65,390 beds of purpose-built worker accommodation, 4,501 beds of purpose-built student accommodation, and 400 build-to-rent apartments. By 31 March 2026, after the CAREIT spin-off and a subsequent quarter of portfolio activity, Centurion’s directly-owned operating portfolio stood at 24 assets with c.52,993 beds per the 1Q 2026 Business Update (5 Singapore PBWA, 13 Malaysia PBWA, 1 Hong Kong PBWA, 2 Hong Kong PBSA, 1 Australia PBSA, 1 UK PBSA, and 1 Xiamen BTR), complemented by 16 managed assets with c.28,395 beds (CAREIT’s 15 plus Castle Gate Haus in the Centurion Student Accommodation Fund). The geographic spread went from Singapore-only to Singapore, Malaysia, Australia, the United Kingdom, Hong Kong SAR, and China.

A note on jargon before we continue. Centurion operates in two distinct accommodation segments and we will use the industry shorthand throughout: PBWA stands for purpose-built worker accommodation, the formal name for the licensed dormitories that house migrant construction, marine, and industrial workers (in Singapore, in Malaysia, and now in Western Australia for resource-sector workers). PBSA stands for purpose-built student accommodation, the formal name for the private-sector student housing typically located near universities (in Centurion's case, the United Kingdom, Australia, and Hong Kong). The third segment, build-to-rent (BTR) apartments, is a smaller category covering longer-stay rental housing for working professionals (Centurion's Xiamen property).

The inflection points were structural. In 2014, Centurion entered the United Kingdom PBSA market through the Dwell Student Living brand. In 2017, it added US student housing through a private fund structure. In 2020, the COVID-19 pandemic and the well-publicised migrant-worker dormitory outbreak forced a wholesale reset of Singapore's PBWA regulatory framework: the Foreign Employee Dormitories Act licensing regime, the Improved Dormitory Standards, and ultimately the New Dormitory Standards that will apply to all Singapore PBWAs by 2040. Centurion responded by buying or building NDS-compliant capacity early. Westlite Ubi became operational in December 2024 as the first fully NDS-compliant Centurion dormitory in Singapore. New blocks at Westlite Toh Guan (1,764 beds) and Westlite Mandai (3,696 beds) obtained their temporary occupation permits in October 2025 and January 2026 respectively.

Then in 2025, the largest single move. On 7 January 2025, the company announced it was exploring the establishment of a REIT. Listing application went in by July. Cornerstone book closed with sixteen institutional investors. The IPO was oversubscribed by 30 times on the public tranche and 16 times overall. CAREIT began trading on 25 September 2025 at S$0.88 a unit, with Centurion as sponsor and Centurion Asset Management Pte Ltd, a wholly-owned subsidiary, as manager. Fourteen assets were spun in: five Singapore PBWAs, eight United Kingdom PBSAs in the Dwell portfolio, and one Australian PBSA. The forward purchase of EPIISOD Macquarie Park in Sydney completed in January 2026 for A$345 million, taking CAREIT's portfolio to 15 assets and c.28,266 operational beds at 31 March 2026 per the 1Q 2026 Business Update (or c.30,246 including the 1,980-bed Mandai Expanded Capacity retained until 31 December 2030 pending FEDA license).

What remained at Centurion is the larger portfolio — 24 directly-held operating assets totalling 52,993 beds at 31 March 2026, spanning six markets:

Singapore PBWA — 5 assets, 15,156 beds (ASPRI-Westlite Papan plus four Westlite Quick-Build Dormitories)

Malaysia PBWA — 13 assets, 36,006 beds (eight long-standing Westlite properties plus five Harum Megah-rebranded assets acquired September 2025)

Hong Kong — 3 assets, 653 beds (Westlite Sheung Shui PBWA; Dwell Prince Edward and Dwell Ho Man Tin PBSAs)

Australia PBSA — 1 asset, 597 beds (Dwell Village Melbourne City)

United Kingdom PBSA — 1 asset, 181 beds (Dwell Garth Heads, Newcastle)

China BTR — 1 asset, 400 apartments (Centurion-Cityhome Gaolin, Xiamen)

Two Australian Key Worker Accommodation assets added in April 2026 (Karratha and South Hedland, 446 beds combined) take the post-1Q snapshot to c.26 assets and c.53,439 beds. The US PBSA assets were disposed in March 2026, completing Centurion’s exit from the United States. A c.7,000-bed PBWA development at Nusajaya, Iskandar, Johor is under exploration with NS Corp and is not yet operational. Westlite Toh Guan and Westlite Mandai sit inside CAREIT and are addressed under Pillar 3 below.

The shape of the business changed. Pre-September 2025, Centurion was an operator. Post-September 2025, Centurion is an operator, an asset manager, a property manager, and the largest unitholder in a separately-listed REIT. The strategy that took fifteen years to build did not change in 2025. What changed is the form in which it monetises.

What Centurion actually is now

The consolidated financial statements obscure the structure, and the structure is the point.

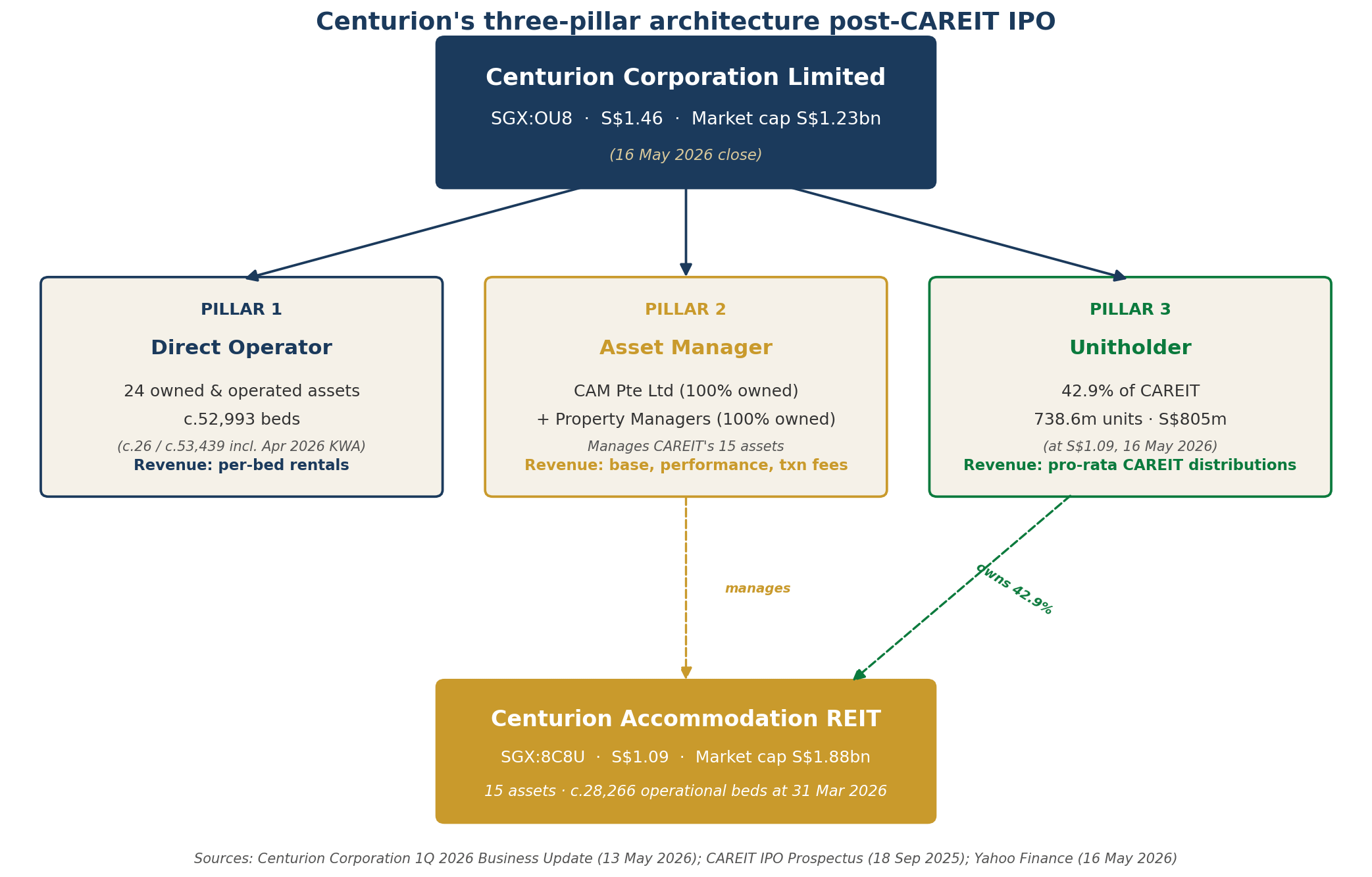

Centurion Corporation owns three things operationally. The first is the 24-asset directly-owned portfolio described above, totalling c.52,993 beds at 31 March 2026 (c.26 / c.53,439 including the April 2026 Australian additions), generating operating revenue from per-bed rentals. The second is the asset-management business, comprising Centurion Asset Management Pte Ltd (100% owned, manager of CAREIT) and the property management companies (100% owned, contracted property managers for CAREIT and increasingly for third-party owners). The third is a 42.9% unitholding in CAREIT itself, the SGX-listed REIT that Centurion sponsored.

The market’s mental model of Centurion is often that “CAREIT is the main business now; OU8 is the leftover holding company.” The bed-count picture is precisely the opposite. Of the c.81,388 operational beds in Centurion’s universe at 31 March 2026, 52,993 (65%) are directly owned and operated by Centurion, 28,266 (35%) are held in CAREIT (and Centurion owns 42.9% of those, equivalent to c.12,124 beds on a look-through basis), and 129 (<1%) sit in CSAF (Castle Gate Haus, Newcastle). A further c.3,548 beds across Singapore are under third-party property management agreements. CAREIT is the high-quality, stabilised, externally-financed slice. Centurion is the larger, broader, more diversified, and faster-growing whole.

These three pieces generate three flavours of income. The directly-owned portfolio produces operating profit. The asset-management business produces recurring fee income (base manager fee, performance fee, acquisition and divestment fees, property manager fees). The CAREIT unitholding produces investment income (Centurion’s 42.9% pro-rata share of CAREIT’s distributions). All three flow through Centurion’s consolidated income statement. But here is where it gets technical: CAREIT itself is consolidated into Centurion’s accounts, not just equity-accounted, because Centurion controls CAREIT through its 100% ownership of the manager. So 100% of CAREIT’s revenue appears on Centurion’s revenue line, 57.1% of CAREIT’s profit gets stripped out at the non-controlling interest line, and what remains at the bottom is Centurion’s economic share.

The non-controlling interest line on Centurion's balance sheet tells the story. At end-FY2024, NCI was S$82.9 million. At end-FY2025, three months after the CAREIT listing, NCI was S$939.7 million. That is a more than tenfold jump in a single year, reflecting the 57.1% of CAREIT's net assets attributable to non-Centurion unitholders that now sits inside Centurion's consolidated balance sheet.

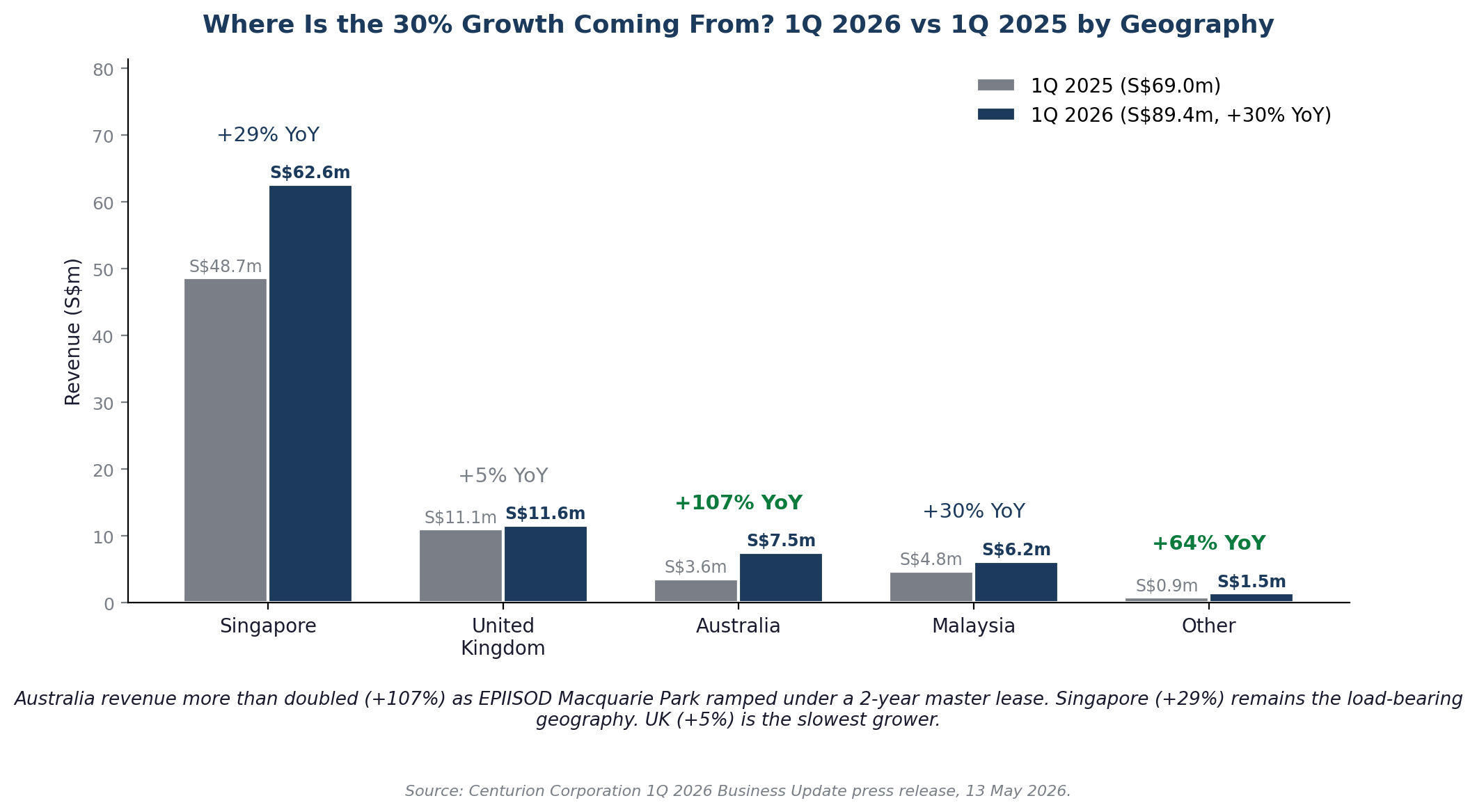

Centurion's reported FY2025 revenue rose 17% to S$295.9 million. FY2026 is set to land materially higher, driven by five incremental items: Westlite Mandai's transition from equity-accounted associate to fully consolidated via CAREIT (the largest single contributor); the new Mandai block running for a full year; EPIISOD Macquarie Park's master-lease income for a full year; the Harum Megah Malaysian portfolio's first full year; and the two Australian Key Worker Accommodation assets for a partial year — offset by the US PBSA disposal. Putting these together, FY2026 consolidated revenue should land between approximately S$355 million and S$390 million (+20% to +32% YoY). The 1Q 2026 print of S$89.4 million annualises to about S$358 million, the lower end of this range before EPIISOD and the April 2026 Australian additions ramp into the full-year run-rate. The market sees the +17% FY2025 print and reads it as the steady-state run-rate; the FY2026 print is set up to land considerably higher.

A casual reader of the FY2025 press release sees revenue +17%, net profit -63%, EPS -67%, and concludes Centurion is in trouble. The actual story is that the FY2024 IFRS net profit was inflated by a S$219 million fair value gain on the Singapore PBWA portfolio that did not recur, while core profit (excluding fair value movements and one-off transaction costs) grew 9% from S$99.3 million to S$108.6 million. But the reader has to know to look at core profit, not IFRS profit, and most readers don't.

Three markets, three cycles

Centurion operates in three distinct industries that share one structural feature: each is undersupplied in professionally managed, regulation-compliant accommodation for a specific resident profile that has limited substitutes.

Singapore PBWA hosts approximately 460,300 work permit holders in the Construction, Marine Shipyard and Process industries as at June 2025, all of whom require licensed dormitory accommodation under the Foreign Employee Dormitories Act (figure varies with the construction cycle) [9]. After the 2020 dormitory outbreak, the Ministry of Manpower introduced new standards: Improved Dormitory Standards (IDS) as an interim measure, and New Dormitory Standards (NDS) as the long-run requirement. The Dormitory Transition Scheme (DTS), articulated in MOM’s 17 January 2026 press release [1], requires approximately 900 existing migrant worker dormitories housing roughly 200,000 workers to transition to IDS by 2030, with NDS by 2040 for early adopters. Crucially, dormitories that convert from 16 residents per room to 12 reduce their licensed bed capacity by 25% for the same building, so industry-wide bed capacity contracts during the 2026–2030 transition. Operators who cannot or will not retrofit lose their licences.

Centurion's positioning here is its single strongest competitive feature. The largest NDS-compliant PBWA capacity in Singapore — Westlite Ubi, Westlite Toh Guan with its new block, Westlite Mandai with its Expanded Capacity, Westlite Woodlands and Westlite Juniper — sits inside CAREIT, with the four Westlite Quick-Build Dormitories adding directly-owned NDS-compliant capacity at Centurion. The moat is the recycling platform rather than the legal-entity location of any individual building: Centurion develops the NDS-compliant pipeline, drops the stabilised asset into CAREIT, retains the manager fee on it for the life of the REIT, and recycles the proceeds. While competitors are losing licensed capacity, the Centurion–CAREIT platform is adding compliant capacity at scale — the new Toh Guan block contributed c.1,764 beds in October 2025 and the new Mandai block c.3,696 beds in January 2026 at the CAREIT-owned properties. Approved retentions of legacy capacity at the same sites preserve operating revenue during the transition: 664 beds at Toh Guan until 31 December 2028, and 1,980 beds at Mandai until 31 December 2030. Demand is anchored by Singapore's construction cycle: the BCA forecasts total construction demand of S$47 billion to S$53 billion in 2026, declining slightly to S$39 billion to S$46 billion annually through 2027 to 2030 [2].

Malaysian PBWA is a different story. Malaysia hosts approximately 2.4 million documented foreign workers, and enforcement of Act 446 (the Employees’ Minimum Standards of Housing, Accommodations and Amenities Act 1990) has intensified through 2024, 2025 and into 2026, with a “comply-or-lose-licence” mandate for Centralised Labour Quarters now reportedly in effect particularly across Selangor and the Klang Valley [3]. The Multi-Tier Levy Mechanism was implemented 1 March 2026 [4]. The maximum accommodation rental cap was revised to RM150 per worker per month [5]. Centurion is the largest privately-owned PBWA operator in Malaysia by bed count, with capacity exceeding 20,000 beds. The September 2025 acquisition of Harum Megah added six operating dormitories in Johor, expanding Malaysian capacity by approximately 25% in a single transaction.

Global PBSA, primarily UK and Australia, is undersupplied at the structural level. Australia hosts approximately 1.6 million enrolled university students against a total PBSA bed count of only approximately 90,000 beds. The Student Accommodation Council estimates that 84,000 new PBSA beds are needed by 2026, but only 7,700 are in the pipeline [6]. CAREIT’s acquisition of EPIISOD Macquarie Park at A$345 million for 732 beds (A$471,000 per bed) reset Australian PBSA pricing expectations and drew Singaporean REIT and European pension capital into the segment [7]. Centurion’s directly-held Australian pipeline includes c.644-bed EPIISOD North Melbourne (1H 2027), c.472-bed Perth (4Q 2027), and c.675-bed Mackenzie Melbourne. The UK is the most cautious market: Unite Group, the UK’s dominant pure-play PBSA REIT, trades at approximately 51% discount to NTA per share and has guided 2026 EPS down 12.6% versus 2025 [8]. Centurion’s UK assets have so far outperformed (98% occupancy FY2025), but the CAREIT prospectus already factors in mid-single-digit UK revenue decline in FY2026.

What cannot be copied

Centurion’s competitive position rests on four sources of durable advantage.

First, regulatory positioning in Singapore. Singapore’s PBWA market is licensed under the Foreign Employee Dormitories Act. New PBWA capacity requires a licence granted on a per-site basis after compliance with the New Dormitory Standards. NDS compliance is expensive: higher floor area per resident, larger common facilities, more demanding fire safety and infection control infrastructure. New entrants face a structural cost disadvantage relative to operators who have already amortised the compliance cost across a portfolio. Centurion controls the largest NDS-compliant PBWA portfolio in Singapore as at 1Q 2026 — most of it inside CAREIT, where Centurion is the manager and the 42.9% unitholder, with the four Westlite Quick-Build Dormitories adding directly-owned NDS-compliant capacity at Centurion.

Second, sticky corporate customer relationships. The PBWA customer in Singapore is not the individual worker but the employer. Major construction companies, marine contractors, and shipbuilders contract with dormitory operators for multi-year leases covering thousands of workers. Switching costs are real: a contractor moving its workforce between dormitories incurs operational disruption, transport logistics changes, and contract renegotiation. Centurion’s customer base of more than two decades includes most of the major Singapore construction names. CAREIT CEO Tony Bin disclosed in November 2025 [14] that renewal rates run above 85% on the Singapore PBWA portfolio, with roughly 60% of residents staying for more than five years.

Third, brand verticalisation in PBSA. The new EPIISOD premium PBSA brand, launched July 2025, complements the existing mainstream Dwell Student Living brand. The first EPIISOD property, EPIISOD Macquarie Park in Sydney (732 beds), commenced operations in January 2026. Two brands at two price points captures the full spectrum of student demand, whereas a single-brand operator captures only one segment.

Fourth, the sponsor-REIT capital recycling mechanism. The CAREIT structure gives Centurion a permanent capital recycling mechanism that did not exist before September 2025. Centurion develops or acquires an asset on its own balance sheet, stabilises operating performance over one to three years, then offers the stabilised asset to CAREIT under the right-of-first-refusal agreement. CAREIT pays Centurion a market-clearing price, generating revaluation gain on the way out, and Centurion redeploys the proceeds into the next development. The arithmetic only works if CAREIT trades at or above 1.0x P/B (currently 1.25x), if CAREIT has capital access (clean balance sheet post-IPO), and if the asset stabilises within Centurion's tolerance. All three conditions are intact as at May 2026. The model is the moat because no other Singapore-listed PBWA operator has built one.

The financial scoreboard

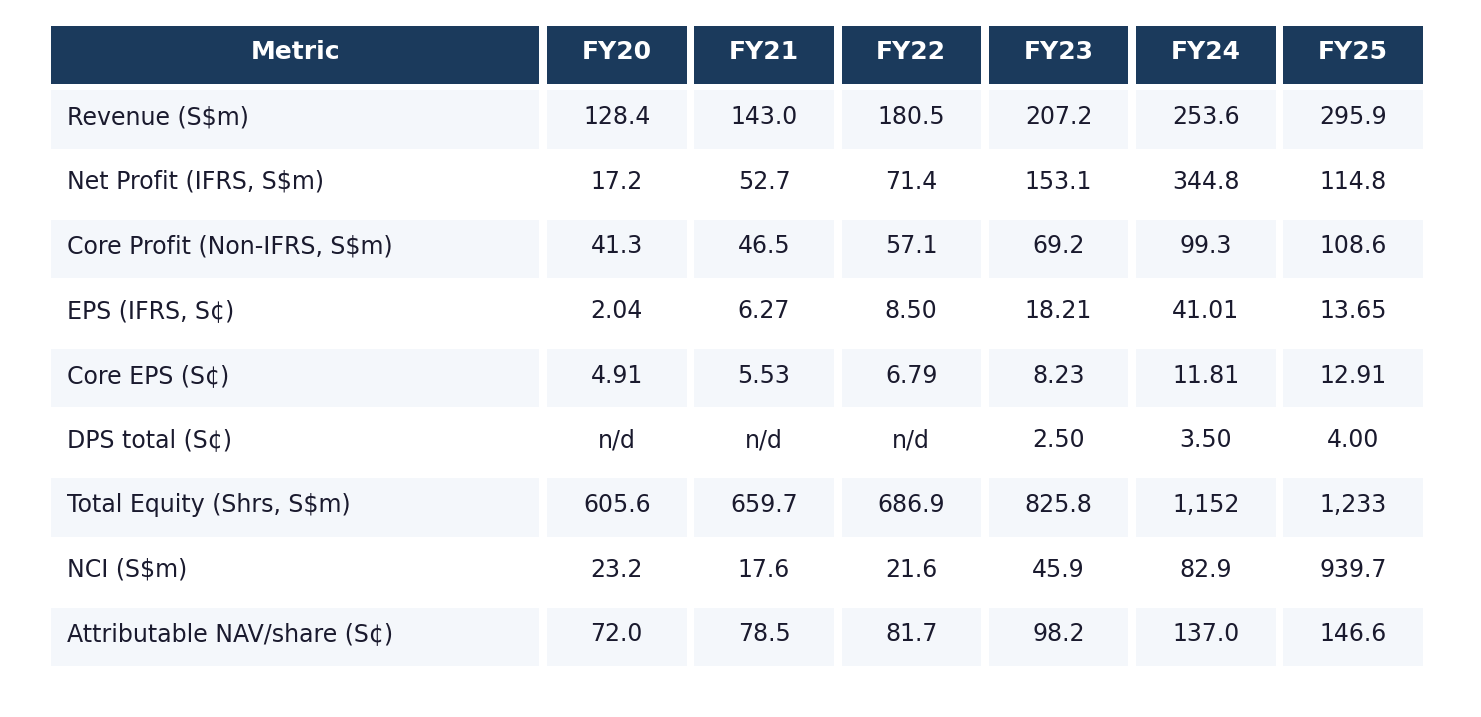

The six-year picture for Centurion, drawn from the published 5-Year Summaries in the FY2023 and FY2025 Annual Reports.

Three patterns are worth surfacing.

Revenue compounded at 18.2% per annum from FY20 to FY25. Top-line growth is the cleanest signal in the scoreboard because it is unaffected by fair value movements, deferred tax, or any of the items that distort net profit. 1Q 2026 revenue was up 30% YoY at S$89.4 million, which annualises to a FY2026 run-rate of approximately S$370 million before any additional capacity adds. Full-year FY2026 reported revenue should print materially higher, driven by full-year CAREIT consolidation versus three-month FY2025 consolidation.

Core profit attributable to shareholders compounded at 21.4% per annum from FY20 to FY25. The core profit measure adjusts for fair value movements and one-off transactions including the S$12.5 million of CAREIT listing costs in FY2025. Even after stripping out the FY2024 fair value gain of S$219 million that inflated reported IFRS profit, core profit continues to compound. Core EPS grew 9% YoY in FY2025 despite the asset spin-off.

Attributable NAV per share has more than doubled in five years. From 72 cents at end-FY2020 to 146.6 cents at end-FY2025, Centurion’s per-share equity has roughly doubled, supported by retained earnings and the FY2024 revaluation uplift on the Singapore PBWA portfolio. At the 16 May 2026 share price of S$1.46, Centurion trades at 0.996x book, basically at NAV.

Three pillars, priced as one

Here is the central tension. The market is pricing Centurion at 1.0x book and 11x trailing earnings. Those are operator multiples. They make sense for a single-pillar dormitory operator.

But Centurion is no longer a single-pillar operator. It is three things at once.

Pillar one is the directly-held portfolio: 24 operating assets, c.52,993 beds across six markets at 31 March 2026, generating operating revenue from per-bed rentals. This is the legacy operator business, just with more geographic diversity and a younger asset profile after the FY2024–FY2025 capacity adds.

Pillar two is the asset-management business. Centurion Asset Management Pte Ltd, wholly-owned, earns fees from CAREIT under the Trust Deed. The fee economics are detailed in the CAREIT prospectus: a base manager fee, a performance fee tied to DPU growth versus prospectus-projected DPU, acquisition and divestment fees, and property manager fees on each asset. The property managers, also Centurion-owned, additionally earn 2% of gross revenue plus 5% of NPI on each PBWA asset, and 4% of gross revenue on each PBSA asset. The same management platform additionally manages two private funds and, more recently, third-party PBWA properties for which Centurion bears no balance sheet capital. We have run the FY2026 fee math against CAREIT’s projected distributable income and built an estimate of the business’s annual fee revenue and operating profit. We do not run those numbers in this article; the multiple applied to value it is treated in a separate write-up.

Pillar three is the unitholding. As at 31 December 2025, Centurion held approximately 42.9% of CAREIT’s 1.722 billion units, equivalent to 738.6 million units worth S$805 million at the 16 May 2026 closing CAREIT price of S$1.09. After the proposed Dividend in Specie of 84.1 million units to Centurion shareholders (1 CAREIT unit per 10 OU8 shares), Centurion will hold approximately 38% of CAREIT. The CAREIT distribution income flowing to Centurion at the 42.9% stake against FY2026 projected distributable income gives an annual income figure of approximately S$48.8 million; post-Dividend in Specie this drops to approximately S$43.2 million. We have built a forward earnings model for CAREIT’s contribution to Centurion’s consolidated economics; the precise figures are not detailed here. The early operating evidence is encouraging: CAREIT’s first standalone reporting period (25 September to 31 December 2025) beat the prospectus forecast on every metric — DPU 1.739 cents versus forecast 1.630 cents (+6.7%), PBWA occupancy 97.6% versus forecast 95.8%, PBSA occupancy 99.1% versus forecast 97.3%, and aggregate leverage and financing costs better than forecast.

Adding the three pillars at market-observable values and applying credible multiples produces a per-share fair value materially above the 16 May 2026 close of S$1.46. The exact figure, and the segment-by-segment build that produces it, is not run in this article. What we will say here is that across the central case, the conservative case, and the optimistic case, the implied valuation lands above the current market price by a margin large enough to be worth understanding.

Why the market hasn’t priced this yet

Three explanations, in descending order of analytical weight.

The first is technical. The consolidated financial statements obscure the structure. A casual reader of Centurion’s FY2025 press release sees revenue +17%, net profit -63%, EPS -67%, and concludes Centurion is in earnings decline. The actual story is the opposite (one-time fair value gain in FY2024 distorted the prior year; underlying core earnings grew 9%) but the reader does not pause to do the adjustment. The CAREIT consolidation amplifies this by introducing NCI swings that further confuse non-specialist readers. The accounting is correct under SFRS(I) 10; the analytical inference from the reported numbers, without adjustment, is misleading.

The second is structural. Singapore institutional capital is concentrated in REITs as such, not in REIT sponsors. CapitaLand Investment is the exception, with the scale, brand, and S$125 billion AUM to attract institutional flows in its own right. Mid-cap REIT sponsors below CapitaLand Investment do not have a clean comp set on SGX; investors who like sponsor economics tend to buy the underlying REITs. CAREIT itself trades at 1.25x P/B and roughly 6% yield, attracting yield-seeking capital. The same investors do not necessarily buy OU8 alongside.

The third is governance. The cousin-controlled Loh-Han structure is unusual on SGX. Family-controlled mid-caps often trade at small but persistent discounts to non-family-controlled comparables of similar quality. The discount reflects governance risk pricing, a structural factor rather than evidence of any specific incident. The single material governance risk we monitor is the structural exposure to related-party transactions between Centurion family vehicles and the listed entities, which is the central risk we hold visible to readers of this article. The additional flip triggers tied to CAREIT unit price, Singapore occupancy levels, lock-up expiry dynamics, and ROFR cliff thresholds are not enumerated here.

The gap will close progressively, not immediately. The catalysts are CAREIT establishing a DPU track record supporting the manager fee economics, Centurion's directly-held pipeline (Australian PBSA, Malaysian Iskandar 7,000-bed development) demonstrating execution, any future drop-down transactions confirming the recycling model, and the analyst community modelling Centurion as a sponsor rather than a pure operator. By end-FY2026, with one full year of CAREIT operating performance and the projected DPU run-rate demonstrated, the market should be in a position to model the look-through more confidently.

The bottom line

Centurion at the 16 May 2026 close of S$1.46 prices a single-pillar dormitory operator. The September 2025 CAREIT IPO turned it into a three-pillar platform. The dormitory operator alone, valued on operator multiples, is worth roughly where it trades. The same business, framed as the operator-plus-manager-plus-unitholder it actually now is, is worth materially more. The transition from one frame to the other is where the analytical crux lies.

The full quantitative verdict, the forward earnings model, the look-through sum-of-the-parts, the scenario-weighted implied value, and the complete flip-trigger register are published in our institutional-length analysis. Link below.

Notes on the data

Three items material to readers of this article.

The detailed valuation arithmetic is treated separately. This article makes the case for the business and the structural argument. The segment-by-segment forward earnings model, the look-through sum-of-the-parts valuation across bull-base-bear scenarios, the probability-weighted implied value, and the complete flip-trigger register are written up in a separate piece.

Direct operating portfolio fair value is triangulated, not disclosed. Centurion’s consolidated financial statements present investment properties at fair value in a single line item that combines Centurion-direct properties with CAREIT properties post-consolidation. The split is not separately disclosed; our valuation segment derives the breakdown by deduction from segment data and from CAREIT’s standalone disclosures.

DPS history for FY2020 to FY2022 is not aggregated in published 5-Year Summaries. Individual half-year and full-year dividend announcements exist on SGXNet for those years but were not aggregated for this article. Marked as “n/d” in the scoreboard.

Post-publication correction (2026-05-29/31) — Westlite Toh Guan and Westlite Mandai are CAREIT-owned; portfolio totals re-anchored to the 1Q 2026 Business Update; three further factual corrections (Centurion management feedback). Centurion management noted that Westlite Toh Guan and Westlite Mandai are owned by CAREIT, and that the new redevelopment blocks at each property sit within the respective assets and are therefore also CAREIT-owned. CAREIT’s IPO Initial Portfolio comprises five Singapore PBWAs — Westlite Toh Guan, Westlite Woodlands, Westlite Ubi, Westlite Mandai and Westlite Juniper. The new block at Toh Guan (1,764 beds, October 2025) and the new block at Mandai (3,696 beds, January 2026) sit at those CAREIT-owned properties. Several passages in this article counted the new blocks in Centurion’s directly-owned bed total; they belong in CAREIT instead.

The initial correction restated the directly-held portfolio from “24 assets, c.53,107 beds” at publication to “c.22 assets, c.47,600 beds”. The principle was right; the arithmetic was not. The 53,107-bed figure had incorrectly included the new blocks (5,460 beds combined) on the Centurion side but had also omitted Westlite Tampoi (5,790 beds) and Westlite Senai II (3,700 beds) from the directly-held list, so the headline magnitude was approximately right by coincidence. The 13 May 2026 1Q 2026 Business Update resolved the composition cleanly: at 31 March 2026 the directly-held portfolio is 24 assets totalling 52,993 beds, comprising 5 Singapore PBWA, 13 Malaysian PBWA, 1 Hong Kong PBWA, 2 Hong Kong PBSAs, 1 Australia PBSA, 1 UK PBSA, and 1 Xiamen BTR. Including the April 2026 Australian Key Worker Accommodation additions, the post-1Q snapshot is c.26 assets and c.53,439 beds. CAREIT’s portfolio is correspondingly 15 assets and c.28,266 operational beds (or c.30,246 including the 1,980-bed Mandai Expanded Capacity retained until 31 December 2030 pending FEDA license).

The numerical thesis does not change. With thanks to Centurion management for the correction and to the 1Q 2026 Business Update for the definitive numbers.

Post-publication correction (2026-05-29) — FY2026 revenue bridge and Malaysian revenue weighting (Centurion management feedback). Centurion management noted that the FY2026 revenue bridge in the original article — which attributed roughly +S$160 million of ‘mechanical lift’ to the difference between three months and twelve months of CAREIT consolidation — was wrong, because most of the CAREIT-bound assets had been on Centurion’s revenue line for the full FY2025 (either as direct subsidiaries, as a 51%-owned consolidated subsidiary in the case of Westlite Ubi (held through Centurion-Lian Beng (Ubi) Pte Ltd at 51% Centurion / 49% Lian Beng Group per the Final Prospectus), or as a master-lease arrangement in the case of Westlite Juniper). The genuinely incremental items in FY2026 are Westlite Mandai’s transition from 45% equity-accounted associate to fully consolidated via CAREIT (an accounting transition that lifts the gross revenue line by approximately S$12 to S$19 million as Mandai’s pre-new-block annual revenue enters the line for a full year for the first time, plus a further S$14 to S$20 million from the new Mandai block running for a full year — without proportionally lifting attributable earnings, because Centurion’s economic share of Mandai net income drops modestly from 45% to ~42.9%); the new Mandai block running for a full year; EPIISOD Macquarie Park’s master-lease income for a full year; the Harum Megah Malaysian portfolio’s first full year; and the new Australian Key Worker Accommodation assets, offset by the US PBSA disposal. The realistic FY2026 revenue range is S$355 million to S$390 million (+20% to +32% YoY), not the S$420 million to S$460 million range cited in the article. The Harum Megah contribution has been re-sized against the disclosed acquisition figures (six Johor PBWA properties, 7,197 beds, RM110.8 million purchase price), with the implied per-bed economics of roughly S$650 to S$800 of revenue per bed per year putting Harum Megah’s annualised revenue at approximately S$5 to S$6 million. Centurion management also clarified that Malaysian PBWA generates materially lower SGD revenue per bed than Singapore PBWA — operating margins and ROIC are comparable, but Malaysian rents in local terms are lower and the Ringgit translates at a lower rate — so the bed-count comparison between Centurion-direct and CAREIT understates the revenue-weighted asymmetry. The thesis (look-through implied value materially above the market price across central, conservative and optimistic cases) does not change, because the SOP build relies on Layer 1 property value, Layer 2 fee economics and Layer 3 CAREIT market value, not on the FY2026 revenue bridge. What changes is the size and pace of the FY2026 catalyst the article was pointing to. The full quantitative restatement is set out in the institutional-length version (data-integrity note 13). With thanks to Centurion management for the clarification.

References

[1] Ministry of Manpower, “Applications for Dormitory Transition Scheme grant to open from 1 Mar to 31 Aug to help existing dormitories meet improved standards”, MOM press release, 17 January 2026. https://www.mom.gov.sg/newsroom/press-releases/2026/0117-dts-grant

[2] Centurion Corporation Limited, “Centurion Reports 30% Revenue Growth to S$89.4 Million in 1Q 2026”, SGX filing, 13 May 2026.

[3] UU.com.my, “Act 446 Malaysia Compliance Guide for Employer”, 2026. https://www.uu.com.my/act-446-malaysia-compliance-guide/

[4] Free Malaysia Today, “Multi-tier levy for foreign workers delayed to 2026”, 31 July 2025. https://www.freemalaysiatoday.com/category/nation/2025/07/31/multi-tier-levy-for-foreign-workers-delayed-to-2026

[5] Osadi Malaysia, “Malaysia Updates Act 446 Accommodation Rental Cap to RM150”, February 2026. https://osadi.com.my/malaysia-updates-act-446-accommodation-rental-cap-to-rm150/

[6] Australian Broker News, “Student housing surge in 2026 opens rich finance pipeline for Aussie brokers”, 2026. https://www.brokernews.com.au/news/breaking-news/student-housing-surge-in-2026-opens-rich-finance-pipeline-for-aussie-brokers-288866.aspx

[7] Cushman & Wakefield Australia, “Purpose-Built Student Accommodation in Australia”, December 2025. https://www.cushmanwakefield.com/en/australia/news/2025/12/purpose-built-student-accommodation-in-australia

[8] Motley Fool UK, “After tanking 46.5%, this FTSE 250 stock offers me an 8.1% dividend yield”, 3 May 2026. https://www.fool.co.uk/2026/05/03/after-tanking-46-5-this-ftse-250-stock-offers-me-an-8-1-dividend-yield/

[9] Centurion Corporation Limited, “Annual Report 2025: Evolving with Purpose”, SGX filing, 6 April 2026.

[10] Centurion Accommodation REIT, “Condensed Interim Financial Statements and Distribution Announcement for the Financial Period from 12 August 2025 (Date of Constitution) to 31 December 2025”, SGX filing, 23 February 2026.

[11] Centurion Accommodation REIT, “Prospectus dated 18 September 2025”, lodged with the Monetary Authority of Singapore.

[12] Centurion Corporation Limited (OU8.SI), share price and market data via Yahoo Finance, retrieved 16 May 2026. https://sg.finance.yahoo.com/quote/OU8.SI/

[13] Centurion Accommodation REIT (8C8U.SI), unit price and market data via Yahoo Finance, retrieved 16 May 2026. https://sg.finance.yahoo.com/quote/8C8U.SI/

[14] Julian Wong, “CAREIT CEO: The human touch behind Centurion’s living spaces”, The Edge Singapore, 14 November 2025. https://www.theedgesingapore.com/news/kopi-c-company-brew/careit-ceo-human-touch-behind-centurions-living-spaces

IMPORTANT DISCLAIMERS

This article is published for informational and educational purposes only. It does not constitute financial or investment advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The author is not a licensed financial adviser under the Financial Advisers Act 2001 of Singapore. This content is exempt from the requirements of the Singapore Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication. This publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, readers should consult a licensed financial or investment adviser in their relevant jurisdiction. Past performance is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author holds a long position in Centurion Corporation (SGX: OU8) as of the date of publication. This does not constitute a recommendation. This publication has received no compensation from Centurion Corporation or any related party.