UltraGreen.ai: Understated Earnings, One Untested Seam

UltraGreen.ai's (SGX:ULG) FY2025 earnings are understated by a tax charge and idle IPO cash; what stays untested is whether its US pricing power holds.

Long-form deep dive, institutional-level analysis, ~45-min read

Somewhere in a Singapore operating theatre this week, a surgeon will inject a few milligrams of green powder dissolved in sterile water into a patient’s bloodstream. Under a near-infrared camera, the compound, indocyanine green, will light up the patient’s blood vessels and tissue perfusion in real time: a glowing map of where blood is flowing and where it is not. The surgeon uses that map to decide where to cut, what to reconnect, and whether a newly joined section of bowel will survive. The dye has been in clinical use since the 1950s. The camera, the regulatory approvals, the distribution network and, increasingly, the data captured around each procedure belong to a company most Singapore investors had never heard of before December 2025.

UltraGreen.ai Limited listed on the SGX Mainboard on 3 December 2025 at US$1.45 per share, the largest non-REIT listing in Singapore since 2017 [12]. It sells roughly 83% of all indocyanine green (”ICG”) vials used in the United States and about 94% of those used in Europe, with no approved substitute for the fluorescence-guided surgery (”FGS”) indications it dominates [2]. It earned an 85.0% gross margin in FY2025. Its revenue has compounded at 43% a year since FY2022. As at 10 June 2026 the shares trade at US$1.42 [1], 2% below the IPO price and 24% below the February peak of US$1.86.

The market’s implied verdict is that this is a fully priced, mid-growth medtech: at US$1.42, roughly 18x our estimate of FY2026 earnings, against the premium multiples global medtech peers command, which published comp sets put anywhere from about 20x to 32x forward [8]. We think that verdict rests on a misreading of one income statement. FY2025’s reported numbers simultaneously overstate the group’s tax burden, through a one-time US$8.5 million provision that is the subject of a pending exemption application, and understate its interest income, because the US$150.0 million of IPO proceeds arrived in the final month of the financial year and earned almost nothing. One distortion reverses mechanically in FY2026; the other awaits a ministerial ruling, with both outcomes computable today. Together they could add roughly US$13–15 million of net profit, a 20–24% uplift on the underlying FY2025 base of US$63.8 million, before a single additional vial is sold.

This article works through three questions in sequence. First, are FY2025 earnings temporarily depressed? We will show the arithmetic says yes, and quantify it. Second, does UltraGreen’s US pricing hold through the hospital purchasing cycle? That is genuinely open, and we will name the one undisclosed variable that matters most. Third, can the ICG cash engine fund a credible platform business in data and imaging? That is conditional, and we will treat it as optionality rather than earnings. Along the way we will also explain why the share price fell 24% from its peak, why we think much of that fall was macro rather than company-specific, and what one number, due in August 2026, would make us abandon the thesis entirely.

From Frame Relay to fluorescent dye

Ravinder Sajwan, 64, did not invent anything UltraGreen sells. That is worth stating plainly at the outset, because the company’s moat makes more sense once you stop looking for the patent. Sajwan’s career is a Silicon Valley operator’s résumé: a 2,400bps modem design early on, a universal network-testing device acquired by Tektronix, senior technical roles at StrataCom, whose Frame Relay technology Cisco bought for US$4 billion in 1996, then the co-founding of Acclaim Communications, sold to Level One for US$120 million in 1998, shortly before Intel bought Level One for US$2.2 billion [3][19]. Between telecoms and medtech came a long, lucrative interlude producing 5-Hour Energy drinks, a business connected to founder Manoj Bhargava, which threw off dividends that capitalised the family’s Renew Group [3].

The ICG story began, by Sajwan’s own telling, around 2013, when he encountered the dye through a German medical device company using it to measure holes in hearts [3]. What he saw was not a molecule but a market structure. ICG itself is an old, unpatentable compound; Sajwan has compared it to matcha powder, an everyday-seeming ingredient with an outsized value per use [19]. The product is cheap to make, sells for a small fraction of the cost of the surgery it supports, and is protected not by intellectual property but by regulatory approvals, manufacturing accreditation, distribution relationships and surgeon habit. From 2015, Renew built UltraGreen by buying, partnering with and consolidating the companies that held those positions: the moat was assembled, not invented [3]. The group even founded the International Society of Fluorescence-Guided Surgery, a surgeon education body that, whatever its scientific merits, functions commercially as a standard-of-care flywheel for ICG procedures [19].

The capital structure history matters for what comes later in this article, so we set it out here. UltraGreen took no outside investors at all until 2025, when 65 Equity Partners (a Temasek-backed vehicle investing from a fund with an explicit mandate to groom companies for SGX listings) and Vitruvian Partners invested in a pre-IPO round [10]. Before that, in November 2024, the company issued a US$142.8 million promissory note to its immediate holding company RGPL, in effect a distribution to the controlling shareholder funded by an IOU, which pushed group equity negative (total equity at 31 December 2024 was negative US$26.0 million). In August 2025, the note was settled by issuing RGPL 142.8 million new shares at US$1.00 apiece. In the same pre-IPO window the company paid US$39.8 million of FY2025 dividends to its pre-listing shareholders and sold its UltraLinQ cardiology software business for a US$23.7 million gain. Then came the December IPO: US$150.0 million of primary proceeds at US$1.45 per share, within a roughly US$400 million total offering including a US$237.5 million cornerstone tranche taken up by sixteen institutions, among them abrdn, AIA, Eastspring and Lion Global [11][12].

The debut was respectable but not euphoric: the stock opened at US$1.51, touched US$1.62 intraday, and closed at US$1.52 [12]. Within nine trading days it was at US$1.31, and the stabilising manager deployed its full 20.7 million share mandate; the over-allotment option was never exercised [13]. The stock then rallied to US$1.86 by 23 February 2026, sold off through a risk-averse March, and slid to a US$1.20 low in late May after a first-quarter print the market misread [7], both of which we return to below; it sits at US$1.42 as we write [1]. A listing that was priced at 28.6x FY2024 earnings [12] now trades, on our normalised arithmetic, at a multiple in the high teens against earnings that have since grown.

What the company actually sells

UltraGreen is best understood as three layers stacked on one molecule.

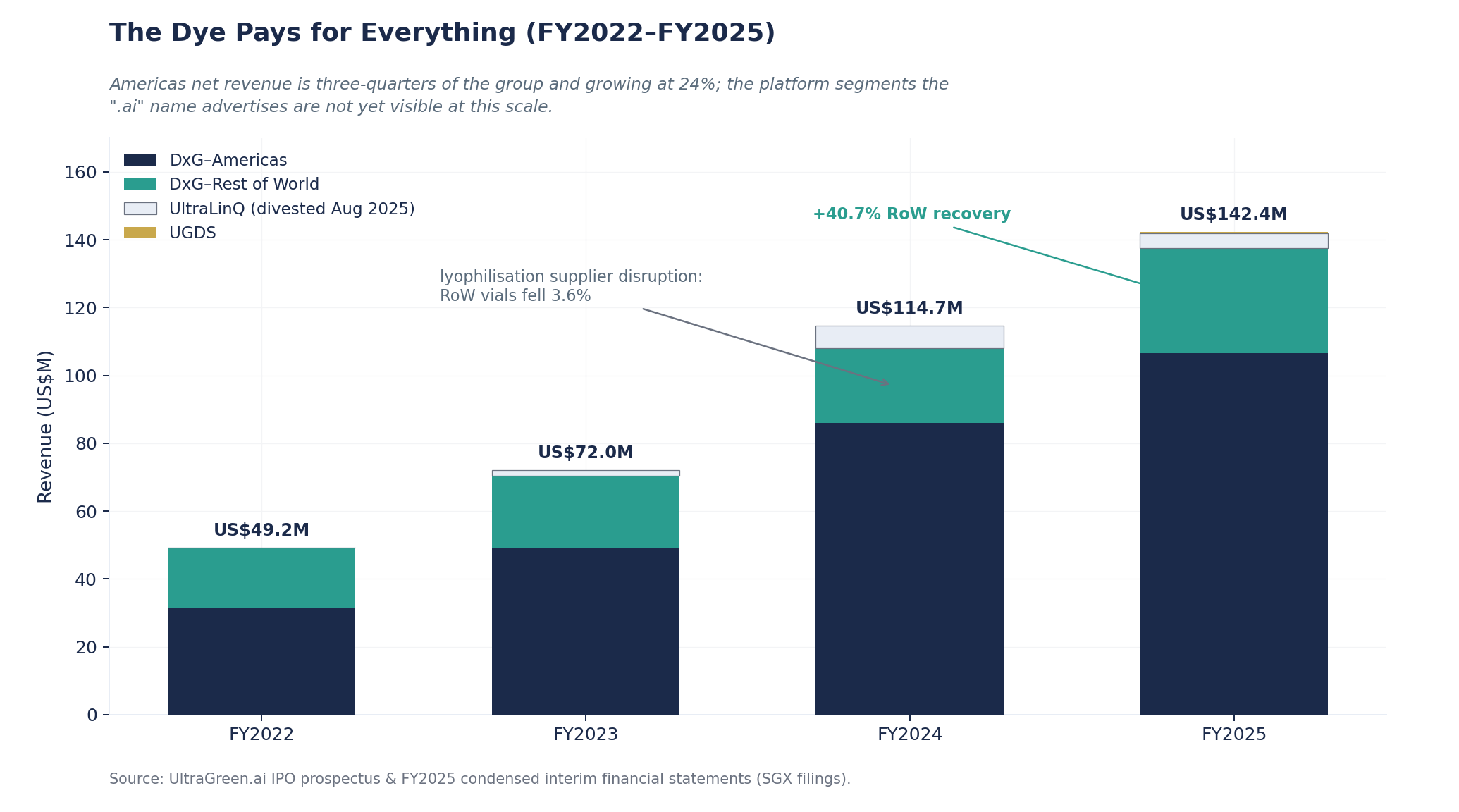

The first layer is the dye itself, and it is almost the whole income statement today. The group sells ICG vials under the IC-GREEN brand in the US and Verdye elsewhere, through two geographic segments. DxG–Americas generated US$106.5 million of net revenue in FY2025, 74.8% of the group total, up 23.9% year on year. DxG–Rest of the World generated US$31.0 million, up 40.7%. Volumes tell the same story with less noise: 667,800 vials shipped in the Americas in FY2025 and 319,900 elsewhere, 987,700 in total, up 13.2% on FY2024. Cumulatively the group had sold about 5.3 million vials since 2015 as at June 2025 [11]. Gross margin on all of this was 85.0% in FY2025, up from 75.5% in FY2022, a function of price increases falling through to a largely fixed cost of goods.

The second layer is hardware: the IC-Flow imaging system, a handheld near-infrared camera that makes the dye visible. UltraGreen’s German subsidiary Diagnostic Green GmbH is the license holder and manufacturer of record. The camera is not currently a profit centre; it is an ecosystem device, and the group’s Asia strategy makes that explicit. In Asia, UltraGreen will lease cameras to hospitals rather than sell them, lowering the entry cost for adoption while keeping the recurring vial sales and, importantly, the procedure data [10]. Camera manufacturing is being relocated from Germany and Ireland to Singapore, at the group’s MacPherson headquarters [10]. Commercial responsibility is split between two Chief Commercial Officers, one for the Americas and one, Fidelma Callanan, based in Ireland, covering everything else; the Asia build-out reports to her [10].

The third layer is the platform ambition that justifies the “.ai” in the name: the UltraGreen Data Platform, the PerfusionWorks perfusion-analytics software acquired with Denmark’s Perfusion Tech ApS (the remaining 72.6% was bought in June 2025 for US$5.6 million net of cash, adding US$3.7 million of goodwill and US$8.2 million of intangibles), and a small UltraGreen Data Systems (”UGDS”) segment created in 2025 from retained UltraLinQ staff. UGDS also distributes biosensor products from LifeSignals Inc., an associate of the controlling shareholder’s private group, a related-party arrangement we examine in the governance section. The platform layer is currently a cost: UGDS recorded US$0.4 million of revenue and a US$1.6 million operating loss in FY2025, and PerfusionWorks is targeted for commercial launch in 2027, a management target rather than a committed date. The regulatory groundwork is further along than the revenue line suggests: the IC-Flow system and the UltraGreen Data Platform carry US 510(k) clearance and CE marking, and PerfusionWorks has been filed for approval in Europe, with management indicating a potential European launch as early as 2026 and progress through the EU MDR and FDA pathways during the year. In April 2026 the group also branded its cardiology distribution business UltraGreen Cardiac Technologies, the commercial wrapper for the LifeSignals biosensor arrangement. There is also Ferronova, a 26.9%-owned Australian associate developing iron-oxide nanoparticle devices for sentinel lymph node biopsy, an adjacent modality that costs the group roughly US$0.5 million a year through the associates line. We note it here and set it aside: it is not material to the valuation.

One business is deliberately absent from this list. UltraLinQ, the cardiology image-management software the group sold in August 2025 for a US$23.7 million gain, contributed US$4.4 million of revenue in FY2025 before disposal and US$6.7 million in FY2024. Reported FY2025 revenue of US$142.4 million therefore overstates the continuing perimeter; the comparable core figure is US$137.9 million. We use the core figure throughout this article when we discuss growth.

The industry: a standard of care still in its first quarter

Fluorescence-guided surgery is one of those rare medical technologies whose clinical evidence base is enormous while its adoption remains shallow. More than 20,000 peer-reviewed publications and over 780 clinical trials involve ICG [5], and the dye has US FDA approval history stretching back decades. Yet FGS penetration is still below 25% of addressable procedures in the United States, and lower again in Asia-Pacific [8]. At UltraGreen’s April 2026 AGM, the CEO put the addressable market for just the four core procedures, laparoscopic cholecystectomy, colorectal surgery, breast sentinel lymph node biopsy and breast reconstruction, at roughly 10 million surgical procedures a year, of which the group currently serves a small fraction, with procedure growth running at mid-to-high single digits. Frost & Sullivan frames the same runway in dollars: it sizes the global ICG market at about US$173 million in 2024, against a total addressable market of roughly US$925 million were FGS and ICG adopted across every eligible procedure, which leaves the category only about 19% penetrated [2].

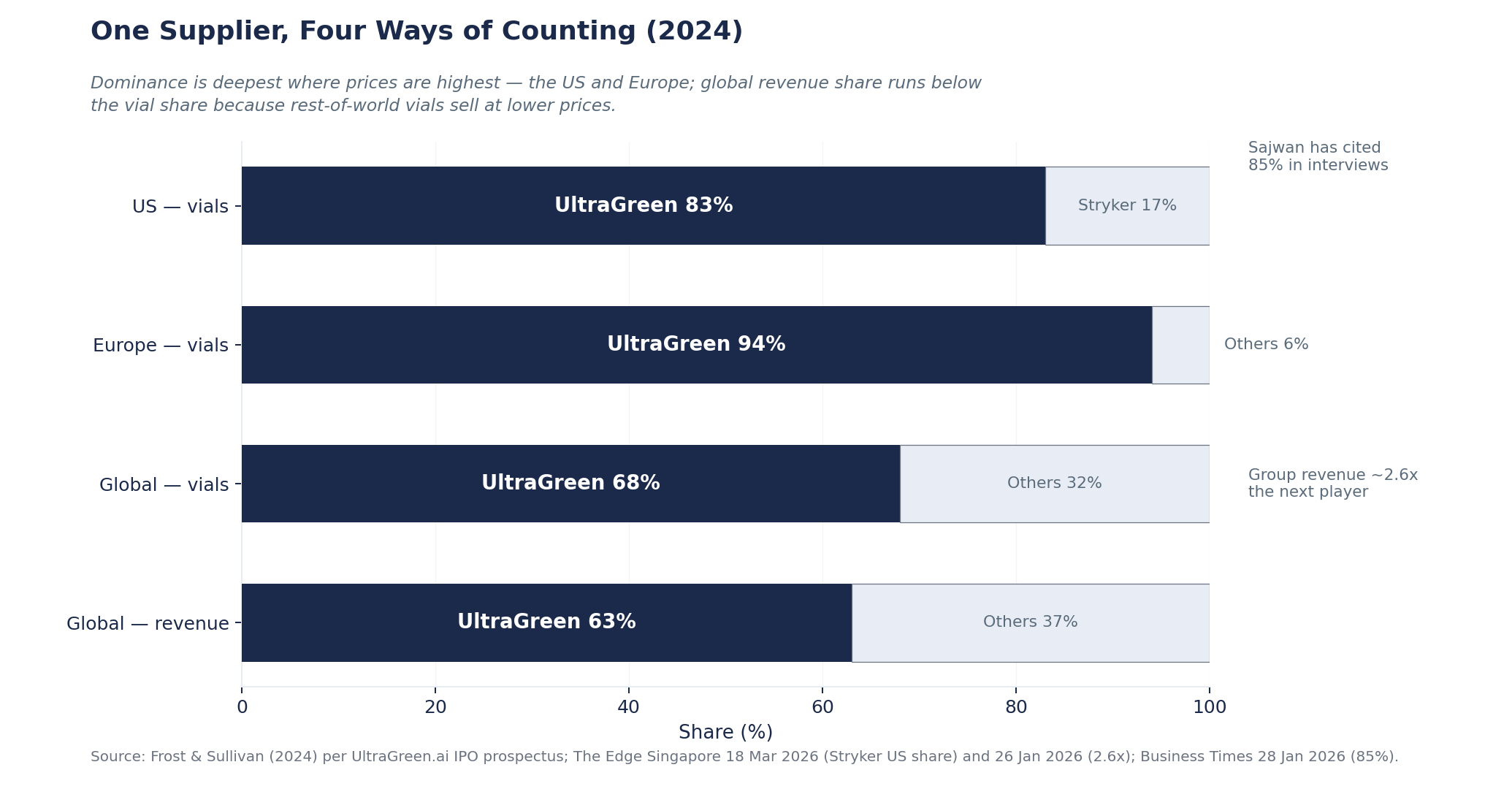

The competitive map is unusually concentrated. By Frost & Sullivan’s count, UltraGreen held about 68% of the global ICG market by vials and 63% by revenue in 2024, with 83% of US vials and a 94% share in Europe [2]; Sajwan has put the US figure at 85% in interviews [3]. The company’s revenue is roughly 2.6 times that of the second-largest player [18]. In the US, the remaining ~17% of the vial market belongs to Stryker Corp, the Michigan-based devices group [4]. Daiichi Sankyo, the original Japanese incumbent, retains only a minor global role [4]. There is no other FDA-approved fluorescent agent for the broad FGS indications ICG covers; emerging agents target specific procedures, and management’s stated view at the AGM was that ICG’s safety profile keeps it the default across the majority of use cases.

Two industry developments in 2026 bear directly on the investment case. The first is regulatory: UltraGreen’s approval footprint expanded from 35 territories in 2024 to 45 by mid-2026. The composition of those approvals deserves precision, because dye and camera travel on separate regulatory tracks. The Verdye dye itself was approved in the Philippines (December 2025) and Singapore (May 2026); the March 2026 four-country sweep across India, Thailand, the Philippines and Bangladesh, like the December 2025 Malaysia clearance, covers the IC-Flow V2 imaging system, with the dye still to follow in most of those markets. The camera approvals lay regulatory groundwork; meaningful revenue in those territories waits on the corresponding ICG registrations, and the company says approvals are being sought in roughly 20 further markets across Asia and the Middle East. Asia is the growth frontier, and the entry indications are deliberately chosen for emerging-market epidemiology: diabetic foot ulcer assessment and lymphedema, ahead of the surgical oncology uses that dominate Western volumes. Sajwan’s framing of the wound-care opportunity is worth quoting: “Five per cent penetration of the diabetic foot ulcer market is twice our current total addressable market.” [9]

The second development is the misfortune of the only US competitor. On 11 March 2026, a hacking group calling itself Handala, claiming Iran-linked motives, attacked Stryker’s Microsoft IT environment; the company’s SEC filing disclosed disruption to order processing, manufacturing and shipping [20]. Recovery was quick by the standards of such incidents: electronic ordering was restored for customers by 26 March, with most manufacturing sites and critical lines back and order reconciliation still under way [21], and by 9 April the company reported itself fully operational [25]. Brief as it was, the disruption was not trivial: Stryker’s amended SEC filing formally determined the incident had a material impact on its first-quarter 2026 operations and financial results, while leaving full-year guidance intact [25]. Hospitals buying a consumable that sits on the critical path of scheduled surgery prioritise supply reliability above almost everything, and a two-week ordering outage is long enough to force substitution decisions. We treat the possibility that displaced Stryker orders flowed to UltraGreen as a hypothesis bounded by that two-week window, to be tested by the next volume print, not as an accrued benefit; the timing arithmetic is in the deep dive. But the episode illustrates the asymmetry of this market: when 83% leans on 17%, disruption at the small player consolidates the large one.

The moat: three layers, one weak seam

Asserting a moat is cheap; the financial record either corroborates it or it does not. UltraGreen’s record corroborates three distinct layers of advantage, and exposes precisely where the structure is least tested.

The first layer is regulatory and clinical entrenchment. ICG is not proprietary, and management says so plainly: at the April 2026 AGM the CEO identified the group’s advantages as its regulatory approvals, manufacturing processes, ownership of the FDA drug master file, and accumulated clinical data, not the molecule. A would-be competitor needs an approved abbreviated new drug application, accredited sterile manufacturing, and a reason for surgeons to switch a consumable that costs a rounding error within a surgical bill. IC-GREEN has been FDA-approved since 1959 and remains the Reference Listed Drug other ICG products are measured against (we develop this point, and what the FDA register shows about would-be generics, in the risks section), and the publication and training flywheel around the group’s surgeon society raises the switching bar each year.

The second layer is distribution. In the US, the Big Three pharmaceutical wholesalers, Cencora, McKesson and Cardinal Health, collectively accounted for 67.8% of group revenue in FY2025. We will argue later that this concentration is more benign than it looks, because wholesalers are logistics and credit conduits rather than buyers with pricing power. But as a barrier it is real: shelf position inside the ordering systems of effectively every US hospital is something a new entrant cannot replicate quickly at any price.

The third layer is the one the income statement proves: pricing power, exercised in three rounds and absorbed each time. UltraGreen raised US prices by an average of 60% per vial in August 2023 and another 30% in April 2024, then implemented a further round of US pricing initiatives in the third quarter of 2025 that lifted US average selling prices 22% to about US$158 per vial that year. Over the period the global blended ASP went from US$70.3 per vial in FY2022 to US$139.3 in FY2025 [4], and volumes did not fall; Americas vials grew from 470,400 in FY2022 to 667,800 in FY2025, and total vials from 699,600 to 987,700. A 98% cumulative increase in the blended ASP met 41% volume growth over the same three years. Demand for ICG is, on this evidence, about as price-inelastic as consumables get, which is what you would expect for a product that enables a procedure billed at two or three orders of magnitude above the vial price.

The weak seam runs through the second and third layers where they meet: