The Watch Dynasty That Hasn't Issued a Share Since 1988

The Hour Glass (SGX:AGS) is asset-backed, family-run, and just made its largest acquisition while the seller was fleeing the brand.

Short-form deep dive, distilled analysis, ~15 mins read

Walk into the Rolex boutique on the casino floor at Crown in Perth, or into Tong Building at the top of Orchard Road in Singapore, and the experience is engineered to feel timeless. A salesperson who knows your collection. A display of steel sports models you cannot simply buy off the shelf. A waiting list that is itself a status object. None of it looks like a listed company, and that is the point. The business behind that boutique floor is one of the oldest continuously operating luxury watch retailers in Asia, and it has been run by the same family for forty-six years.

The Hour Glass Limited (SGX:AGS) was founded in 1979 by Dr Henry Tay and Dato’ Dr Jannie Tay. It listed on the Singapore Exchange in 1988 and has not raised a dollar of equity from public markets in more than three decades. For the financial year ended 31 March 2026 it earned a headline net profit of S$179.5 million on revenue of S$1,338 million, both records, and it closed the year with no bank debt or bonds for the first time in at least a decade. Its book value per share has risen every single year for seven consecutive years, from S$0.86 to S$1.67. At the 3 June 2026 close of S$2.63, the market values the whole company at roughly S$1,685 million.

The most interesting fact about The Hour Glass right now is the acquisition it completed in 2025, and the reason the seller gave for selling. In a deal worth AUD90 million, The Hour Glass bought THGRAU, the Australian Rolex authorised-dealer business previously owned by Kennedy Watches & Jewellery: four Rolex flagship boutiques in Melbourne, Sydney and Perth. The seller, James Kennedy, told the Australian Financial Review that the timing was right to sell the licence because Rolex “may sell directly to shoppers in the future” [1]. An informed seller cashed out of the exact relationship The Hour Glass paid AUD90 million to acquire, and told the press why. That tension is the question the institutional-length version of this analysis sets out to resolve in full; here we lay out why the franchise behind it is real, and where the market may be giving it too little credit.

That tension is the question the institutional-length version of this analysis sets out to resolve in full; here we lay out why the franchise behind it is real, and where the market may be giving it too little credit. Link below.

Forty-Six Years, Zero Equity Raises

The Hour Glass began in 1979 as a single boutique. Dr Henry Tay, a Monash-trained doctor who had practised before moving into business, and Dato’ Dr Jannie Tay built the company around an idea unusual for its time and place: sell luxury Swiss watches in Southeast Asia as objects of taste rather than as commodities, in retail environments that matched the brands’ own standards. The two founders were husband and wife, married in 1969, and they built The Hour Glass together for three decades before divorcing in 2010; both have remained substantial shareholders since, and their son Michael Tay now leads the group. Jannie Tay is today often known as Jannie Chan. The watch trade was already in Dr Tay’s family: his forebears ran Lee Chay & Co on North Bridge Road from 1946, one of the Singapore retailers Rolex appointed in 1950, so the group’s Rolex relationship is closer to seventy-five years old than to the company’s own forty-six [14]. The name itself sets the character of the company. An hour glass measures time by letting it run out grain by grain, a fitting emblem for a business that sells mechanical timekeeping and thinks in decades.

The company listed in 1988, and the most telling fact about the thirty-eight years since is a negative one: it has not issued a single new share to raise capital. Growth has been funded from retained earnings and modest borrowing that has now been fully repaid. A retailer that expands across eight countries without diluting its owners is doing something deliberate.

The growth came in layers. The first Australian boutique opened on the Gold Coast in 1988, at Marina Mirage. The Thai business that became THG Prima Times was built as a joint venture and is now a 49 per cent associate spanning Bangkok and, more recently, Vietnam. Japan followed, with a Ginza presence dating to the 1990s. The two acquisitions that matter most to the current story are recent: Mansors Jewellers in Auckland in February 2020, New Zealand’s oldest authorised Rolex retailer, as part of a New Zealand entry of more than NZ$80 million that also took in two Auckland commercial properties; and THGRAU in Australia in 2025. Both were Rolex dealerships, and both were acquired with Rolex’s explicit blessing.

Michael Tay, Dr Henry Tay’s son, became sole Group Managing Director in April 2020, taking day-to-day management into the pandemic. The timing matters: he assumed full control at the bottom, ran the business through the extraordinary boom of FY2022 and FY2023, through the correction of FY2024 and FY2025, and into the record FY2026. That is a complete cycle under one leader, and the company came out of it with more cash, less debt, and a larger network than it entered with. His own description of how the business is built is the one worth remembering: “It’s like kueh lapis, where you bake layer by layer. After that, you will have multiple layers, and our business is just like that” [9].

What The Hour Glass Actually Does

For reporting purposes The Hour Glass has one business segment: the retail and distribution of watches, jewellery and other luxury products across Singapore, Malaysia, Thailand, Vietnam, Hong Kong, Japan, Australia and New Zealand. It sells brands including Rolex, Patek Philippe, Tudor, Cartier, Hublot and F.P. Journe. There are no factories and no own-brand product of consequence. The company buys watches at wholesale and sells them at retail, and the entire economics of the business sit in that spread, in the inventory it carries to earn it, and in the relationships that determine which watches it is allowed to sell at all.

Geographically the group reports two segments. Southeast Asia and Oceania produced S$1,165 million of FY2026 revenue, about 87 per cent of the total; North East Asia, principally Japan and Hong Kong, produced S$174 million, about 13 per cent. There is no Mainland China operation, which over the last two years has been a feature rather than a gap: Mainland China and Hong Kong were the two worst markets in the global Swiss watch trade, and The Hour Glass does not sell into either at scale.

One distinction matters for reading the numbers. THGRAU, the Australian Rolex business, is wholly owned and fully consolidated, so its revenue and costs flow straight into the group accounts. THG Prima Times, the 49 per cent Thai and Vietnamese associate, is not controlled, so accounting rules bring in only the group’s share of its profit, S$15.6 million in FY2026, not its revenue. A reader who misses that distinction will misread both the growth and the risk.

A Shrinking Industry, Concentrating Upward

The backdrop is a Swiss watch industry contracting in aggregate while the top of it holds up. Swiss watch exports fell to CHF26.0 billion in 2024, down 2.8 per cent in value and 9.4 per cent in volume, then to CHF25.6 billion in 2025, a second consecutive annual decline [2][3]. The pain has been concentrated in Greater China: after Mainland China exports collapsed 25.8 per cent in 2024, 2025 brought a further 12.1 per cent fall there and a 6.5 per cent decline in Hong Kong, while the United States held up to become the single largest destination at about 17 per cent of all Swiss watch exports [3]. Fewer watches, more expensive ones: mix is moving upward.

The secondary market tells the same story. The Bloomberg Subdial Watch Index, which tracks resale prices of the most heavily traded Rolex, Patek Philippe and Audemars Piguet models, fell about 6 per cent in 2024 to a three-year low, then recovered about 8 per cent in 2025 on stronger holiday demand [4][5]. For a retailer, the secondary market is a sentiment gauge and a margin signal: when resale prices rise, retail demand is firm and discounting is absent; when they fall, the grey market widens.

Singapore as a market remains healthy. The Singapore Tourism Board reported 16.9 million international visitor arrivals in 2025, up 2.3 per cent, and record tourism receipts of S$32.8 billion for the full year, [7]; shopping has historically accounted for roughly a third of those receipts, with watches a named category in the STB breakdown. Chinese visitors were the largest source market at 3.1 million arrivals. A Singapore-headquartered luxury watch retailer with no direct Mainland exposure, capturing Chinese demand as it travels rather than at home, is positioned more sensibly in 2026 than it might have looked five years ago.

Behind the tourism numbers is a structural driver: new wealth is concentrating in The Hour Glass’s home market. Single family offices receiving tax incentives from the Monetary Authority of Singapore rose from about 400 at the end of 2020 to roughly 1,400 by the end of 2023 and continued toward 2,000 through 2024, the principals drawn heavily from China, India and Indonesia [11]. Knight Frank’s 2026 Wealth Report projects the global ultra-high-net-worth population to grow about 27 per cent over the five years to 2031, with several of The Hour Glass’s markets among the fastest: Australia close to 60 per cent, Vietnam 59 per cent, and Indonesia, a key source of its Singapore clientele, around 82 per cent [12]. This is a slow tailwind rather than a quarterly catalyst, but it puts the group’s flagship boutiques in the path of the new wealth arriving on their doorstep.

The Moat: Relationships You Cannot Buy

The competitive advantage of The Hour Glass has four parts, and most of them cannot be bought at any price.

The first is the brand relationships themselves. The right to sell Rolex and Patek Philippe as an authorised dealer is not for sale on the open market. It is granted, slowly, to retailers the maisons trust, and withdrawn from those they do not. The Hour Glass has held its Rolex relationship for about seventy-five years, since the founder’s family firm was among the retailers Rolex appointed in 1950, and operates one of roughly eighty Patek Philippe mono-brand boutiques in the world. A competitor with unlimited capital cannot simply buy an equivalent position; it would have to be invited into it over many years, and the brands have every incentive to keep the invitations few.

The second is the family, and it is the part most easily underestimated from a spreadsheet. The Hour Glass’s relationships with Rolex and Patek Philippe were built by the Tay family across forty-six years, through downturns weathered without dumping inventory and through consistent representation of the brands at the highest level. When Rolex approved the Mansors acquisition in 2020 and the THGRAU acquisition in 2025, it was approving transactions by people it knew, not by an abstract listed entity. Any change of ownership would introduce a transition risk that the current structure avoids entirely. This is the one competitive advantage in the business that cannot be acquired, replicated, or read off a balance sheet.

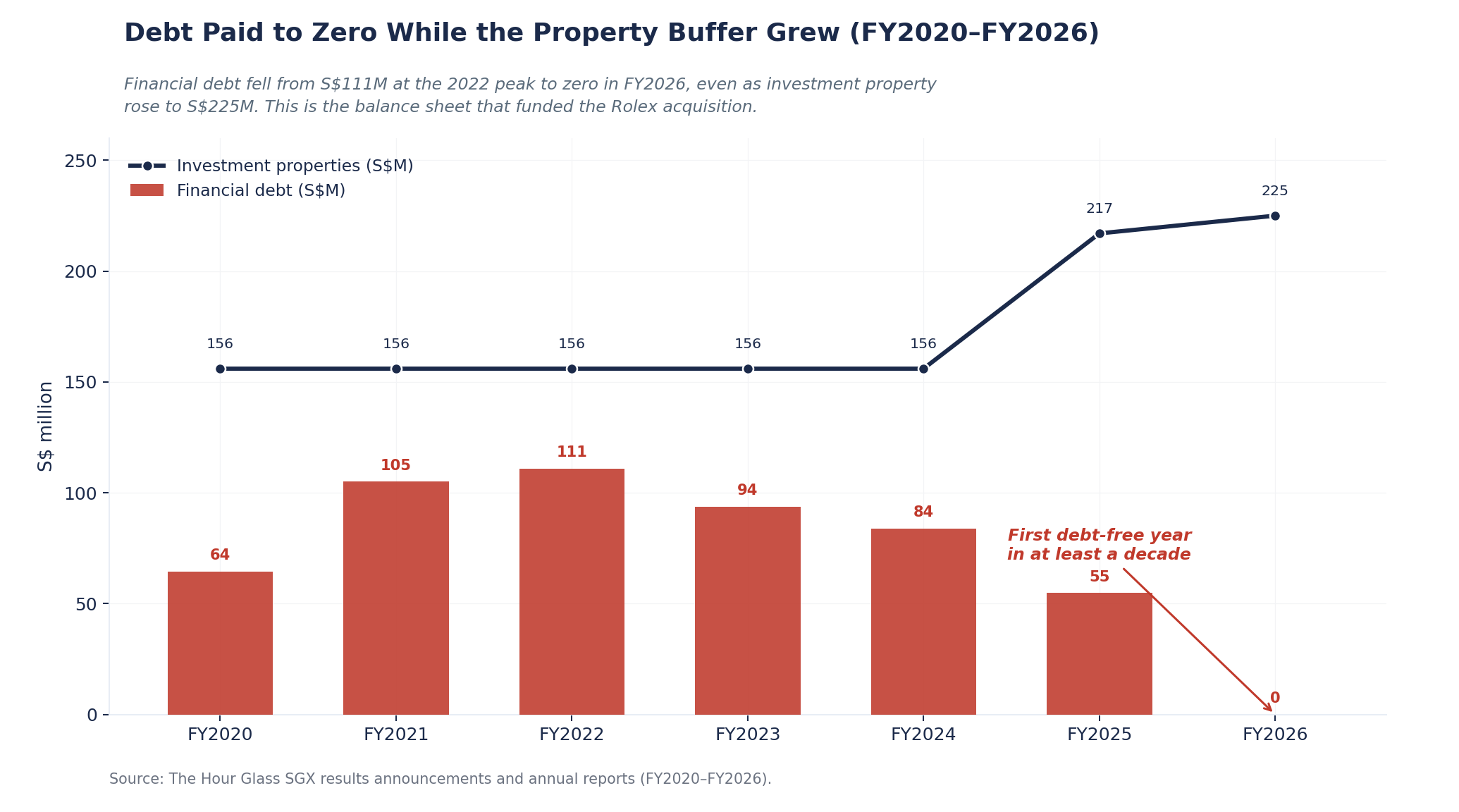

The third is the balance sheet as a strategic instrument. Zero financial debt, S$157.5 million of cash and S$225 million of unencumbered property give the company the capacity to act when a motivated seller appears and competitors are retrenching. That property is not a recent manoeuvre: the group bought its first building in Australia around 1992 and assembled the S$225 million position over more than thirty years, to occupy rather than to trade. That is exactly what happened with THGRAU: The Hour Glass built balance-sheet strength through the boom while others over-extended, then deployed it when Kennedy decided to exit.

The fourth part is the one most easily missed, because it produces little revenue and almost no headline: The Hour Glass is the regional curator of the ultra-premium independent watchmakers. Alongside Rolex and Patek Philippe, the group carries names such as F.P. Journe, Akrivia, Urwerk and MB&F, brands that Cortina and the mainstream Southeast Asian retailers do not stock. Its credentials here run deep: the group once owned the watchmakers Gerald Genta and Daniel Roth outright, buying them in the 1990s and selling both to Bulgari in 2000 [15]. It has also been one of MB&F’s original retail partners since the brand’s early days, stayed with it through the lean years, and now co-operates the world’s first MB&F Lab in Singapore, the kind of flagship partnership a new entrant cannot buy [16]. These watches are not allocated on a waiting list and are not arbitraged on the grey market; they are placed with collectors who have demonstrated taste and a relationship with the retailer, which means they carry the highest margins in the business with no brand quota and no competing regional retailer. The group’s ambition to be “the watch world’s leading cultural retail enterprise” is built on this layer, through collector events and the free IAMWATCH public lectures that cultivate a younger, more educated audience long before its members have the budget to buy. That audience is the client pipeline for the next five to ten years, and spending today to build it is the kind of long-horizon thinking that compounds a business over decades. With the group reporting a single segment, this layer cannot be sized from the disclosures; it is unpriced optionality and a competitive position no regional rival holds, not a number anyone can yet put in a model.

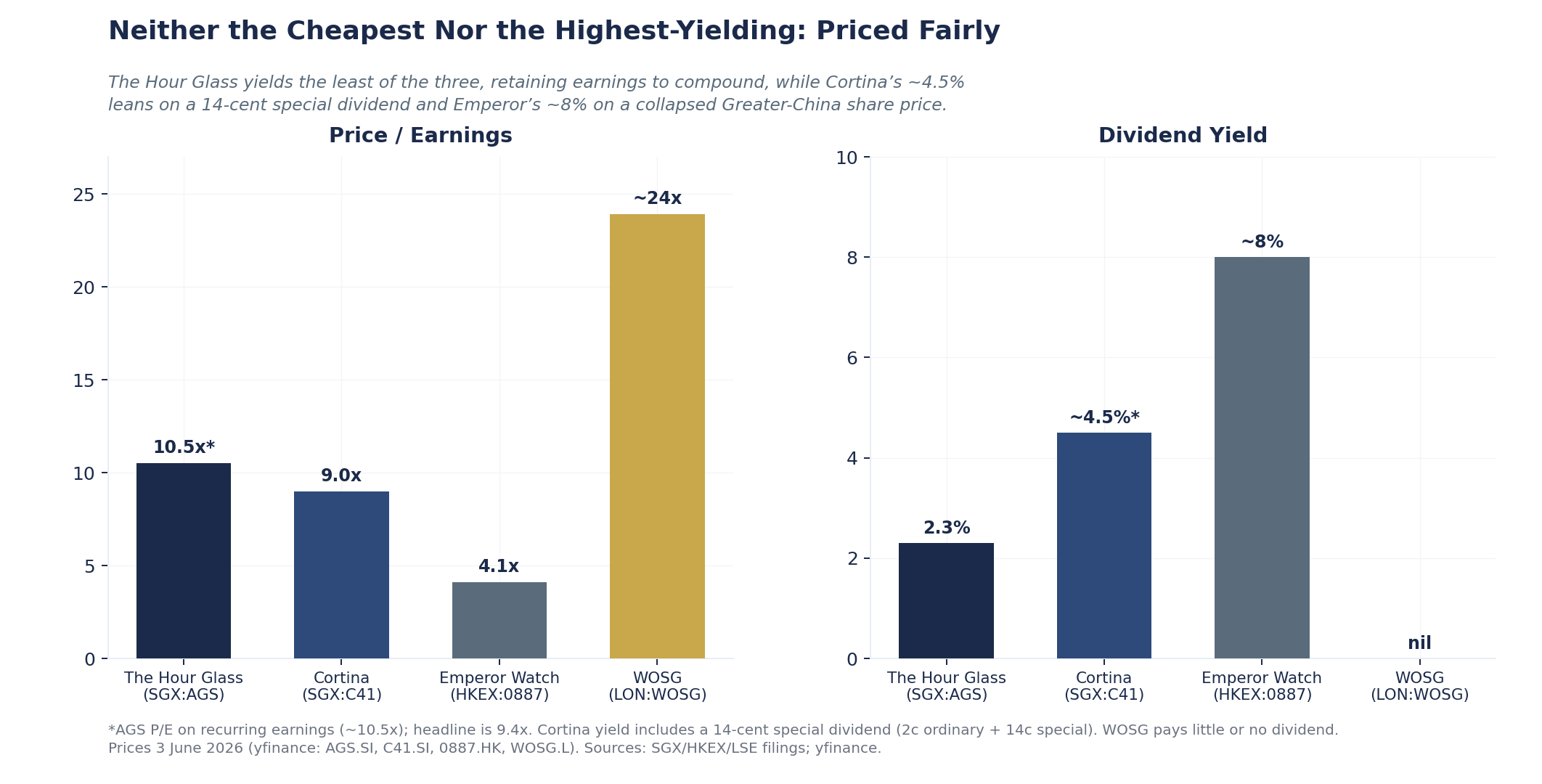

Where the moat is weaker is worth stating plainly. The brand relationships that cannot be bought also cannot be owned: they are licences, not property, and the maisons hold the right to change the terms. The family that built the trust is also the single point of failure if succession is mishandled. And the balance sheet that funds acquisitions earns a low operating return while it waits. The closest listed comparison, Cortina Holdings (SGX:C41), runs a similar model at a materially lower margin, roughly 6.6 per cent net against The Hour Glass’s roughly 12 per cent on recurring earnings [10]. The premium The Hour Glass earns is real, but it has to keep being earned through brand concentration and mix.

A sharper version of the same question comes from Hong Kong. Emperor Watch & Jewellery (HKEX:0887), a listed Greater China retailer that carries the same top brands, Rolex and Patek Philippe included, trades far more cheaply than The Hour Glass on every headline measure, and it is not a failing business: its revenue and profit both grew in the year to December 2025 [13]. The reasons it trades where it does are precisely the things The Hour Glass is not. Its recent profit growth is led by gold jewellery rather than watches, which makes it a less pure read on the watch franchise. It is concentrated in Hong Kong, Macau and Mainland China, the part of the market most exposed to the structural questions over Chinese luxury demand, where The Hour Glass spreads across eight markets and has just added Australia. And it is a tightly controlled family company that retains most of its earnings rather than returning them, with a 60 per cent controlling stake and related-party dealings, the kind of structure the market has long discounted. The Hour Glass is family-controlled too, but it has not issued a share in thirty-eight years and cancels the stock it buys back. The cheaper peer is real, and an investor who wants Greater China watch exposure at a low multiple can find it there. What they cannot find there is the combination of brand concentration, better geographies and capital discipline that the rest of this article describes.

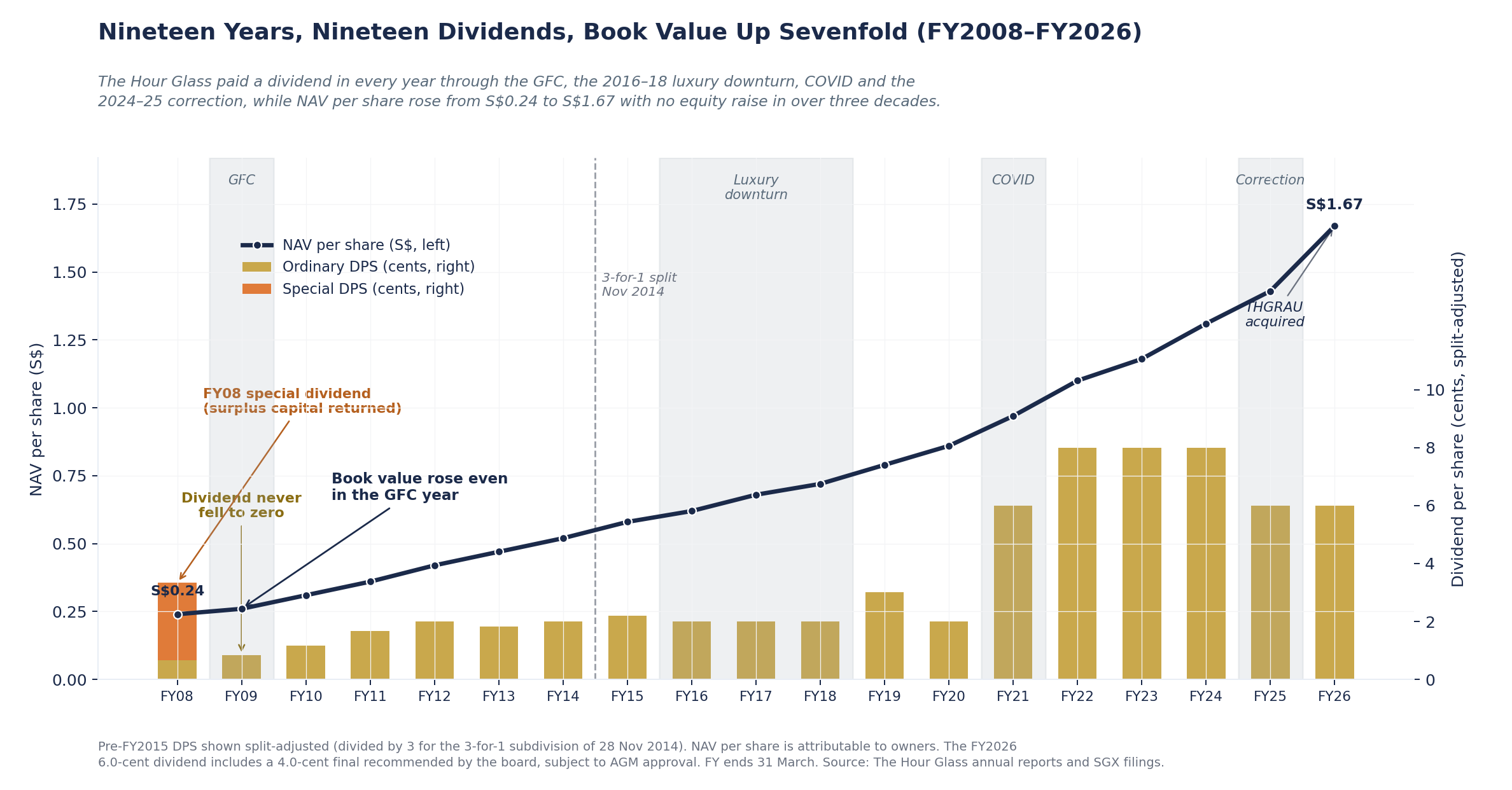

The Scoreboard: Seven Years of Rising Book Value

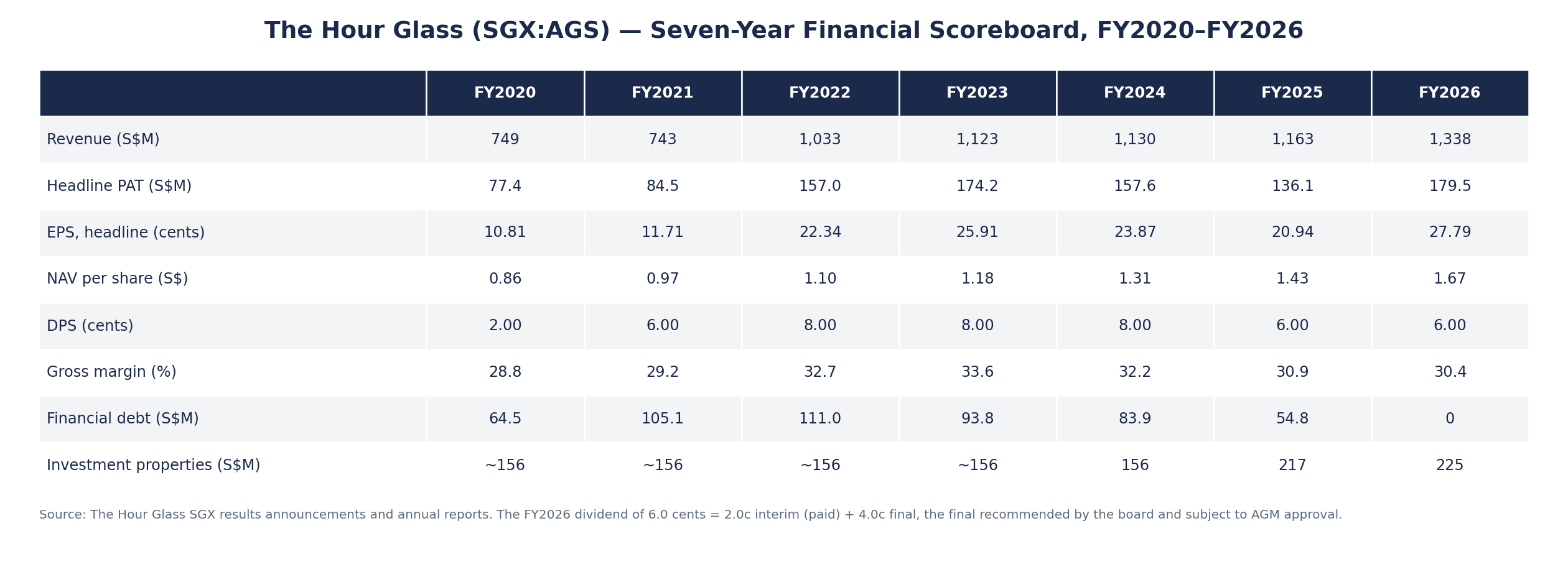

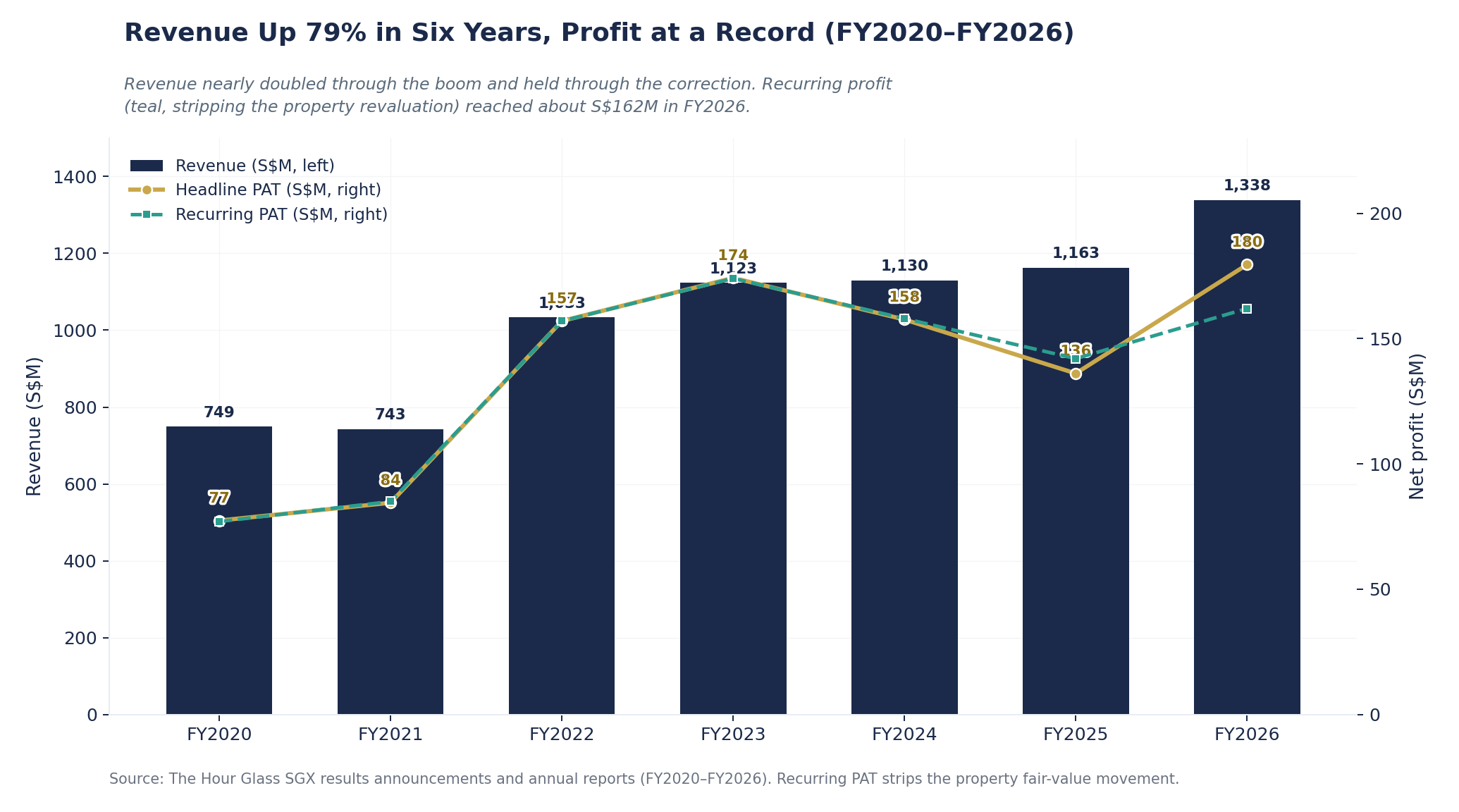

The seven-year record holds the whole story in one table: a doubling of revenue through a boom, a real correction in the middle, and a return to record earnings, with book value per share rising in every single year regardless of what the profit line did.

The arc reads in four parts. FY2022 and FY2023 were the boom: revenue jumped above the billion-dollar mark, gross margin peaked at 33.6 per cent, and headline profit reached S$174 million as the pandemic-era frenzy for waitlisted steel sports models ran at full force. FY2024 and FY2025 were the correction: the secondary market normalised, sentiment softened, a New Zealand deferred-tax charge bit, and headline profit fell 22 per cent from the FY2023 peak to S$136 million. FY2026 was the re-acceleration: revenue rose 15 per cent to a record S$1,338 million and headline profit reached a record S$179.5 million, helped by the consolidation of THGRAU.

The single number that survives all four phases is book value per share. It rose from S$0.86 to S$1.67 across the seven years, an increase of 94 per cent, compounding at roughly 11.7 per cent a year, and it rose in the correction years as well as the boom years. A retailer that keeps growing its net asset value per share through a 22 per cent earnings drawdown is retaining and reinvesting capital faster than the cycle can erode it. That is the financial signature of the business.

One caution on the headline profit belongs here. The FY2026 figure of S$179.5 million includes a S$20.3 million non-cash gain from revaluing the investment-property portfolio upward, which under Singapore accounting standards runs through the income statement. Strip it out and recurring profit is nearer S$162 million. The reported 9.4 times earnings is therefore closer to 10.5 times on recurring earnings, which matters for how cheap the stock really is.

Capital Allocation: Paid Every Year, Never Diluted

It is tempting to look at the 2.3 per cent yield and dismiss The Hour Glass as nothing special for income. That misreads it. The dividend is the residual left after the company funds inventory, boutiques, property, buybacks and the occasional acquisition, and the residual has a remarkable record: paid every single year, without exception, through the global financial crisis, the FY2016 to FY2018 luxury downturn [17], and the COVID closures of FY2020. In the boom years it has gone further, paying special dividends on top of the ordinary one, including a one-time special in the FY2008 boom that was four times the size of that year’s final dividend.

The global financial crisis shows the model under stress. FY2009 headline profit fell 57 per cent, but S$14.1 million of that was a one-off impairment on a listed investment unrelated to watch retail; the core business fell only about 13 per cent and recovered above its pre-crisis peak the very next year, with the dividend maintained throughout. Across fifteen years, book value per share has compounded at roughly 11 per cent a year on a split-adjusted basis, rising through every downturn. A shareholder who bought during the FY2016 luxury downturn, when the stock traded around or below S$0.60 split-adjusted, would have more than quadrupled their capital by today’s S$2.63, before a single dividend.

None of that came from yield. It came from a business that reinvests retained earnings at a mid-teens return on equity, has not issued a new share to raise capital in over three decades, and has been shrinking its share count rather than growing it, from about 705 million shares after the 2014 subdivision to roughly 646 million today, including S$112.3 million of treasury shares cancelled outright in FY2026. The 2.3 per cent yield is the by-product of that machine, not the reason to own it.

The Two Things the Market Has Not Yet Tested

Two specific developments sit behind the FY2026 numbers, and neither has been seen across a full clean year yet.

The first is THGRAU. The Australian Rolex business consolidated from 30 April 2025, so FY2026 captured only eleven months of it, and the purchase-price allocation was still provisional at the half-year. FY2027 will be the first clean twelve-month contribution, and the first year in which the audited standalone economics of the four boutiques are visible. The Southeast Asia and Oceania segment grew by S$167 million in FY2026, and THGRAU is the dominant contributor, although organic growth, currency and other movements are folded into the same segment line, so a clean THGRAU-only figure is not available until the FY2026 annual report is filed, expected in July 2026.

The second is the conversion of multi-brand stores into single-brand boutiques. The clearest delivery so far is the Patek Philippe Boutique Tokyo Ginza, which opened on 29 January 2025, one of roughly eighty Patek mono-brand boutiques worldwide and the second in Japan, built at around 200 square metres from the shell of the former multi-brand store [8]. A mono-brand conversion deepens the relationship with the maison, removes cannibalisation between brands on the same floor, and signals a franchise credential a new entrant cannot match. The capital cost is limited to fit-out, and the benefit shows up as mix rather than as a new revenue line, which is part of why it is easy to miss.

We have built the segment-level arithmetic on what a full year of THGRAU plus the conversion programme does to forward earnings, and it produces a figure that sits meaningfully above what the trailing numbers imply. The detailed forward build, and what it does to the valuation, is held back from this article. What can be said here is that the gap between the trailing multiple and the forward economics is the heart of the case, and it is the part the market has the least basis to have priced, because the audited numbers do not yet exist.

The One Risk That Matters Most

If the bull points are real, so is the central risk, and it is the same transaction that drives the upside. The Hour Glass paid AUD90 million for THGRAU and put S$66.5 million of it on the balance sheet as “distribution rights” with an indefinite useful life, an accounting treatment that says the asset does not wear out. The man who sold it said he sold precisely because that future looked uncertain, that Rolex “may sell directly to shoppers in the future” [1]. The buyer booked permanence; the seller cited impermanence as his reason for leaving.

The uncomfortable part is the contract. The actual agreement between Rolex and the THGRAU boutiques is not public, but comparable Rolex authorised-dealer agreements that have surfaced elsewhere typically allow either party to terminate without cause on short notice. An asset carried as indefinite-life on the balance sheet may, in contractual reality, sit on a notice period measured in weeks. Set against that is the pattern of behaviour: Rolex has not, in any documented case, internalised a major mono-brand flagship dealer of the kind The Hour Glass now runs, its chief executive said publicly in November 2025 that it intends to keep authorised dealers as its primary channel [6], and it approved not one but two acquisitions by The Hour Glass in five years. The same variable, Rolex’s assessment of The Hour Glass as a partner, drives both the downside and the upside. The realistic risk is not dramatic termination but slow erosion, through allocation and capex pressure and the ordinary margin cycle of luxury retail. The full risk register, and the specific signals that would break the thesis, are deliberately held back from this shorter analysis; this is the one risk every holder should understand.

Valuation: Why the Headline Multiple Is Not the Whole Story

At the 3 June 2026 close of S$2.63, The Hour Glass trades at 9.4 times reported earnings, or about 10.5 times once the property revaluation is stripped out, at 1.58 times book value, and on a total shareholder yield of about 3.1 per cent including buybacks. None of that is a deep-value signal. Ten-and-a-half times recurring earnings for a debt-free, high-quality luxury watch retailer is a fair-to-modest price, not an obvious bargain, and the honest version of the case does not pretend otherwise.

The reason the stock is interesting anyway is what sits behind the earnings. A buyer at S$2.63 is acquiring a business with zero financial debt, S$157.5 million of cash, S$225 million of investment property carried at fair value, and a S$107.1 million stake in the Thai associate, none of which earns an operating return in the recurring profit line but all of which is real asset backing. The working capital is disciplined too, which matters for a watch retailer where cash can get trapped in slow-moving stock: The Hour Glass turns its inventory about 2.4 times a year against roughly 1.8 times at its listed peer Cortina, both on their latest FY2025 accounts, tying up materially less cash per dollar of sales. A sum-of-parts that values the operating business on earnings and adds the cash, property and associate at sensible haircuts produces a range of implied values that brackets the current price, with the downside protected by the assets rather than by the multiple. Those assets are not dollar-for-dollar, to be clear: the property is illiquid and tax-affected, the 49 per cent stake in the Thai associate cannot be monetised without selling it, and the thin family float means minorities depend on the family’s capital-allocation choices rather than on any forced distribution. They cushion the downside; they do not set a hard floor. The full sum-of-parts build, the bear-base-bull range, and the resulting implied value are deliberately held back from this article. The conclusion that can be shared is the shape of it: a modest, asset-protected downside against a wider upside that depends on the THGRAU full year and the acquisition optionality delivering.

The Bottom Line

The Hour Glass is a high-quality, balance-sheet-protected luxury watch retailer at a fair price. It is debt-free, it has compounded book value per share at roughly 11 per cent a year for fifteen years, it has paid a dividend every single year through three downturns without once raising equity, and it holds Rolex and Patek Philippe relationships that no amount of capital can simply buy. It is not an obvious bargain at roughly 10.5 times recurring earnings, and the protection on the downside comes from the cash and property rather than from the multiple. The near-term upside comes from the first full year of THGRAU, the mono-brand conversion programme, and the optionality of a third Rolex acquisition the balance sheet can already fund. The longer-term upside comes from two things the earnings screen cannot see: a curated-independent position no regional competitor occupies, and a structural wave of new Asian wealth concentrating in the group’s home market.

The central tension is the one the seller handed us. The buyer booked the Rolex distribution rights as permanent; the seller left because he thought they were not. The reconciliation is the family: the relationship that earned two acquisition approvals in five years is the same relationship that makes outright expropriation unlikely, and it is the one asset in this business that cannot be valued from a balance sheet. Whether that is enough, at this price, to make the stock more than a fair-value holding depends on the forward earnings build and the valuation range that this article has deliberately stopped short of. The franchise is real. What it is worth, to the dollar, is the question the full analysis answers.

The forward earnings build, the complete sum-of-parts and implied value, the full risk register and the specific signals to monitor are available in the institutional-length version of this analysis. Link below.

Notes on Data Integrity

Source of FY2026 figures. Drawn from The Hour Glass’s unaudited condensed full-year results filed with SGX in May 2026 and the H1 FY2026 half-year results. The full FY2026 Annual Report, with complete notes, is expected around July 2026, so the THGRAU purchase-price allocation and standalone economics, the THG Prima Times FY2026 financials, and the detailed investment-property composition remain provisional.

Recurring earnings are author-derived. Recurring profit strips the S$20.3 million property fair-value gain and its deferred tax, and is an approximation.

THGRAU contribution. The S$167 million segment increase is the total segment movement, not a verified THGRAU-only figure.

Rolex agreement terms. The reference to short-notice termination is drawn from comparable public Rolex dealer agreements in other jurisdictions, not from the THGRAU contract, which is not public.

Market data. Retrieved on 3 June 2026 via yfinance (AGS.SI). The peer comparison with Emperor Watch & Jewellery uses operating figures from Emperor’s FY2025 annual report (year ended 31 December 2025) [13], not a data vendor.

Macro context. Singapore family-office figures are from the Monetary Authority of Singapore and the wealth-growth projections from Knight Frank’s 2026 Wealth Report, used as context rather than valuation inputs.

Analytical independence. No third-party analyst research, rating or price target was used as an input; the conclusions derive from primary filings and market data.

References

[1] Primrose Riordan, "Kennedy family sells off Rolex dealership to Singapore," The Australian Financial Review, 27 June 2025. https://www.afr.com/companies/retail/kennedy-family-sells-off-rolex-dealership-to-singapore-20250625-p5ma97

[2] Federation of the Swiss Watch Industry, 2024 export statistics, 30 January 2025. https://www.fhs.swiss/eng/2025_01_30_00_statistics.html

[3] Federation of the Swiss Watch Industry, 2025 export statistics, 29 January 2026. https://www.fhs.swiss/eng/2026_01_29_statistics.html

[4] Bloomberg, "Rolex, Patek, Audemars Piguet Used-Watch Prices Hit Three-Year Low," 7 January 2025. https://www.bloomberg.com/news/articles/2025-01-07/rolex-patek-audemars-piguet-used-watch-prices-hit-three-year-low

[5] Bloomberg, "Luxury Watch Prices Hit a Two-Year High in the Secondary Market," 8 January 2026. https://www.bloomberg.com/news/articles/2026-01-08/luxury-watch-prices-hit-a-two-year-high-in-the-secondary-market

[6] Rolex CEO Jean-Frédéric Dufour at Dubai Watch Week, November 2025. https://news.centurionjewelry.com/articles/detail/rolex-ceo-says-brand-will-stick-with-authorized-dealers-limits-retail-expansion

[7] Singapore Tourism Board, 2025 full-year tourism performance (16.9 million visitor arrivals; record S$32.8 billion in tourism receipts), announced at the Tourism Industry Conference 2026 on 8 May 2026. https://stan.stb.gov.sg/content/stan/en/tourism-statistics.html

[8] The Hour Glass, "Patek Philippe Boutique Ginza Tokyo." https://www.thehourglass.com/story/patek-philippe-ginza-tokyo-boutique

[9] Samantha Chiew, "The Hour Glass sees lower demand amid market uncertainties; sticks to fundamentals," The Edge Singapore, 24 October 2024. https://www.theedgesingapore.com/news/luxury/hour-glass-sees-lower-demand-amid-market-uncertainties-sticks-fundamentals

[10] Cortina Holdings (SGX:C41) FY2026 results, SGX filings.

[11] Monetary Authority of Singapore, single family office incentive data and the speech "Building a Stronger Tomorrow: Family Offices in our Flourishing Wealth Management Landscape," 16 September 2024. https://www.mas.gov.sg/news/speeches/2024/building-a-stronger-tomorrow---family-offices-in-our-flourishing-wealth-management-landscape

[12] Knight Frank, The Wealth Report 2026 (20th edition, April 2026; global and country ultra-high-net-worth growth projections to 2031). https://www.knightfrank.com/research/reports/wealthreport

[13] Emperor Watch & Jewellery Limited (HKEX:0887), Annual Report for the year ended 31 December 2025 (results announced 25 March 2026).

[14] The Hour Glass, "Our Rolex History" (Lee Chay & Co, North Bridge Road, from 1946; Rolex appointment 1950). https://www.thehourglass.com/rolex/our-rolex-history

[15] Federation of the Swiss Watch Industry, "Bulgari to acquire Gerald Genta and Daniel Roth," 5 July 2000 (acquired from The Hour Glass). https://www.fhs.swiss/eng/2000-07-05_44.html

[16] "Maximilian Büsser on the MB&F Lab and venturing beyond watchmaking," Tatler Asia, 2022 (MB&F Lab founded and operated in partnership with The Hour Glass; Singapore the largest MB&F collector community). https://www.tatlerasia.com/style/watches/mbf-lab-maximilian-busser-creative-process-venturing-beyond-watchmaking-interview

[17] The Hour Glass, FY2019 Annual Report, five-year financial highlights (FY2015–FY2019), showing the revenue and profit decline into the FY2017–FY2018 trough and the FY2019 recovery.

All The Hour Glass financial figures are sourced from SGX filings and the company’s investor relations site.

IMPORTANT DISCLAIMERS

This article is published for informational and educational purposes only. It does not constitute financial or investment advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The author is not a licensed financial adviser under the Financial Advisers Act 2001 of Singapore. This content is exempt from the requirements of the Singapore Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication. This publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, readers should consult a licensed financial or investment adviser in their relevant jurisdiction. Past performance is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author holds no position in The Hour Glass (SGX: AGS) as of the date of publication. This does not constitute a recommendation. This publication has received no compensation from The Hour Glass or any related party.

The SEA Analyst,

Thanks for sharing your analysis of The Hour Glass Limited (AGS; HG SP).

I also thought it was interesting, but I did not end up shortlisting it.

Like you said, the investment hinges on whether Rolex will expand into retail and eat AGS' lunch. I've heard both sides of the argument.

But I concluded that even though Rolex said they have no such plans, the fact remains that Rolex has the ability to upend AGS' business overnight.