The S$63 Million Question: Inside Singapore's Most Extreme Cash Shell

S$63.5 million in cash. A S$41 million market cap. And zero dividends. HL Global Enterprises (SGX: AVX) is either the most obvious deep-value play - or the most perfectly constructed value trap.

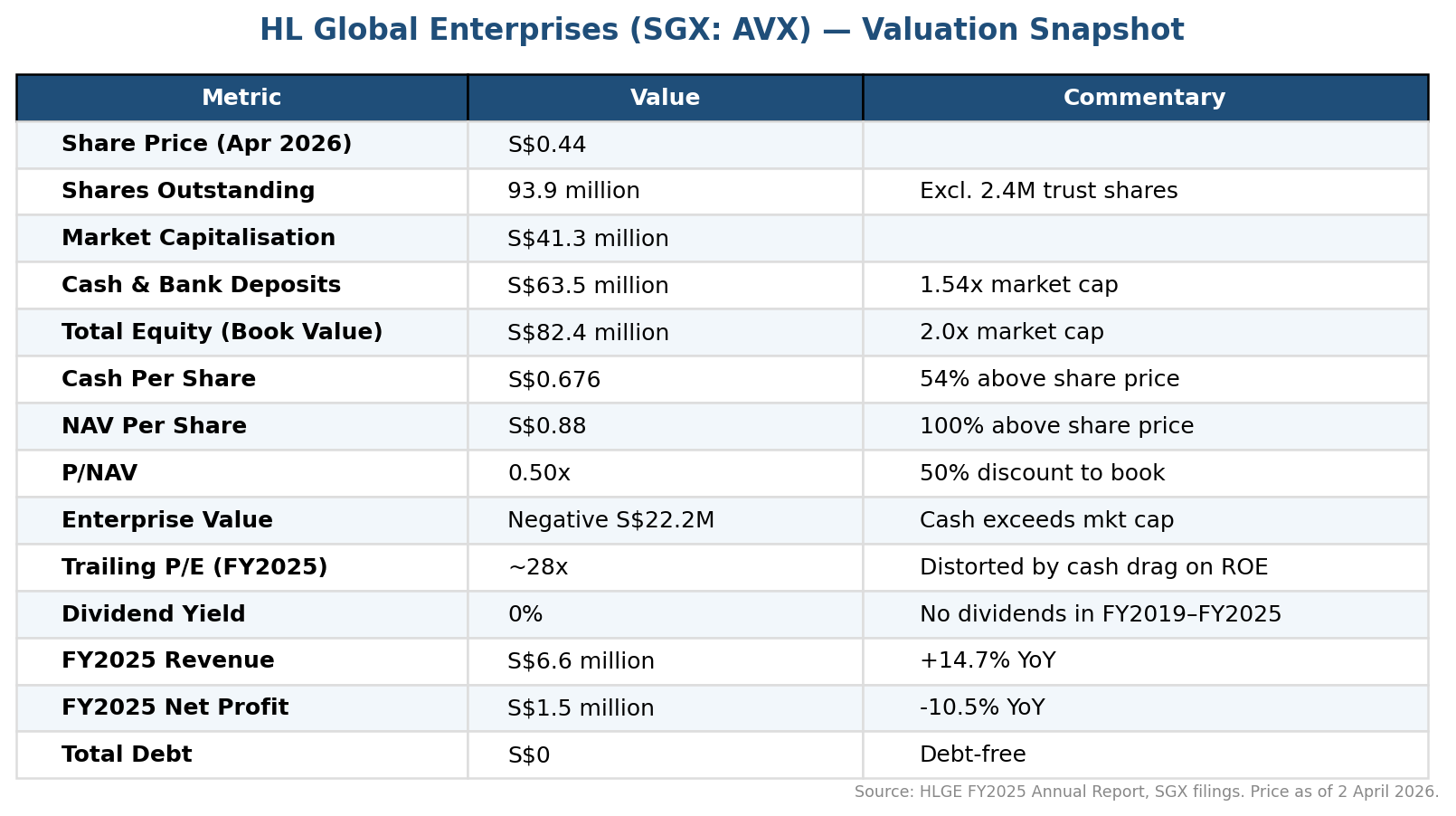

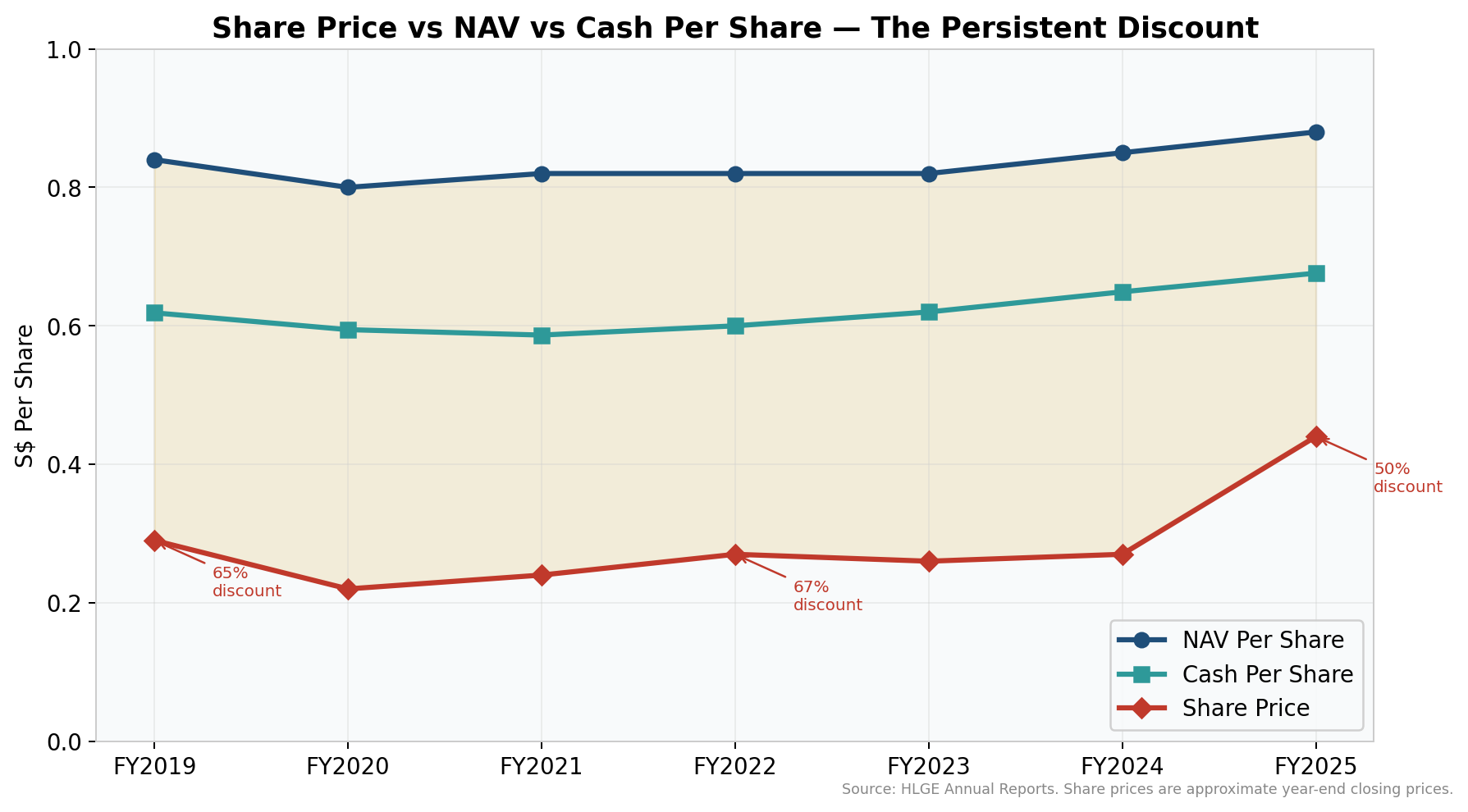

If you went looking for the most mispriced stock on the Singapore Exchange, you might stumble across HL Global Enterprises (SGX: AVX). The numbers are almost absurd in their simplicity: the company holds S$63.5 million in cash and bank deposits, carries essentially zero debt, and trades at a market capitalisation of roughly S$41 million. Cash per share alone is S$0.676, more than 50% above the current share price of around S$0.44. The stock trades at 0.50x its net asset value of S$0.88 per share. Enterprise value, by any conventional definition, is deeply negative.

On paper, this is a screaming buy. In practice, it’s considerably more complicated.

What HLGE Actually Does Today

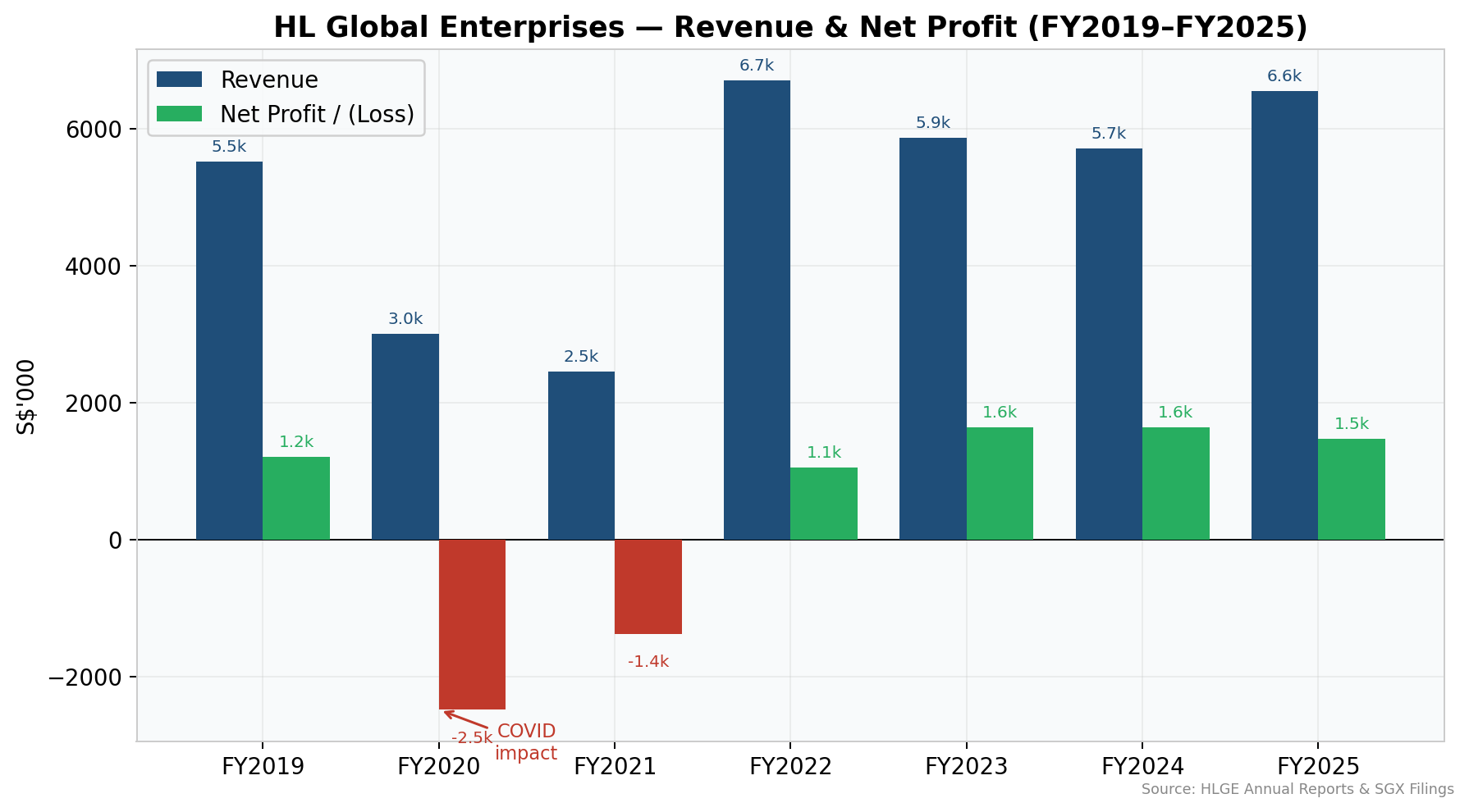

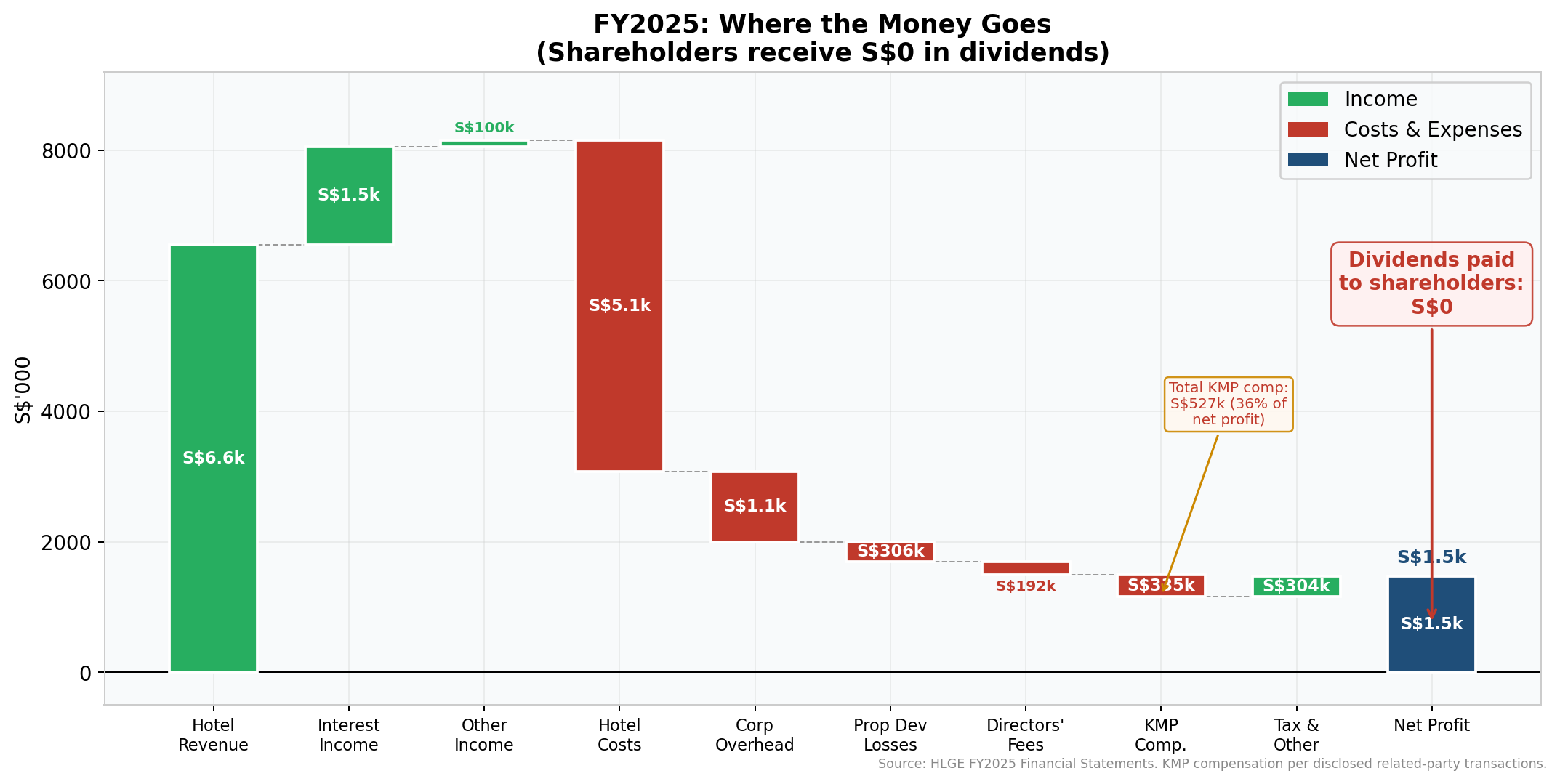

Strip away the balance sheet, and HLGE’s operating business is remarkably small. FY2025 revenue was S$6.6 million, virtually all from Copthorne Hotel Cameron Highlands, a 269-room property perched at 1,628 metres in the Malaysian highlands. The hotel earned an operating profit of S$1.5 million. The Group also holds a stalled property development in Melaka, suspended since 1998 in the wake of the Asian Financial Crisis, making it twenty-eight years of inaction, and is reviewing a tender for 48 apartment units in Kea Farm, Cameron Highlands.

Revenue has recovered from COVID lows but remains range-bound at S$5.7–6.7 million. Net profit is modest and entirely dwarfed by the cash balance.

The company does not have a CEO. It does not have an Executive Director. The Executive Committee, chaired by 79-year-old Dato’ Gan Khai Choon, explicitly states it is “not involved in the executive management of the Group’s business.” Day-to-day operations rest with two Key Management Personnel: CFO Foo Yang Hym, who joined in 1984, and hotel General Manager Tee Puat Heng. The entire listed company is run by two people who are not on the board.

This is a lean structure befitting a single-asset company, but it is also one with no strategic mandate, no growth function, and no accountability to minority shareholders for capital allocation.

How a Hotel Became a Cash Box

To understand HLGE, you have to understand its history, because the company you see today bears little resemblance to what it once was.

Founded in 1961 as Lim Kah Ngam (Singapore) Private Limited, the company spent decades building a portfolio of hotel assets across Asia under the Hong Leong Group umbrella. By the mid-2010s, HLGE was a multi-country hospitality operator generating S$13 million in annual revenue, with significant holdings including a 60% stake in Copthorne Hotel Qingdao (a 455-room deluxe hotel in China), interests in Shanghai real estate, and Elite Residences Shanghai (106 serviced apartments). The Group also managed Hotel Equatorial Shanghai, a 506-room property, through a joint venture.

But HLGE was also leveraged. It carried a S$68 million unsecured loan from Venture Lewis Limited, a subsidiary of China Yuchai International, itself a Hong Leong-related entity. The balance sheet was not the fortress it is today.

The transformation came in 2016–2017. Management decided to exit China. The Group listed its Qingdao hotel stake for sale on the Shanghai United Assets and Equity Exchange, and after initial rounds that attracted no bids, eventually completed the disposal in October 2017. One month later, HLGE sold its entire interest in LKNII, the subsidiary holding the Qingdao, Shanghai, and serviced apartment assets. The combined gain: approximately S$86.8 million.

What happened next defined the company’s trajectory for the next decade. Rather than reinvesting in new properties or distributing the windfall to shareholders, management used the proceeds to repay the S$68 million Venture Lewis loan in full. After the repayment, the residual surplus (roughly S$18–19 million) was added to existing cash balances. The company retained only one operating asset: Copthorne Hotel Cameron Highlands.

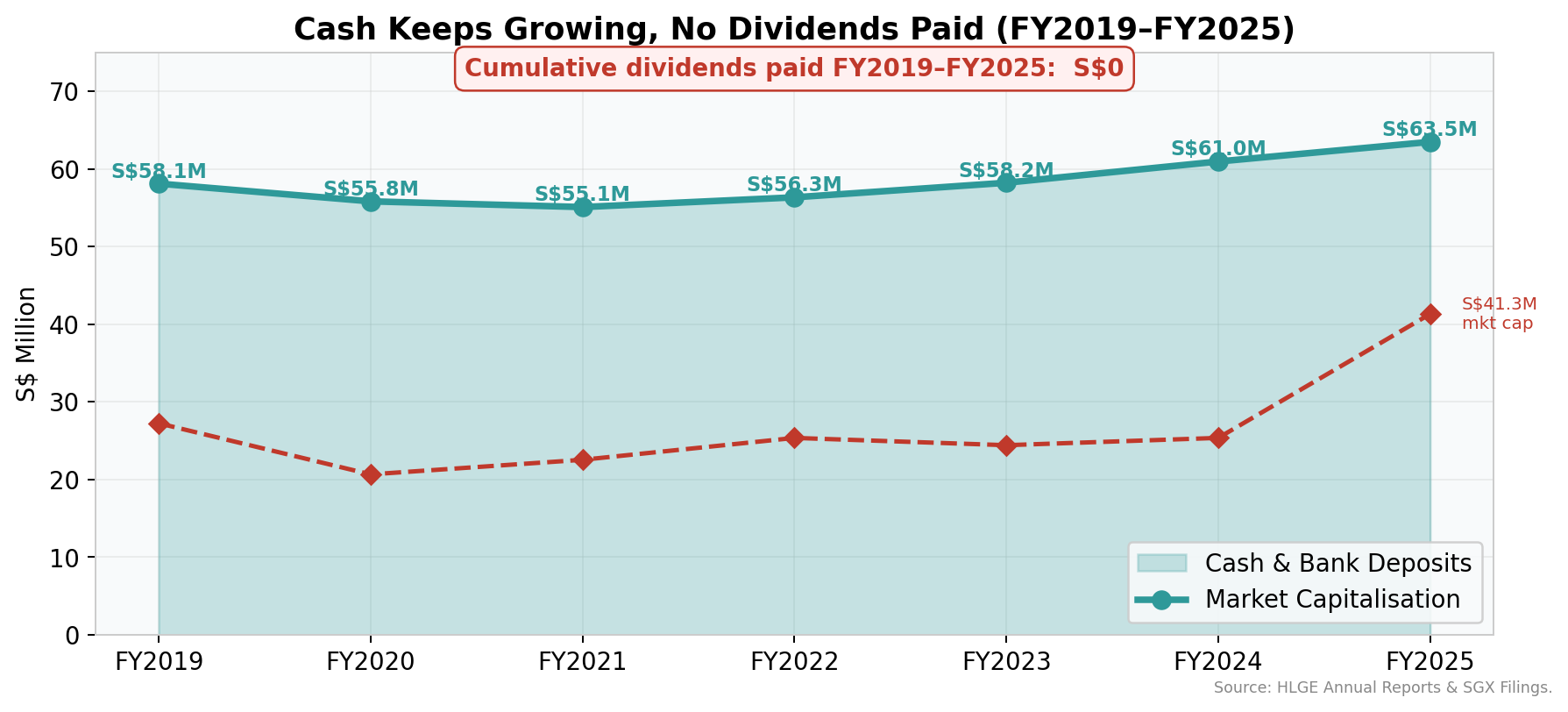

From that point forward, the cash pile has grown steadily. The hotel generates modest operating cash flow (S$2.1 million in FY2025), capital expenditure is minimal (under S$400,000 annually), and interest income on the deposits adds roughly S$1.5 million per year. No dividends have been paid in at least the past seven financial years. The result: cash balances have climbed from S$55 million in 2018 to S$63.5 million today, a quiet, relentless accumulation with no discernible purpose.

Cash has grown steadily from S$55M to S$63.5M over seven years, consistently exceeding the market capitalisation — yet cumulative dividends paid to shareholders remain at zero.

The Bull Case - And Why It’s Seductive

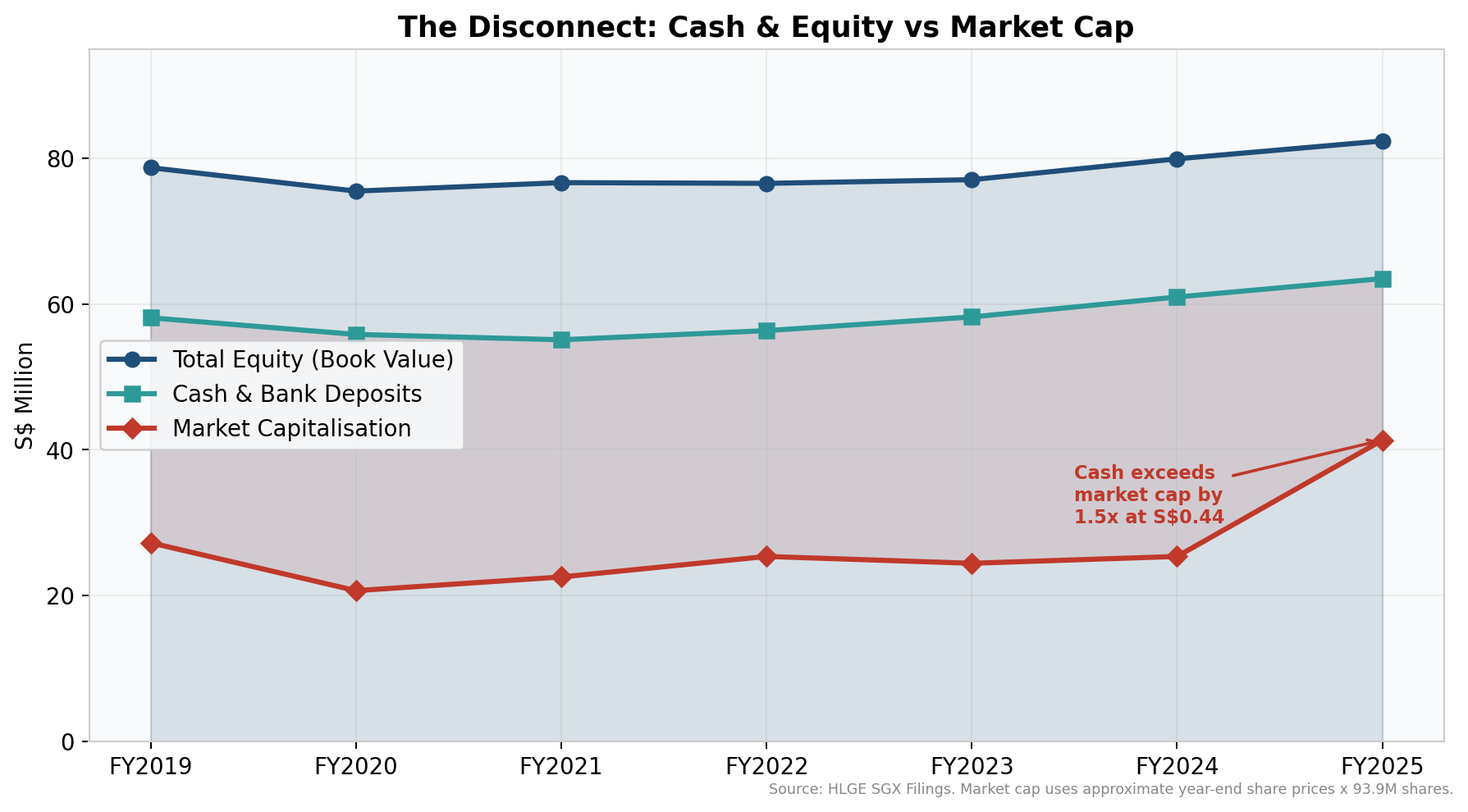

The value argument is elegantly simple. At S$0.44, you are paying S$41 million for a company holding S$63.5 million in cash, a profitable hotel, and development land. You are buying dollars for roughly 65 cents. The hotel operations come for free, or more precisely, at a negative implied value.

Total equity and cash balances have remained far above the market capitalisation for the entire period. The red-shaded gap between cash and market cap represents the discount investors are paying for every dollar of cash on the balance sheet.

The shareholder register adds to the appeal. According to the company’s FY2024 annual report, the Hong Leong Group, through a chain of entities ultimately linked to Kwek Holdings Pte Ltd and the Kwek family, holds 48.9% of issued shares, while Temasek Holdings has a deemed interest of 12.0% through DBS Group Holdings. These are not speculative punters. The backing of Singapore’s premier property conglomerate and its sovereign wealth fund lends a veneer of credibility. In November 2025, China Yuchai (another Hong Leong entity) purchased 200,000 shares at 33 cents, a purchase totalling just S$66,000, trivial for a company of that size, though it nonetheless triggered a brief run-up to 44 cents.

The bull thesis ultimately rests on catalysts: a privatisation offer from Hong Leong, a special dividend, a share buyback programme, or a meaningful deployment of the cash into value-accretive acquisitions. At the April 2025 AGM, when shareholders pressed management on the cash pile, the board cited three projects in progress — the Kea Farm apartments, the conversion of an entertainment complex into hotel rooms, and the Melaka development.

The Bear Case - And Why the Discount Persists

Every element of the bull case has a structural counterargument.

The cash is real but inaccessible. Minority shareholders cannot force a dividend, a buyback, or a liquidation. The Hong Leong Group controls the company with 48.9% and has shown no inclination to return capital. The board’s stated dividend policy is to “conserve cash for operations and future investment opportunities”, a formulation it has repeated, verbatim, for years. The market isn’t mispricing the cash; it’s correctly pricing the probability that minority shareholders will never see it.

The prestigious register is the problem, not the solution. Hong Leong’s controlling stake is what creates the value trap. They already control the company and its cash. A privatisation under the Singapore Code on Take-overs would require a premium to the prevailing market price and an independent financial adviser would likely benchmark any offer against NAV. At NAV of S$0.88 per share, buying out the 51% Hong Leong doesn’t own would cost roughly S$42 million, not the S$21 million a naive calculation at market price would suggest. Why would they spend that when the status quo already serves them? Temasek’s 12% is likely a legacy holding through DBS, too small for active management. Neither shareholder has any incentive to act as an activist catalyst.

The projects are recycled talking points. The Melaka development has been suspended since the 1998 Asian Financial Crisis. The entertainment complex conversion has been awaiting regulatory approval for years. The Kea Farm tender is being reviewed with a focus on cost reduction, suggesting the economics may not work. These are not catalysts, they are justifications for inaction, trotted out at AGMs to deflect shareholder frustration.

The hotel faces structural headwinds. Cameron Highlands is experiencing an oversupply of hotel apartments and homestays, which management itself has flagged repeatedly. Rising operating costs from Malaysia’s minimum wage increases and skilled labour shortages are compressing margins. The Hotel Equatorial Shanghai licence agreement was terminated in March 2025, eliminating a recurring income stream. CHCH is a decent hotel in a competitive market, but it has limited pricing power and no clear path to meaningful revenue growth.

Compensation absorbs a significant share of profits. Directors’ fees of S$192,000 plus total KMP compensation (employee benefits and employer CPF contributions) of S$335,000 brought total key management compensation to S$527,000 in FY2025, according to the company’s financial statements. That represents 36% of FY2025 net profit of S$1.47 million, for a company that pays nothing to shareholders. There are no performance-linked fees, no share options have ever been granted under the 2006 scheme, and no clawback mechanisms exist. The board is compensated for maintaining the status quo.

A breakdown of FY2025 economics: the hotel and interest income generate nearly S$3 million, but corporate overhead, property development losses, directors’ fees, and management compensation consume a significant portion, while shareholders receive nothing.

The Verdict: Deep Value With an Indefinite Holding Period

The share price has traded at a persistent 50–65% discount to NAV for over seven years. Even cash per share alone has consistently exceeded the stock price. The recent narrowing from a 65% discount to 50% is notable but the gap remains wide.

HLGE is not a fraud. It is not a poorly run company in the conventional sense, the hotel is maintained, the accounts are clean (audited by Ernst & Young), and the balance sheet is pristine. It is simply a company where the interests of the controlling shareholder and minority shareholders have diverged, and there is no mechanism to realign them.

The downside is well-protected. It is difficult to envision a scenario where you permanently lose capital at S$0.44 when the company holds S$0.676 per share in cash and generates positive operating cash flow. But capital protection is not the same as capital appreciation. Without a catalyst, you are buying a stock that pays no yield, offers minimal liquidity (many days see fewer than 200 shares traded), and depends entirely on the goodwill of a controlling shareholder for value realisation.

The recent price action, from roughly S$0.25 a year ago to S$0.44 today, a 76% gain, suggests some investors are beginning to pay attention. The China Yuchai share purchase and The Edge Singapore’s coverage have brought new eyes to the name. But attention alone doesn’t unlock value. What would change the thesis is a concrete action: a dividend policy, a buyback mandate, a privatisation offer, or a genuinely transformative acquisition. None of these appear imminent.

For patient, deep-value investors with a multi-year horizon and high tolerance for illiquidity, HLGE offers an asymmetric risk-reward: limited downside, potentially significant upside, but with no visibility on timing. For everyone else, it remains a fascinating case study in how a company can be simultaneously cheap on every metric and yet offer no clear path to value realisation.

The S$63.5 million sits in the bank. The question, as it has been for years, is whether it will ever find its way to shareholders.

References

All factual claims in this article are sourced from the following publicly available documents filed with the Singapore Exchange (SGX) or published by the company:

[1] HL Global Enterprises Limited, Full Year Financial Statements and Related Announcement for FY2025 (Broadcast: 13 Feb 2026). — Revenue of S$6,551k (p.1); cash & bank deposits of S$63,481k (p.2); net cash from operations S$2,071k (p.4); capex S$303k (p.6); interest income S$1,499k, Note 6 (p.9); directors’ fees S$192k, Note 7 (p.9); KMP employee benefits S$313k and CPF S$22k, Note 8 (p.9); Melaka development suspended since 1998, Note 12 (p.12); no share options granted under SOS 2006, Note 14 (p.13).

[2] HL Global Enterprises Limited, Annual Report 2025 (FY ended 31 Dec 2025). — Hotel description: 269 guestrooms, 1,628 metres elevation (p.8); Dato’ Gan Khai Choon, age 79, Chairman Non-Executive (p.4); Ms Foo Yang Hym joined 1984 (p.7); Executive Committee not involved in executive management (p.1); Ernst & Young LLP as auditor (p.1); Hotel Equatorial Shanghai licence terminated effective 1 March 2025 (p.2); hospitality segment operating profit S$1.5 million (p.2); Kea Farm 48 apartment units, reviewing tender with aim to reduce development costs (p.3); entertainment complex conversion pending regulatory approval (p.3); no dividend recommended, cash conserved for operations and future investment (p.2).

[3] HL Global Enterprises Limited, Annual Report 2024 (FY ended 31 Dec 2024). — Substantial shareholders: Grace Star Services (48.90% direct), chain of deemed interests through Hong Leong entities to Kwek Holdings Pte Ltd; Temasek Holdings 11.98% deemed interest through DBS Group Holdings (Analysis of Shareholdings section); issued shares 93,915,337 excl. 2,418,917 trust shares.

[4] HL Global Enterprises Limited, Annual Report 2017. — Gain of S$86.8 million from the LKNII and Qingdao disposals (Chairman’s Statement); completion of CHQ disposal Oct 2017 and LKNII disposal Nov 2017.

[5] HL Global Enterprises Limited, Annual Report 2015. — S$68 million unsecured loan from Venture Lewis Limited (Chairman’s Statement, p.5); Copthorne Hotel Qingdao 60% stake, 455 guestrooms (p.2); Elite Residences Shanghai 106 apartment units (p.2); Hotel Equatorial Shanghai 506 guest rooms (p.3).

[6] HL Global Enterprises Limited, Annual Report 2018. — Repayment of S$68 million Venture Lewis loan from disposal proceeds; founding as Lim Kah Ngam (Singapore) Private Limited in 1961.

[7] “Our 2026 Picks: HL Global Enterprises — Undervalued Despite Big Names”, The Edge Singapore (Dec 2025). — China Yuchai purchase of 200,000 shares at 33 cents average in November 2025.

[8] SGinvestors.io, HL Global Enterprises Share Price History (SGX:AVX), accessed April 2026. — Historical share price data; S$0.44 as of 2 April 2026; approximately S$0.25 level in April–May 2025.

[9] HL Global Enterprises Limited, Annual Reports FY2019–FY2024 (SGX filings). — Historical revenue, net profit, cash balances, total equity, and NAV per share data used in charts and trend analysis across all seven fiscal years.

IMPORTANT DISCLAIMERS

General Disclaimer: This article is published for informational and educational purposes only. It does not constitute financial advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The views expressed are based on publicly available data from HL Global Enterprises’s SGX filings and publicly accessible market data, and may not reflect the most current developments.

Not Licensed Financial Advice: The author is not a licensed financial adviser, and this publication is not issued by a holder of a Capital Markets Services Licence under the Securities and Futures Act 2001 of Singapore. This content does not fall within the definition of “financial advisory service” under the Financial Advisers Act 2001 of Singapore. Readers in Singapore should note that this content is exempt from the requirements of the Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication.

MAS Compliance Notice: In accordance with the Monetary Authority of Singapore’s guidelines, this publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, you should consult a licensed financial adviser who can provide advice tailored to your personal circumstances. Past performance of any security discussed herein is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author may or may not hold positions in the securities discussed. No compensation has been received from any company mentioned in this article.

Data Sources: HL Global Enterprises SGX filings, public market data from SGX, Yahoo Finance, and Bloomberg as of April 2026.

The SEA Analyst, thanks for your analysis of HL Global Enterprises Limited (AVX; HLGE SP).

Without a path to growth or capital returns, minority shareholders may wait forever for the discount to close.

This reminded me of Haw Par, which both of us analysed too.

I first invested in Haw Par Corporation Limited (H02; HPAR SP) in Feb 2021. I was attracted to its inorganic growth potential, which I believed the market had not fully recognized.

Through reading management interviews and analysing its hiring activity, I believed Haw Par was about to make a major acquisition. This could increase its profits by almost 50%.

I also believed the market had not fully recognized the ‘hidden’ assets within H02. Its accounting policies have artificially depressed its return on asset (ROA), making it look like a low-return business.

More than 5 years later, I sold all my shares.

H02 still has not made any significant acquisitions. There is no convincing evidence it will do so any time soon.

The hidden assets I saw in H02 remain hidden. I now believe these hidden assets will unlikely ever be unlocked and returned to shareholders.

Furthermore, I believe the outlook for Tiger Balm is bleaker than the market expects.

I discuss the details here: https://angsanaanderson.substack.com/p/haw-par-right-for-the-wrong-reasons?r=5rl2u5

No liquidity