Sheng Siong Group: The Price of a Forty-Year Compound

Dividends every year since 2011, 31x earnings, and S$435 million in net cash. Inside Singapore's quietest compounder.

If you live in Singapore, you have almost certainly walked through a Sheng Siong store. There are eighty-seven of them on the island, anchoring Housing and Development Board (HDB) estates and neighbourhood malls from Yishun in the north to Pasir Ris in the east. The company’s tagline, “Always By Your Side”, captures the philosophy in three words: be the trusted neighbourhood store that ordinary Singaporean households can rely on for daily essentials, week after week.

The company name itself tells part of the story. In Chinese characters, Sheng Siong is written 昇菘, where 昇 (sheng) carries the sense of “to rise” or “to prosper” in Mandarin, and 菘 (siong) is a classical name for the Chinese leafy-green vegetable family that includes bok choy and Chinese cabbage. It is a fitting label for a chain whose founding identity was anchored in fresh produce. Founders Lim Hock Eng, Lim Hock Chee and Lim Hock Leng started the business in 1985, after working in their family’s hog-rearing trade [13], and over forty years built it into a chain whose stated mission has not really shifted: deliver value-for-money daily essentials to heartland families, especially residents of HDB estates, with quality products at competitive prices.

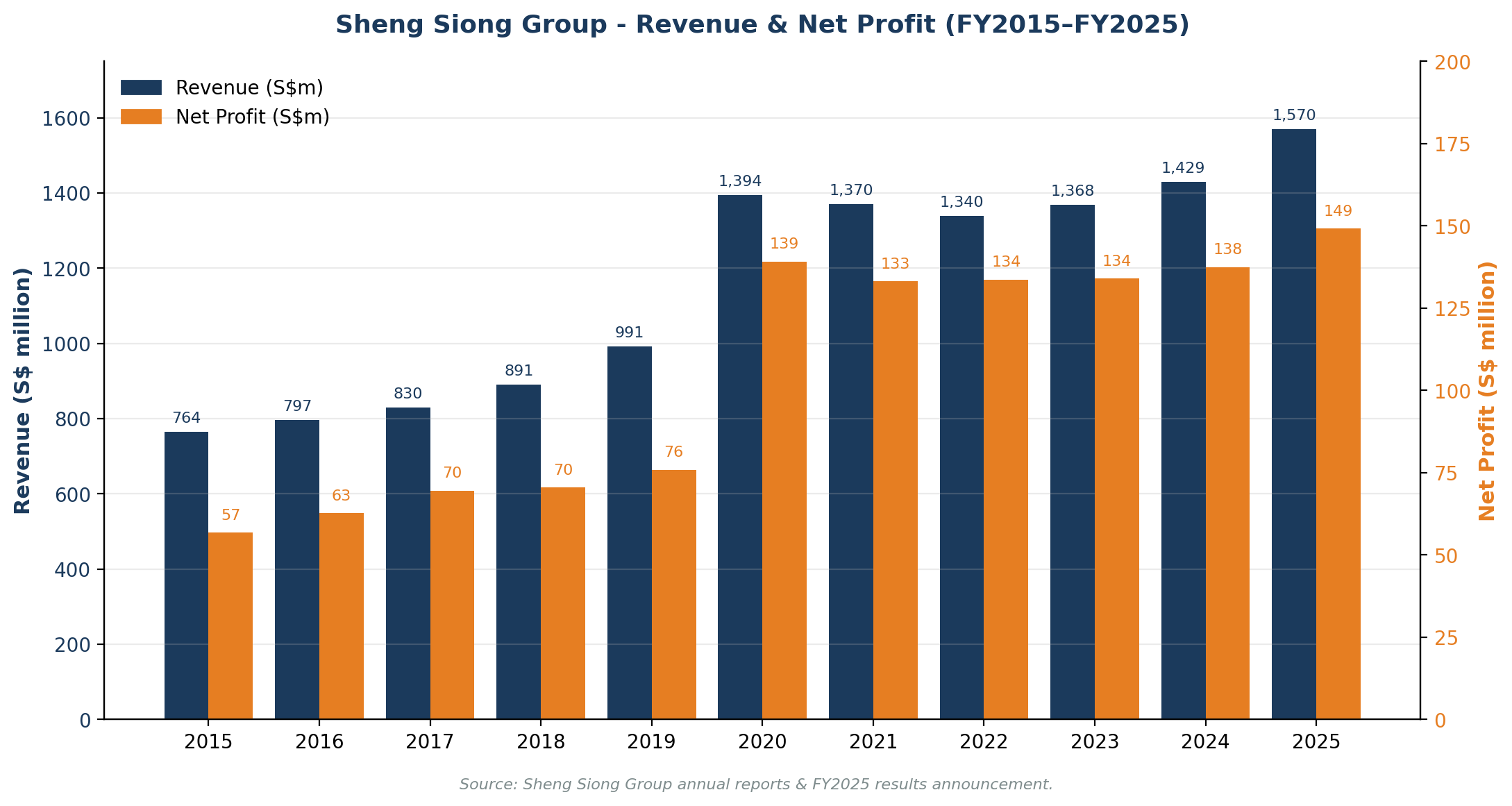

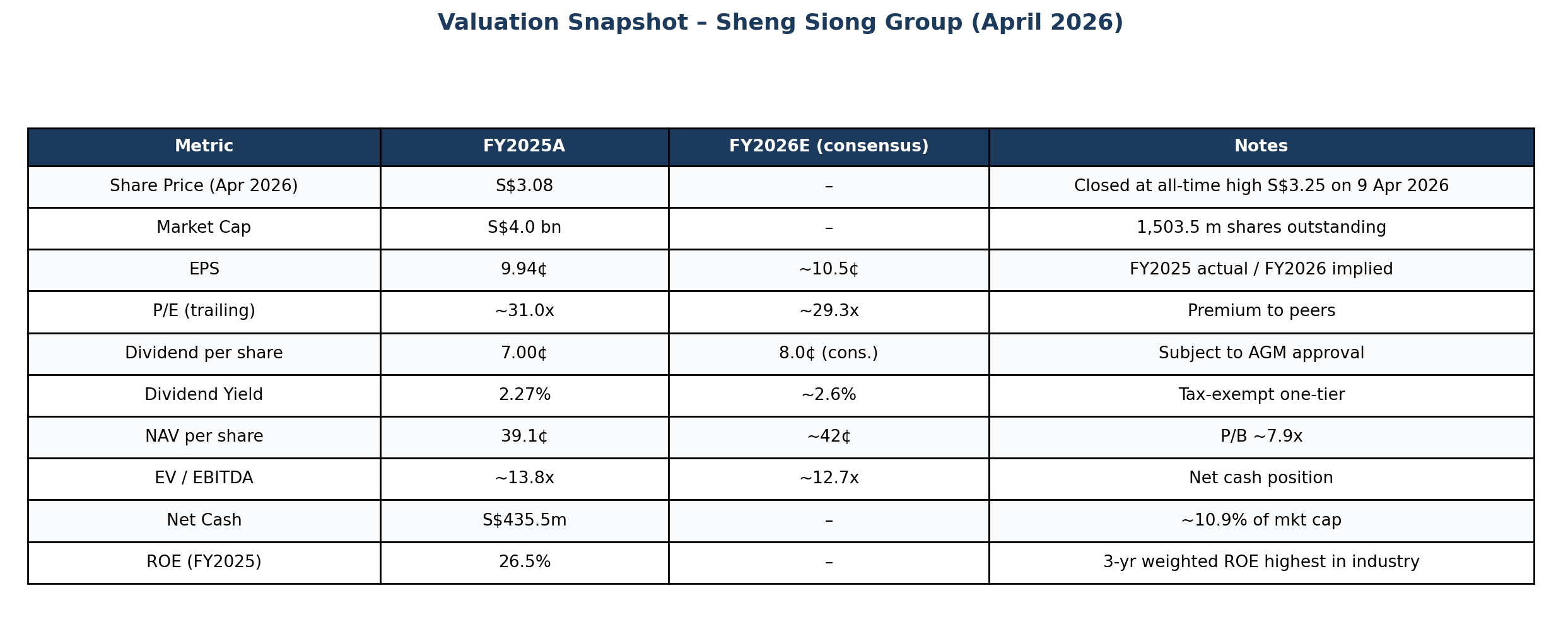

What most people have not done is looked at the company itself as an investment. Sheng Siong Group Ltd. (Singapore Exchange ticker: OV8) is today the third-largest supermarket chain in Singapore, listed on the Singapore Exchange (SGX) Mainboard in August 2011. In its FY2025 financial year ended 31 December 2025, the Group generated S$1.57 billion in revenue and S$149.2 million in net profit, finished the year with S$435.5 million in cash and zero conventional debt, and paid 7.0 cents per share in dividends, a fresh record.

At the share price of roughly S$3.08 in late April 2026, the company carried a market capitalisation of approximately S$4.0 billion [1], placing it just inside Singapore’s mid-cap index neighbourhood. The numbers behind that headline are quietly extraordinary. The story behind those numbers, and whether that story is already fully discounted, is what this article tries to unpack.

A Forty-Year Journey: From Pork Stall to S$4 Billion Grocer

Sheng Siong’s origin is a textbook Singapore growth story. Brothers Lim Hock Eng, Lim Hock Chee and Lim Hock Leng worked in their family’s hog-rearing business before founding the chain in 1985 [13]. The early decades were unglamorous. The chain ground out store-by-store growth, leaning on direct sourcing relationships, value pricing, and a “wet-and-dry” format that combined live seafood, fresh produce and packaged groceries under one roof. It was the format Singaporean heartlanders had grown up with in traditional wet markets, simply put under the air conditioning of a supermarket anchored to a Housing and Development Board (HDB) estate.

The Initial Public Offering (IPO) on the SGX Mainboard in August 2011 marked the first inflection. With listing proceeds and operating cash flow, the Group built a purpose-built central headquarters and distribution centre at Mandai Link, which has anchored Singapore operations ever since. Online grocery followed in 2014, later rebranded as “Sheng Siong Online” in 2021, and a tentative move overseas opened a first store in Kunming, China in 2017.

The next inflection was COVID. Stockpiling drove revenue from S$991 million in FY2019 to S$1.39 billion in FY2020, and net profit jumped 84% to S$139 million in a single year. Investors who treated this as a new run-rate were modestly disappointed when revenue normalised slightly lower in FY2021 and FY2022. The retreat, however, was shallow: total revenue dipped only about 4% off the FY2020 peak, and profit dipped about 4% in FY2021 before re-stabilising. There has not been a year since the IPO when Sheng Siong failed to make money or skipped a dividend.

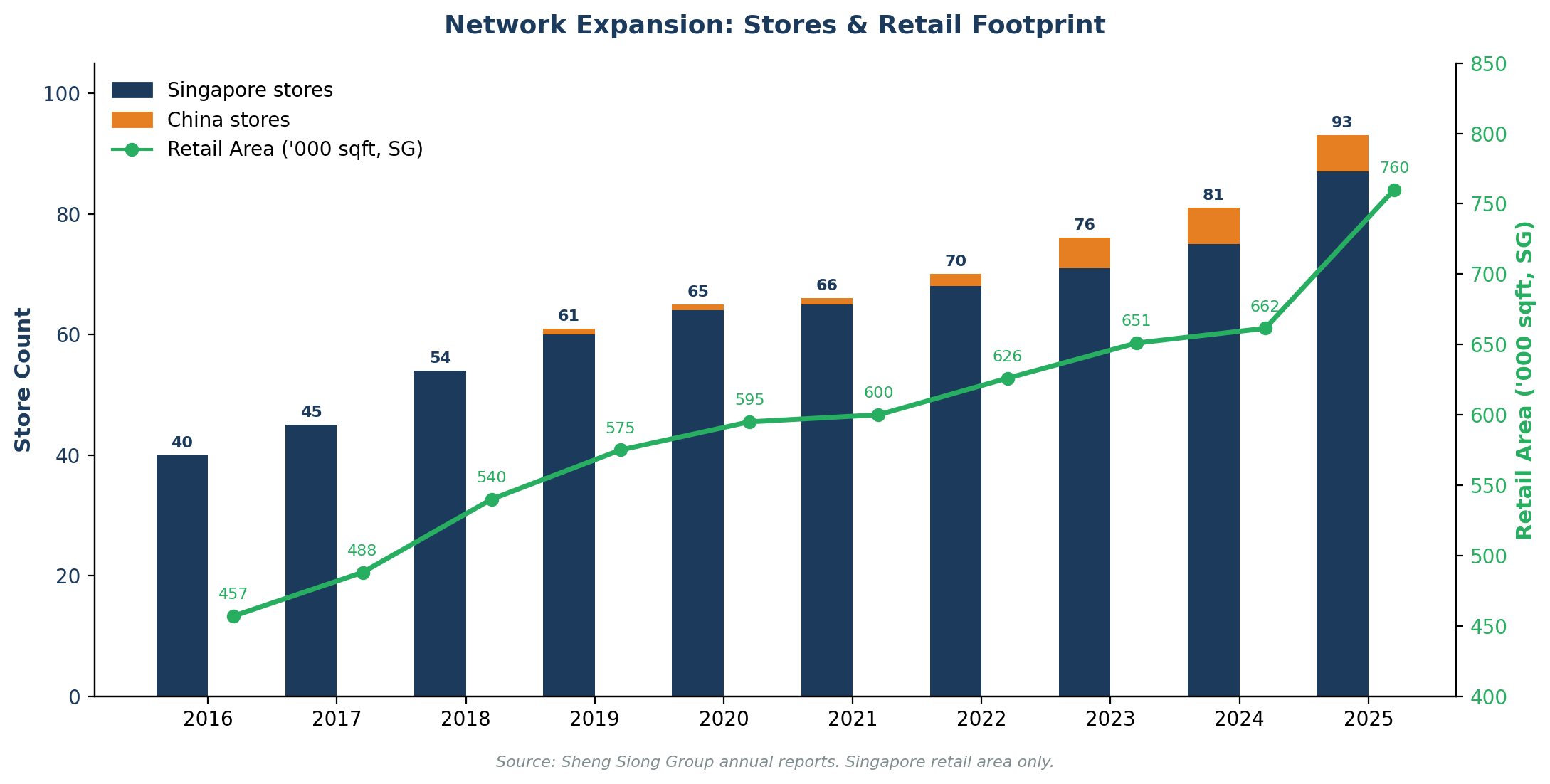

The most aggressive year in the Group’s listed history is the most recent one. In FY2025 the Group opened twelve new stores in Singapore, comfortably above the long-run guidance of three to five per year, and accepted an offer from JTC Corporation (the government-linked industrial real estate developer) to develop a new central distribution centre at Sungei Kadut. The new distribution centre is expected to be operational around 2029 or 2030, and is sized to support at least 120 stores. As part of the deal, the Group must sell or assign the existing Mandai Link property to a buyer approved by JTC Corporation, which triggered a S$2.2 million gain on lease modification recorded in the FY2025 results. In late 2024 the Group also acquired Jelita Property Pte Ltd for S$49 million, securing freehold investment property and a flagship store location. That was the only material corporate deal in years.

What Sheng Siong Actually Does

Sheng Siong reports as a single operating segment: supermarket retail of consumer goods. The simplicity is a feature of the thesis, not a bug. The Group makes its money in four reinforcing ways. The first is direct sourcing and house brands. As of the latest annual report, the Group carries 2,035 stock-keeping units (SKUs) across twenty-eight house brands, including Tasty Bites, Heritage Farm, HomeNiks, Phizz and Happy Family, which both expand gross margin and provide a defensive lever when consumers downtrade. The second is a heartland store rollout where most outlets sit in HDB estates whose rents are tendered through HDB and JTC Corporation processes, structurally cheaper than central business district or shopping mall locations. That said, the FY2025 openings of stores at Leisure Park Kallang and at The Cathay (the Group’s first Orchard Road outlet) demonstrate that the chain can also operate centrally when the rent maths works. The third is a centralised supply chain anchored by the Mandai Link distribution centre, soon to be replaced by Sungei Kadut. The fourth is a still-small but growing online and quick-commerce channel through Sheng Siong Online and the Sheng Siong app, supplemented in early 2025 by a quick-commerce partnership with Deliveroo.

Geographic exposure is overwhelmingly Singapore. The domestic market generated approximately 97.6% of FY2025 revenue, with six stores in Kunming, China contributing the remaining 2.4% and recording a small net deficit for the year amid intense local competition. A long-dormant Malaysian subsidiary remains inactive. The more revealing point is that the Group has not used this dormant subsidiary to make any move into Malaysia despite eight years of cross-border opportunity, even as the Group expanded steadily in Singapore over the same period. If the easiest adjacent market on Sheng Siong’s doorstep has not been pursued, the message about how rigorously the Group screens overseas opportunities is a clear one. The China presence, in turn, is best read as a small, low-capital test lab rather than a regional growth engine. For practical purposes, Sheng Siong is a pure-play Singapore consumer staple, with optional overseas upside that management has deliberately kept on a short leash.

Industry: A Defensive Triopoly Reshaped by Consolidation

Singapore’s grocery retail market is approximately US$36 billion in size and has historically been dominated by three players [3, 5]. The largest is NTUC FairPrice, the cooperative chain with over 370 outlets and a market share above 40%. The second, until very recently, was DFI Retail Group’s Singapore food business, the operator of Cold Storage, CS Fresh, Jason’s Deli and Giant. The third has been Sheng Siong, the heartland-value challenger. Below this top three sit smaller players such as Prime, Mustafa and Don Don Donki, which collectively occupy a single-digit share. The category itself is famously defensive: Singapore consumers buy groceries through inflation, recession, war and pandemic, with relatively low elasticity of demand.

Consolidation: DFI’s Exit and What It Means

The most significant change in the competitive landscape in years is happening right now. In March 2025, DFI Retail Group announced the divestment of its entire Singapore food business (48 Cold Storage, CS Fresh and Jason’s Deli stores, 41 Giant stores, and two distribution centres) to Macrovalue, a Malaysian-headquartered retail conglomerate, for an initial consideration of S$125 million [12]. The transaction was expected to close in the second half of 2025. DFI’s stated rationale was straightforward. In 2024, the food segment had a segment operating margin of just 1.8%, against 8.6% for its Health & Beauty (Guardian) business and 4.3% for Convenience (7-Eleven) [12]. The same Macrovalue group acquired DFI’s Malaysian food business in 2023, so the buyer is a known operator stepping into a familiar role rather than a financial sponsor with no retail track record.

For Sheng Siong, the implications run on two timeframes. In the short term, any ownership transition creates operational disruption, including staff turnover, supplier renegotiations, and customer churn during repositioning, and the most natural beneficiary of marginal customer outflow is the next-cheapest heartland alternative, which is Sheng Siong. In the medium term, the competitive picture depends on Macrovalue’s execution: a sharper, more focused regional owner could revitalise Cold Storage and Giant in ways that DFI did not, in which case the threat moves the other way. The transition also subtly recalibrates the league table. With Sheng Siong at eighty-seven Singapore stores and the former DFI portfolio at eighty-nine, what used to be a clear hierarchy is now a near-tie at the number-two spot by store count, and Sheng Siong already exceeds the former DFI Singapore food business in profitability by a wide margin.

Structural Tailwinds: Aging, Vouchers, Cost-of-Living

The macro backdrop in 2025 was supportive in a specific way. The Monetary Authority of Singapore (MAS) Core Inflation averaged 0.7% in 2025, moderating sharply from 2.8% in 2024, but consumers continued to skew towards value-driven shopping. That dynamic plays directly into Sheng Siong’s positioning. MAS now projects core inflation in a 1–2% range for 2026, slightly higher but still benign, while the Ministry of Trade and Industry (MTI) forecasts 2026 Gross Domestic Product growth in the 2.0–4.0% range [4].

Beyond the cyclical picture, three structural tailwinds matter more for the next decade than any single year’s GDP print. The first is Singapore’s aging population. The proportion of residents aged sixty-five and over is rising steadily and is projected to reach roughly one in four by 2030 [14], a demographic profile that broadly suits a chain of nearby, value-priced stores embedded in residential estates. The implication is two-sided. Demand for staple groceries becomes more stable and more recession-resistant, but the absolute growth rate of grocery spending per capita is unlikely to accelerate sharply because older households generally consume at lower volumes than younger families. Net-net the aging shift looks supportive for Sheng Siong’s positioning, even if it does not lift overall category growth on its own.

The second tailwind is government cost-of-living support. Budget 2026 voucher schemes, Community Development Council (CDC) vouchers redeemable at participating supermarkets, and the Progressive Wage Credit Scheme (PWCS) all act to channel discretionary spending into the supermarket channel and to underwrite consumer purchasing power in a way that disproportionately benefits value-positioned chains. The third tailwind is population growth and the HDB pipeline itself. Every new HDB estate is a tendered store opportunity, and the Singapore government’s ongoing residential build-out is the single largest organic source of new addressable square footage for Sheng Siong over the next decade.

Structural Headwinds and Slow-Burn Risks

The headwinds are tangible too. Singapore’s labour market is structurally tight, and aging works in the opposite direction here. A smaller working-age population means a tighter retail workforce. The Progressive Wage Model (PWM) for the retail sector is phasing in further wage increments, with Sheng Siong raising retail workers’ salaries again in September 2025 to comply with the PWM. The Beverage Container Return Scheme (BCRS) begins on 1 April 2026, adding incremental compliance complexity and modest cost pass-through.

Quick commerce and electronic grocery (RedMart, Grab, and the e-commerce build of FairPrice) is best understood as a slow-burn risk rather than an immediate disruption. Online does eat into small, frequent, dry-grocery purchases and is more relevant to younger consumers, but it is structurally weak in fresh produce (where customers still want to choose what they buy), expensive to run on a per-order basis given Singapore’s high last-mile costs, and disproportionately less relevant to the older heartland shopper who is overrepresented in Sheng Siong’s footfall. The likely path is gradual erosion at the margin rather than a step-change, and Sheng Siong’s online and app channels are themselves growing in absolute terms.

The Johor Bahru–Singapore Rapid Transit System (RTS) Link, scheduled to commence operations in late 2026 or early 2027, may divert some price-sensitive grocery spending across the Causeway. The impact is hard to size in advance, and management has acknowledged the uncertainty publicly. It is worth noting that grocery shopping is mostly a local, repeat-frequency activity, so cross-border shopping is unlikely to be daily behaviour even at the most price-sensitive end. There is also a possible offset on the labour side: easier cross-border movement could marginally ease the supply of retail workers, partially offsetting the wage-cost ratchet.

Cost pressure beyond labour is the final piece. Singapore imports a very high share of its food, which makes the supermarket channel structurally exposed to global commodity volatility and to currency translation, particularly against the US dollar for protein and grains and against regional currencies for fresh produce. Sheng Siong does not disclose a detailed foreign-exchange hedging policy, but the income statement does show meaningful unrealised exchange gains and losses on US-dollar-denominated fixed deposits in different years. Investors should treat input-cost and currency volatility as a normal feature of the business rather than a one-off risk.

The Moat: Cost, Convenience, Habit (and Where the Defences Thin)

Sheng Siong’s moat is not a single feature but a stack of overlapping advantages, most of which are anchored in consumer behaviour rather than in technology or ecosystem effects. Each one is individually shallow; layered together they are surprisingly durable.

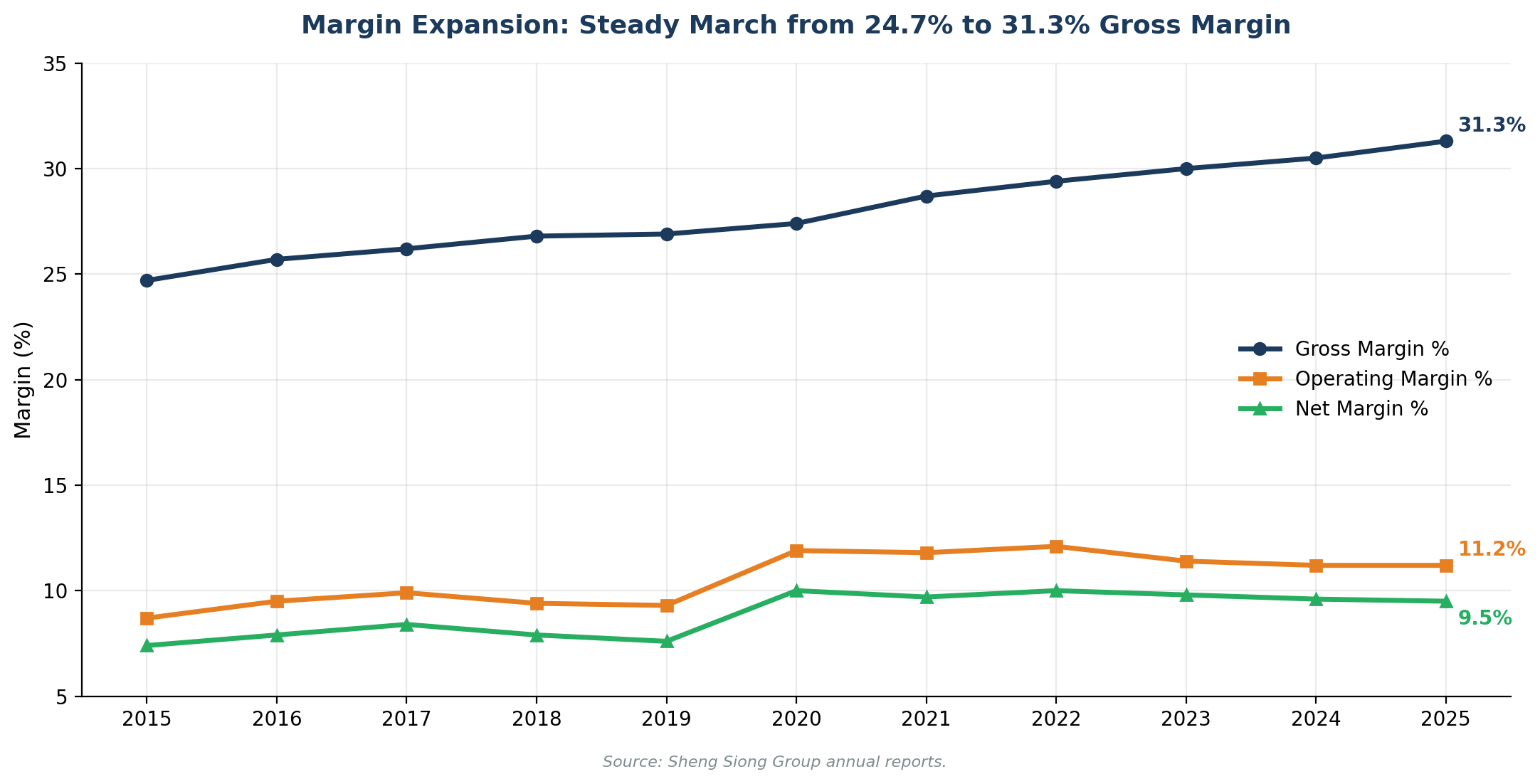

The most foundational layer is cost leadership. Forty years of direct-sourcing relationships, a house-brand catalogue of 2,035 SKUs across twenty-eight brands, and a low-cost central distribution centre at Mandai Link give Sheng Siong a structural cost position that allows it to price below premium peers like Cold Storage and still expand gross margin. The proof is in the multi-year track record. Gross margin has climbed from 24.7% in FY2015 to 31.3% in FY2025 without any pricing-power moves that would have alienated value-seeking shoppers, and that path is the single hardest piece of the moat to replicate. Catching up requires either decades of supplier-relationship building or a willingness to subsidise pricing for a long period, neither of which is rational for a competitor with shareholders.

The second layer is location in the HDB heartlands. Most Sheng Siong outlets sit inside or beside HDB estates, embedded in the residential fabric of the city. In groceries, the rule of thumb is that the nearest acceptable option wins, because the basket is small, the trip frequency is high, and convenience compounds over many small purchases. HDB grocery slots are tendered competitively, but once secured a store anchors a community for years and is rarely displaced. Many Sheng Siong outlets have stood at the same address for over a decade, building footfall habits that are genuinely sticky. The recent FY2025 openings at Leisure Park Kallang and at The Cathay (the Group’s first Orchard Road store) demonstrate the chain can also operate centrally when the rent maths works, but the heart of the moat remains the heartland.

The third layer is fresh-food strength. Sheng Siong’s “wet-and-dry” format combines live seafood, fresh meat, fruits and vegetables under the same roof as packaged groceries. It is the format Singaporean shoppers grew up with in traditional wet markets, simply ported into air-conditioned stores anchored to HDB estates. Fresh-food shopping is the part of the grocery trip that is hardest for online players to displace, because customers want to see and choose what they buy, particularly for fish and produce. Pure-play online grocers like RedMart, and the e-commerce build of the FairPrice Group, have made meaningful inroads in dry packaged categories where the customer is comfortable trusting the picker, but fresh remains a category where physical store experience is genuinely preferred. The fresh-food layer is also a partial defence against premium grocers like Cold Storage, whose fresh selection is positioned at materially higher price points and whose customer base does not overlap with Sheng Siong’s heartland shoppers.

The fourth layer is operational excellence and inventory discipline. Sheng Siong’s negative-working-capital model is partly behavioural (high inventory turnover, disciplined replenishment, low spoilage) and partly structural, because the central distribution centre at Mandai Link is the single physical asset that lets all of these efficiencies compound. Each marginal improvement in inventory days, shrink rate or supplier terms flows directly to operating cash flow, because the company is not re-investing capital to grow at the same time. Free-cash-flow conversion above 90% in FY2025 is a downstream readout of this discipline rather than an accident of any single year. The new Sungei Kadut distribution centre, sized to support 120-plus stores and expected operational by 2029 or 2030, is a deliberate decision to lift this layer further over the long run, even though it will visibly compress reported free cash flow during the build period.

The fifth layer is the value positioning and habit moat. After four decades of consistent messaging, Sheng Siong’s mental shortcut among Singaporean consumers is “cheap and reliable.” That is a durable consumer asset that is hard to value precisely but easy to underestimate. Loyalty programmes from competitors (yuu Rewards Club at DFI Retail, covering Cold Storage and Giant, and LinkPoints at FairPrice) exist and have meaningful enrolment, but they have not noticeably disrupted Sheng Siong’s customer base. The reason is structural rather than tactical: the price gap on a weekly grocery basket is typically larger than the points value redeemable through any rewards programme, and convenience matters more than points to most heartland shoppers. The implicit habit of defaulting to Sheng Siong without re-evaluating each visit is the moat that consumer-staples investors recognise instinctively but that does not show up in any single financial metric.

Beneath these five consumer-facing layers, two further moats sit at the company level rather than the customer level. The first is founder-operator alignment, which is rare among SGX-listed mid-caps. All three Lim brothers remain on the board, with deemed beneficial interests of 44.5%, 44.8% and 46.4% respectively. CEO Lim Hock Chee is in his late sixties and still hands-on, and the second generation has been seeded into operating roles since 2024. Lin Ruiwen sits on the main board, while Lin Yuansheng, Lin Junlin and Lin Zikai serve as directors of the operating subsidiary Sheng Siong Supermarket Pte Ltd. The second is the balance-sheet moat: S$435 million in net cash representing roughly 10.9% of market capitalisation, and zero conventional debt, which give the Group countercyclical optionality that few global grocery peers can match.

Where the Moat Is Weaker

It is just as important to be clear about where the defences thin out. The first weak spot is technology and electronic commerce. Sheng Siong’s online and quick-commerce footprint remains modest, and the Deliveroo Singapore partnership launched in early 2025 hit an unforced setback when Deliveroo announced it would cease Singapore operations. Pure-play online grocers like RedMart, and FairPrice’s own e-commerce build, have invested more aggressively in the digital experience and in last-mile fulfilment. Sheng Siong’s app and online channels are growing, but they are following rather than leading.

The second weak spot, depending on how you read it, is overseas scalability, and this one deserves a more careful framing than a simple line. The advantages that work in HDB Singapore (heartland location, low-cost central distribution, deep local supplier relationships) do not travel well, and the six-store presence in Kunming reflects how hard it is to replicate the formula in unfamiliar real-estate, supply-chain and consumer-behaviour environments. The important nuance is that this is largely a deliberate strategic discipline rather than a managerial inability. Management’s stated approach is to expand overseas only where the Group can credibly replicate its edge, and so far it has assessed that neither Malaysia nor most of China clears that bar. Malaysia, in particular, is the strongest signal. A dormant subsidiary is sitting one Causeway away from the Singapore base, and management has actively declined to revive it because the supply chain is more complex and the cost advantage that anchors the Singapore model is absent in the Malaysian retail market. The trade-off is that Sheng Siong is, by its own choice, capping its addressable market at Singapore plus a small China test lab. The growth ceiling is real even if the discipline is laudable, which is precisely the tension this article keeps coming back to.

The third weak spot is switching costs. There are essentially none. Customers can walk into any other supermarket without friction, and any sustained price war from a deeper-pocketed competitor would force Sheng Siong either to follow it down or watch traffic erode. So far the value gap has been wide enough, and competitor margins thin enough, to insulate the chain from this scenario, but it is a permanent rather than a one-off vulnerability.

Stepping back, the durability ranking matters more than the count. The cost-leadership and value-positioning layers are the most defensible, because both compound through repeat consumer behaviour rather than through capital expenditure. The fresh-food and location layers are nearly as durable but are exposed to slow shifts in consumer preference (more delivery, and from late 2026 more cross-border shopping via the RTS Link to Johor) and in real-estate cycles (HDB tender renewals). The operational-excellence layer is durable and self-reinforcing, but the new distribution centre capex cycle will narrow its visible benefit during the build period. The founder-operator and balance-sheet moats are the ones that change most over the next five to ten years, because family succession will be tested and net cash will fall as Sungei Kadut is funded. None of this is flashy. It is built on cost, convenience and consumer habit, not on technology, network effects or ecosystems. Whether that combination is enough at the price the market is asking today is the question the rest of this article tries to address.

Ten-Year Financial Scoreboard

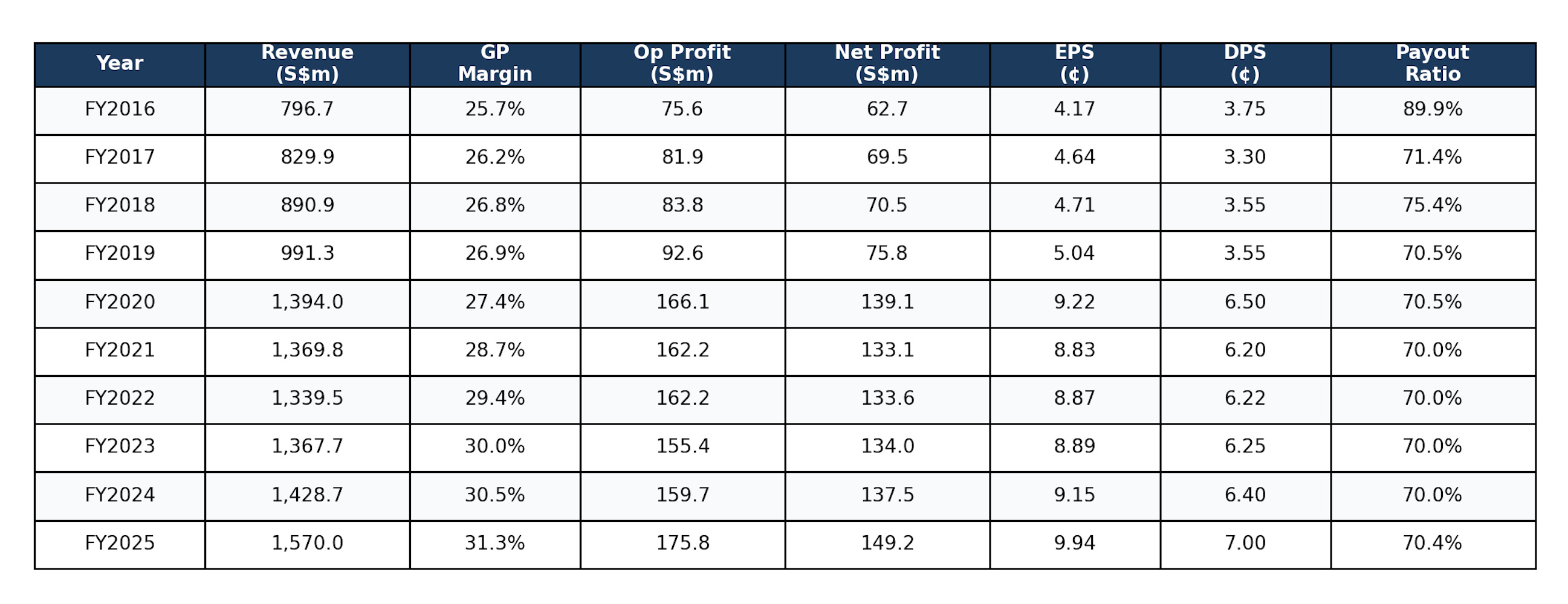

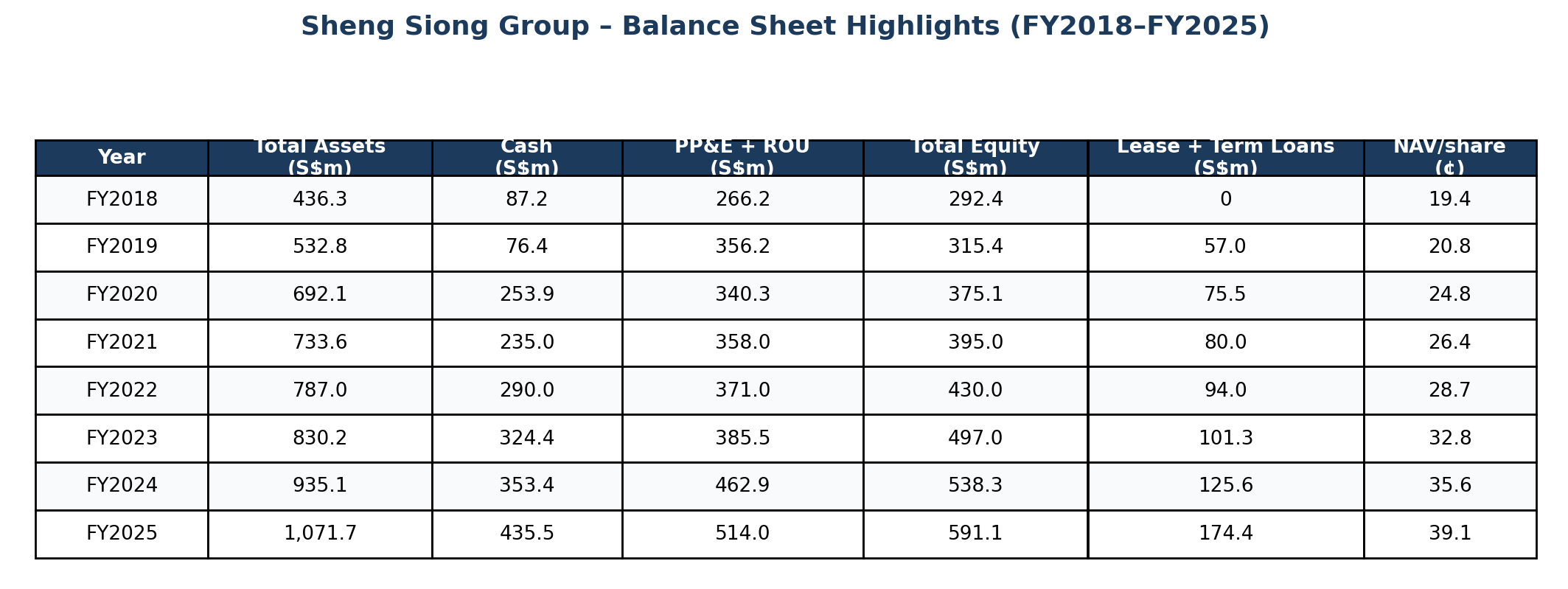

A few features stand out in the long-run track record. Revenue compounded at roughly 7.5% per year from FY2015 to FY2025; even stripping out the COVID bump, the underlying compound annual growth rate (CAGR) is around 6.5%, which is solid for a low-growth category. Net profit compounded faster, at approximately 10.1% per year, and the gap between revenue and profit growth is the single most important number on the page. It is a direct readout of management’s “sales-mix optimisation plus house brands plus direct sourcing” thesis: gross margin expanded from 24.7% in FY2015 to 31.3% in FY2025, six full percentage points over a decade. Earnings per share more than doubled from 3.78 cents to 9.94 cents, despite zero share issuance. The share count has been a flat 1,503,537,000 since the IPO. Dividends per share doubled from roughly 3.5 cents to 7.0 cents, and the payout ratio held remarkably steady at around 70% across the cycle.

The balance sheet has fattened in step with profits. Cash has grown from S$87 million at end-FY2018 to S$435 million at end-FY2025, accumulated despite paying out roughly S$96 million per year in dividends. Equity has nearly doubled to S$591 million. The lease liability number on the balance sheet looks worse than it really is. It is almost entirely operating leases on store space that previously did not appear on the balance sheet (Singapore Financial Reporting Standards 16 took effect from 2019), and is offset on the asset side by right-of-use assets of similar magnitude. Net asset value per share has compounded from 19.4 cents at end-FY2018 to 39.1 cents at end-FY2025, doubling in seven years.

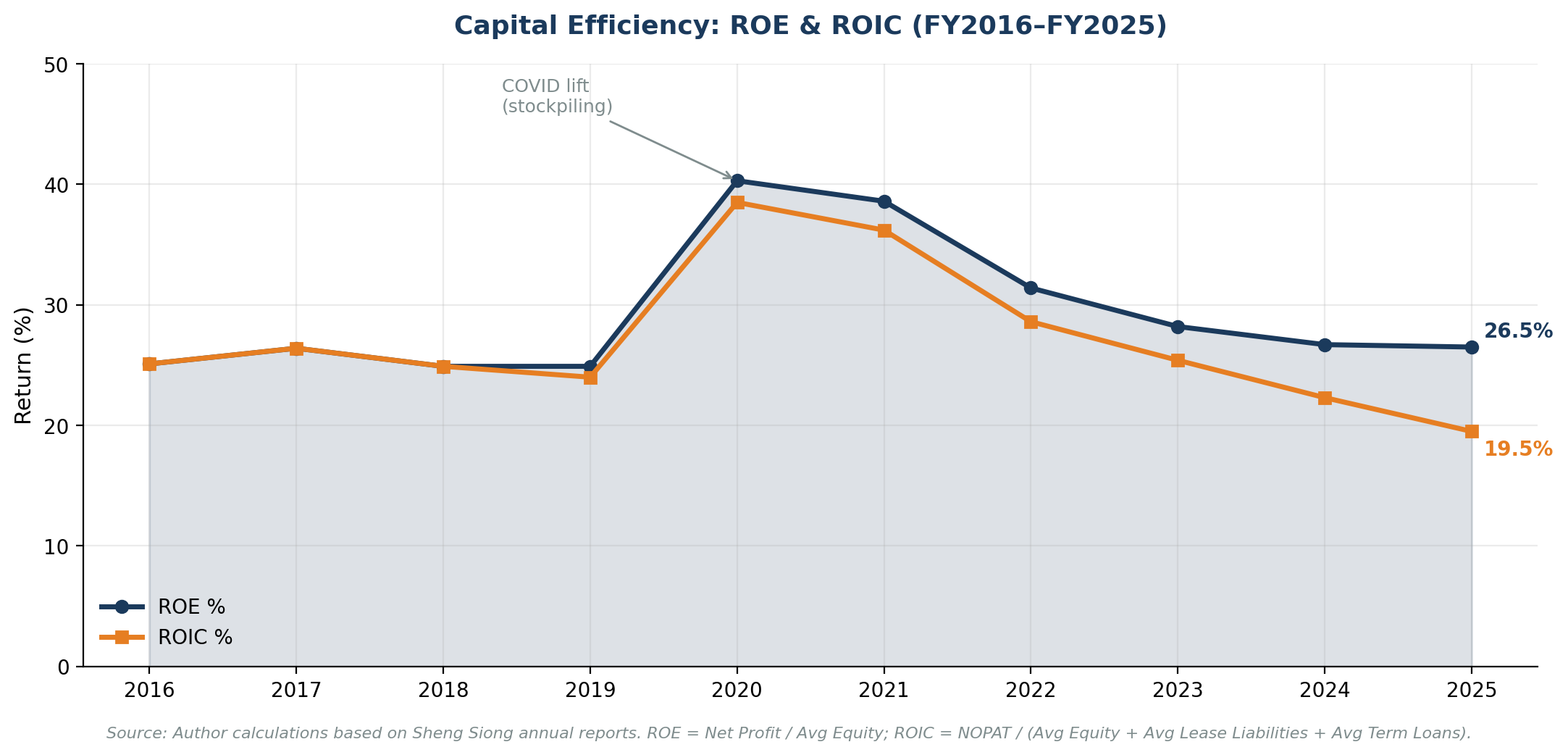

Returns on Capital: Best in Class

Return on Equity (ROE) has been above 25% in eight of the last ten years, peaking near 40% during COVID and settling around 26–27% in FY2024 and FY2025. Return on Invested Capital (ROIC) is structurally a few percentage points lower because of the lease-liability denominator, but still above 19% in FY2025. For context, the Group was awarded “Highest Weighted ROE Over Three Years” in the Consumer Defensive industry by The Edge Billion Dollar Club for the third consecutive year [11].

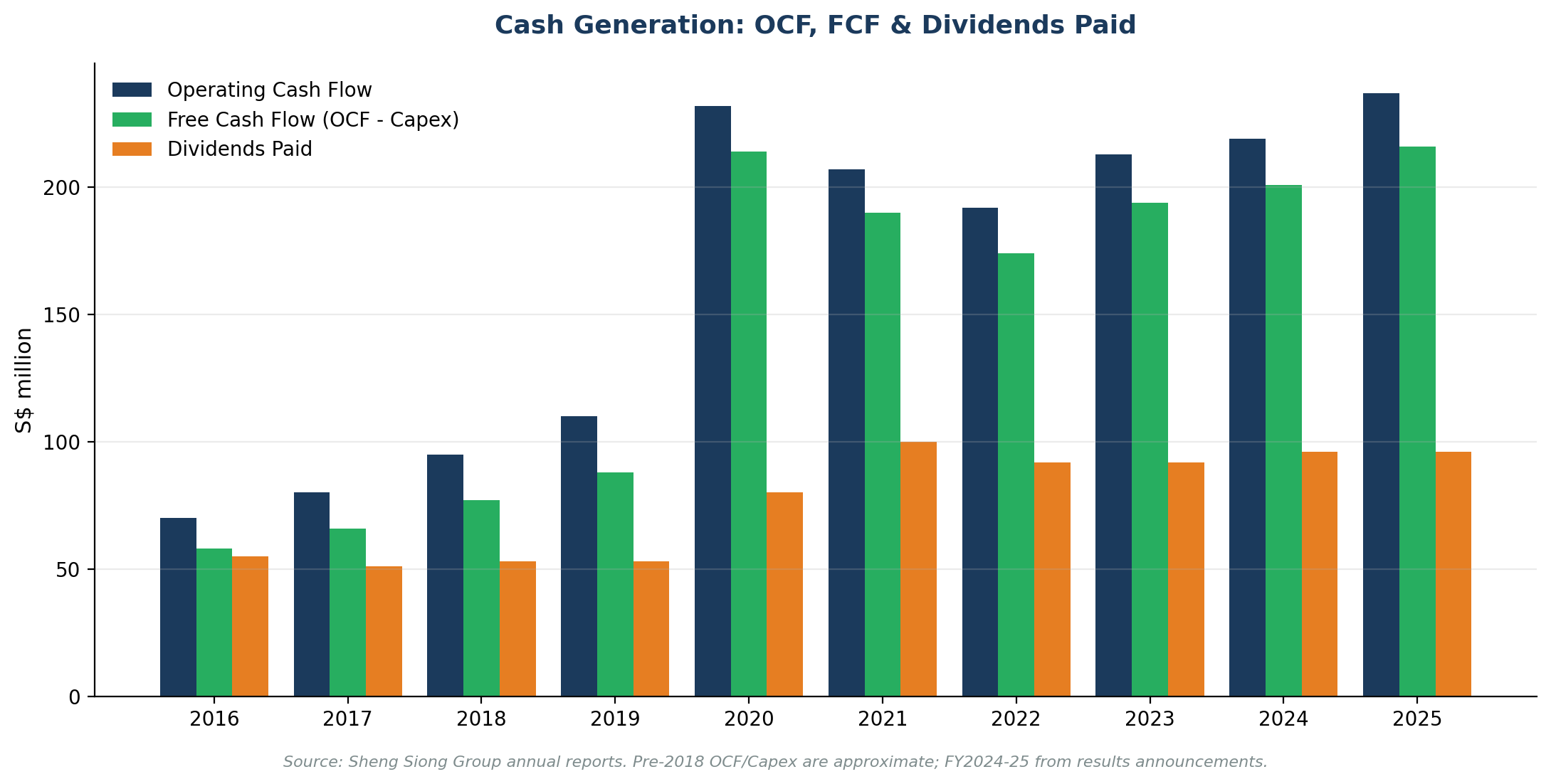

The quality of those returns matters as much as their level. Revenue is paid in cash at the till; working capital is structurally negative, since suppliers fund inventory; capital expenditure requirements are modest in steady state; and incremental gross profit drops nearly intact to operating cash flow. The picture is one of a business that does not need to be re-capitalised to grow, which is why the dividends have been paid every year without strain.

In FY2025 the Group generated S$236.6 million in operating cash flow against capital expenditure of just S$20.9 million. That is a free cash flow conversion ratio above 90%, and a free cash flow figure that comfortably covers the dividend with room to spare. The new Sungei Kadut distribution centre will eventually pull this conversion ratio down for several years, but the trough of free cash flow cover should still leave the dividend intact under management’s communicated plan.

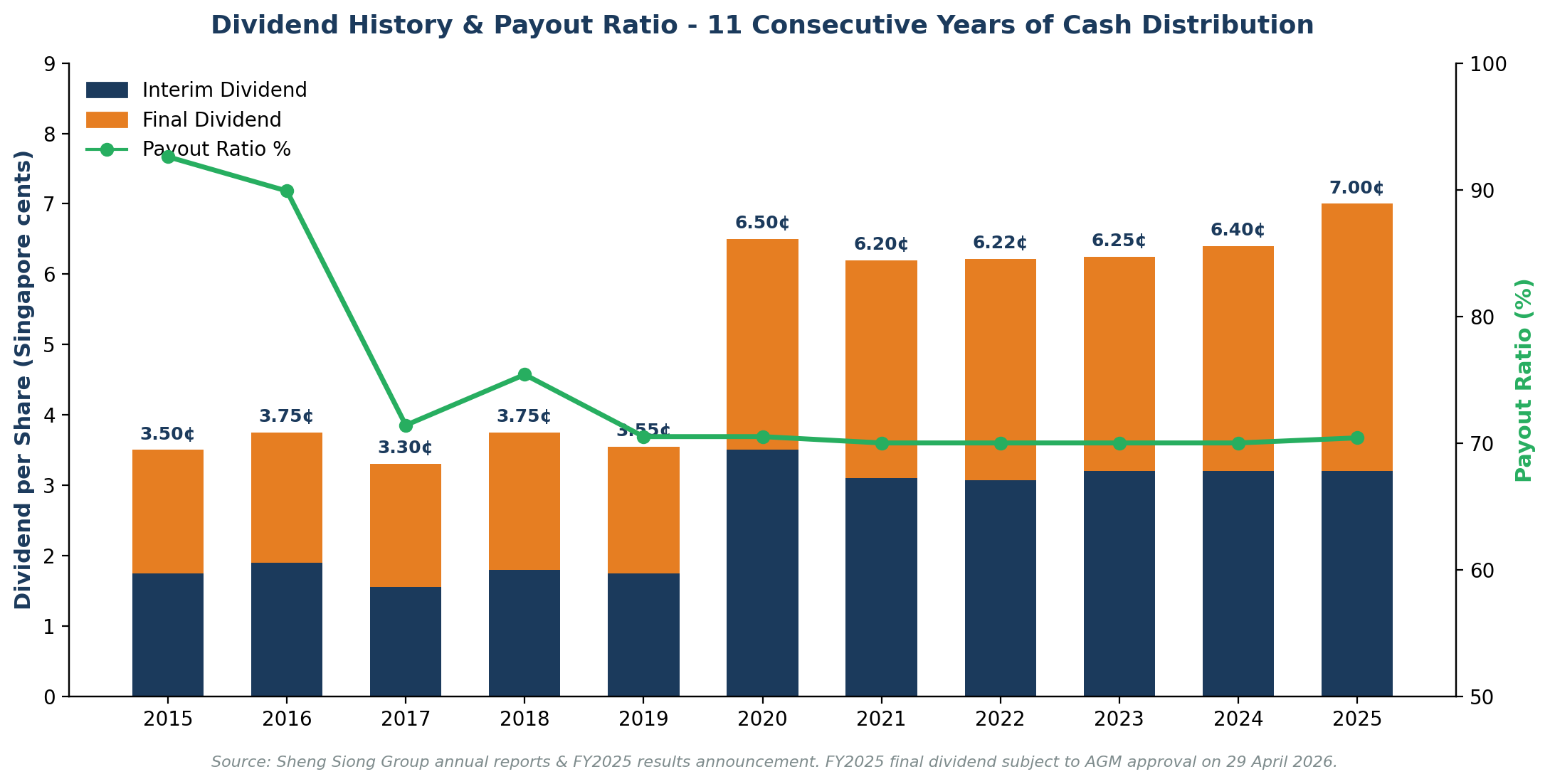

Eleven Years of Dividends: Never Cut, Raised Again

Sheng Siong has paid an interim and a final dividend every year since the IPO, almost always inside a self-imposed 70% payout-ratio policy. The FY2025 final dividend of 3.80 cents per share, up from 3.20 cents the year before, brings total FY2025 dividends to 7.0 cents, a fresh record, payable on 15 May 2026 subject to Annual General Meeting (AGM) approval on 29 April 2026. At the April 2026 share price of S$3.08, the trailing yield is roughly 2.27% [1]. Consensus expectations for FY2026 imply a forward dividend per share around 8.0 cents [2], which would lift the forward yield closer to 2.6%. Modest in absolute terms, but the yield sits on top of organic earnings growth. The total-return profile is closer to a “dividend grower” than a “dividend stalwart”, and the payout has never been funded out of incremental debt.

Growth Drivers Over the Next Three to Five Years

The most visible growth driver is the store rollout. Management opened twelve stores in FY2025 against long-run guidance of three to five per year, and the pipeline includes a secured site at Blk 120 Canberra Crescent, a new store at 11 Rivervale Crescent expected to open in 3Q 2026, and five further tender results pending. The new distribution centre is sized to support at least 120 stores, and the Group’s stated growth aspiration is to add three new stores per year for ten to fifteen years, implying a network of around 117 to 132 stores by the late 2030s. That is roughly 3–5% network growth per year on top of comparable-store growth, which was +1.4% in FY2025.

The second driver is continued sales-mix and house-brand expansion. Gross margin expanded another 80 basis points in FY2025 to 31.3%, and each 100 basis points of additional gross margin is worth roughly S$15.7 million in pre-tax profit at current revenue.

The third is the new Sungei Kadut distribution centre, which is sized to support 120-plus stores and will lift productivity and supply-chain leverage when it comes online around 2029 or 2030. The trade-off is that meaningful capital expenditure must be funded in the late 2020s, and the Mandai Link disposal that anchors the JTC Corporation deal will be timed against this.

A fourth driver, more speculative, is online and quick commerce. Singapore consumers have shifted towards electronic commerce more slowly than peers in larger Asian markets, but the trend is unmistakable. The Deliveroo Singapore partnership launched in early 2025 hit a setback when Deliveroo announced it would cease Singapore operations, but management has stated it will continue to explore alternative quick-commerce partners and to develop the Sheng Siong app organically.

A fifth, almost optional, driver is China, but the right framing is closer to a test lab than to a growth engine. Six Kunming stores generated 2.4% of FY2025 revenue and a small net deficit, and the capital deployed there is small in the context of the Group’s S$1 billion-plus asset base. Management’s tone is unmistakably cautious, framed as “prudent and measured” expansion, and the explicit objective for FY2026 is to improve the performance of existing stores rather than to add new ones. The role of the China subsidiary in the investment thesis is therefore as cheap optionality. If Kunming eventually breaks even and the unit economics travel, that may, in time, support a more confident regional expansion. If it does not, the sums involved are small enough that the downside is contained, and management has shown both the willingness and the discipline to keep it that way.

Major Risks and the Bear Case

Six risks are worth sizing carefully, listed below in rough order of how likely they are to drive the share price over the next three years:

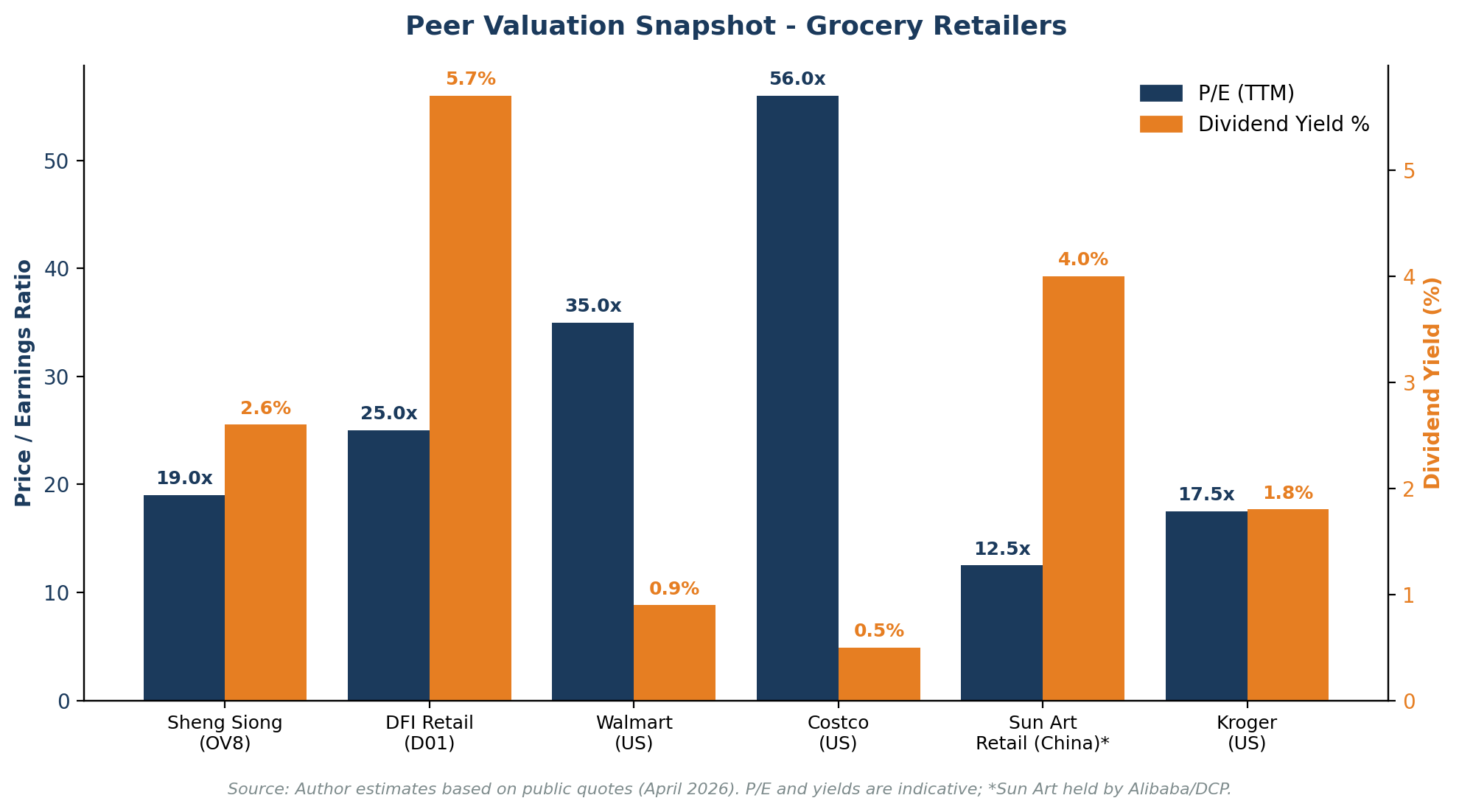

Valuation richness. At S$3.08 the stock trades at roughly 31x trailing earnings and 7.9x book [1]. That is a clear premium to DFI Retail Group at approximately 25x trailing earnings [8], and a wider premium to most US grocery comparables that trade in the 17–20x range. The premium reflects quality, balance sheet, and earnings predictability, but it leaves limited margin for execution slip-ups, and any half-year result that disappoints the consensus could compress the multiple meaningfully.

Margin ceiling. Six points of gross-margin expansion in a decade is rare, and the next 100 basis points will almost certainly be harder to extract than the last. If sales-mix improvement plateaus while wage costs keep ratcheting through Progressive Wage Model and Beverage Container Return Scheme compliance, gross margin could stall or modestly compress. Combined selling, distribution and administrative expenses grew about 12.5% in FY2025, faster than revenue growth of 9.9%. A pattern that, sustained, would erode operating margin even if gross margin holds.

Capex cycle. The Sungei Kadut distribution centre project plus continuing store openings means capital expenditure will step up materially from the recent S$20 million-per-year run-rate. Management has not disclosed a precise total budget, but a multi-year project of this scale and capacity will plausibly run into the hundreds of millions of Singapore dollars. Net cash is likely to fall meaningfully through the build period, although the exact trough depends on the project schedule and on Mandai Link disposal proceeds.

China underperformance. Six stores, eight years after entering Kunming in 2017, with the China subsidiary still loss-making in FY2025. Continued small deficit accumulation is a manageable distraction. An attempt to scale China meaningfully without first proving unit economics in Kunming would be a step-change in capital-allocation discipline that would have to be re-underwritten.

Founder transition. All three founder brothers are now in their late sixties or seventies. Management succession to the second generation is being telegraphed publicly (Lin Ruiwen on the main board, three other family members in operating director roles since 2024), but the handover has not yet been stress-tested.

Free-float and liquidity. The Lim family plus Sheng Siong Holdings own approximately 53% directly, with deemed interests pushing combined family control closer to 62%. Public free float is approximately 46.7%, but daily trading volume is modest by institutional standards, which partly explains why disclosed institutional holdings are unusually thin for a company of this market capitalisation.

A Closer Look at Sungei Kadut: Forced Re-Tooling, Not Free Choice

The most controversial item on the risk list deserves its own treatment, because the natural question for any investor is whether the new Sungei Kadut distribution centre is a sign of management over-confidence or a necessary defence of the cost-leadership moat against a freshly-owned Cold Storage and Giant under Macrovalue. The honest answer is neither, because the binary misses a frame that the FY2025 disclosure makes explicit: this is partly a forced re-tooling.

The over-confidence reading would say that the multi-year capital outlay runs to many multiples of the recent capex run-rate, and that filling distribution capacity sized for 120-plus stores requires a continuation of the very aggressive FY2025 opening pace of twelve stores rather than the long-run guidance of three to five. If store growth normalises, the new distribution centre is structurally over-built for at least a decade.

The moat-defence reading would say that Singapore’s structural labour squeeze (Progressive Wage Model wage increments, an aging working-age population) makes labour-intensive distribution more expensive year by year, and that a more automated centre is partly an insurance policy on wage inflation. Macrovalue is a focused regional operator with a track record of running DFI’s Malaysian food business since 2023, and it would be naive to assume Cold Storage and Giant’s supply chain will be left untouched over 2026 to 2028. Investing in distribution productivity during the window when the rival is still in ownership transition, rather than after it has fully revitalised, is sensible timing even if the absolute number is large.

What the binary misses is that this was not a free strategic choice. JTC Corporation offered the Sungei Kadut parcel conditional on the Group selling or assigning the existing Mandai Link property to a JTC-approved buyer by December 2031. The Group did not initiate the move; JTC did, by tendering a parcel that happens to fit Sheng Siong’s long-run capacity needs. Once that is understood, the question changes from “should the Group spend this much on an upgraded distribution centre?” to “was JTC’s conditional offer good enough to accept, given that staying at Mandai Link past 2031 was not really an option?” The S$2.2 million gain on lease modification booked in FY2025 is the early accounting signal that the swap is at least neutral on book terms.

The honest view, then, is closer to necessary forward-defence than to over-confidence. Strategic direction looks right, the timing relative to Macrovalue is sensible, and the productivity case against wage inflation is real. Execution risk is the hard part. Delivering a project of this scale to budget and on schedule, in Singapore’s tight construction labour market, with a four-to-five-year build window, is where this part of the thesis gets tested. If Sungei Kadut comes in on planned cost and on schedule, the moat-defence reading wins. If it slips materially in cost or to a 2031 delivery, the over-confidence reading wins retrospectively. For the next two to three years, project budget and schedule disclosures matter more than any single quarter’s same-store sales.

Management Quality and Capital Allocation

The promoter family has run this business for over four decades. Executive Chairman Lim Hock Eng was conferred the Pingat Bakti Masyarakat (Public Service Medal) in 2016 and the Bintang Bakti Masyarakat (Public Service Star) in 2022 for community contributions. CEO Lim Hock Chee currently chairs the Marsiling Citizens’ Consultative Committee and was appointed Co-Chairman of the Unit Pricing Industry Workgroup in 2026. The capital-allocation track record has been consistent and conservative across the listed history.

There has been no equity raise since the IPO. The share count has been flat at 1,503,537,000 since 2011, meaning every cent of earnings-per-share growth has come from earnings expansion rather than financial engineering. Mergers and acquisitions activity has been deliberate and infrequent. The Jelita Property acquisition in late 2024 for S$49 million is the only notable corporate deal in years, paid for entirely from operating cash flow, and the deal anchored a flagship store as well as freehold investment property. The dividend policy has been roughly 70% of profits returned every year; the payout ratio has only deviated meaningfully in early IPO years when it ran higher. The China experiment has been disciplined, with six stores in nine years, no hurried roll-out, and no announced intention to accelerate. The board has nine members, five of them independent and three of them female (above the Group’s 30% diversity target). The Audit and Risk Committee is chaired by Tan Huay Lim, a former audit and banking partner of KPMG Singapore with 23 years at the firm.

Related-party transactions, formally known under SGX listing rules as Interested Person Transactions (IPTs), are present but well-disclosed, and small in absolute size relative to the income statement. The largest aggregate IPT in FY2025 was S$3.1 million in rent payable to E Land Properties Pte Ltd (a Lim-family vehicle) for three operating-space leases. Investors should monitor this line item, but it is at a scale that is hard to consider abusive given the visibility of disclosure.

The shareholder register itself tells a clear story. Sheng Siong Holdings Pte Ltd, the family vehicle, holds 29.85%. The three Lim brothers hold a further 22.59% directly in their own names. Citibank Nominees Singapore Pte Ltd, at 8.37%, is the largest custodian-account block, followed by DBS Nominees, DBSN Services, Raffles, HSBC, OCBC and UOB nominees in descending size. Beneath the nominee blocks the register thins out quickly. Position numbers fifteen and sixteen, Lin Yuanfeng and Tan Peck Hiang, hold 0.67% each, with Tan Peck Hiang a spouse of Lim Hock Leng.

Valuation: What the Market Is Paying For

Three framings help decompose the S$3.08 price. The first is the Price-to-Earnings (P/E) multiple. At roughly 31x trailing on FY2025 earnings per share of 9.94 cents [1], the stock is at a clear premium to DFI Retail Group at roughly 25x [8]. DFI is bigger and more geographically diversified, but has structurally lower returns. Globally, Sheng Siong sits between the elevated multiples paid for Costco (above forty times trailing earnings on most data providers in 2025–26) and the more grounded multiples on Walmart and Kroger, which trade in the high-twenties to mid-thirties and the low-to-mid-teens respectively, depending on the data provider and the period [15]. The premium versus the average grocer is real, and reflects the market’s view that Sheng Siong is closer to the Costco end of the spectrum on returns and durability if not on scale.

The second framing is Enterprise Value (EV) divided by Earnings before Interest, Taxes, Depreciation and Amortisation (EBITDA). FY2025 EBITDA, taking operating profit of S$176 million and adding back depreciation of property, plant and equipment plus right-of-use assets, was approximately S$240 million. Net of the S$435 million cash position and ignoring lease liabilities, that produces an EV/EBITDA ratio in the order of 14–15x. Treating capitalised lease liabilities as debt would push the ratio slightly higher. Either way, the cash pile takes some of the sting out of the headline P/E, but Sheng Siong still trades at a premium to most regional grocery peers on this measure.

The third framing is Price-to-Book (P/B). At a market price of S$3.08 and book value of 39.1 cents per share, the stock trades at roughly 7.9x book. That looks demanding in isolation but it is consistent with a 26% return on equity. A return-decomposition lens is in some ways cleaner than a multiples lens. At a 26% ROE and a 70% payout ratio, the implied internal compounding rate of book equity is around 8% per year, and the dividend yield adds another roughly 2.3%. That implies a base-case total-return expectation of around 10–11% per year, before any change in valuation multiple, which value-conscious investors would describe as priced for delivery, not for upside surprise.

A simple discounted-cash-flow framing reaches a similar conclusion. At a 9% cost of equity and a 3.0–3.5% terminal growth rate, the current share price implies roughly 5–6% real revenue growth and stable margins for the next decade. That is plausible. The company’s targeted Singapore store count (eighty-seven to 120 by 2030) alone supports approximately 4% revenue growth, before any margin gain. But it is not heroically conservative either. The valuation is a price for execution. If the execution comes through, the stock pays you in dividends and modest multiple support. If it slips, the de-rating could be sharp.

A Note on the “Parent Company” Question

A few readers will ask how Sheng Siong’s valuation relates to its parent company. The structural answer is that there is no listed parent. The largest shareholder, Sheng Siong Holdings Pte Ltd (often referred to as SS Holdings), is a private investment vehicle owned approximately one-third each by the three Lim brothers. SS Holdings exists primarily to consolidate the family’s stake; its only material asset is shares in the listed company. There is therefore no listed-parent discount to monetise, of the kind that historically existed for, say, Jardine Strategic versus Jardine Matheson. For minority investors, the listed share price is the parent-company price. The controlling family takes its economics primarily through Sheng Siong Group dividends rather than through a separately valued holding company, which is unusually clean by Southeast Asian conglomerate standards.

Recent News and Catalysts

The Group released full-year FY2025 results on 27 February 2026, with revenue of S$1.57 billion (up 9.9%), net profit of S$149.2 million (up 8.5%), and a final dividend lifted from 3.20 cents to 3.80 cents per share. On 23 April 2026, management published responses to questions submitted ahead of the AGM, addressing topics including the Sungei Kadut distribution centre, China losses, the labour-cost outlook and the Group’s quick-commerce strategy. The AGM is scheduled for 29 April 2026, with the re-election of CEO Lim Hock Chee and Independent Director Ko Chuan Aun on the slate.

The most material industry-level catalyst is unfolding outside Sheng Siong’s own operations. DFI Retail Group’s divestment of its Singapore food business (Cold Storage, CS Fresh, Jason’s Deli and Giant) to Macrovalue for S$125 million was announced in March 2025 and was expected to close in the second half of 2025 [12]. The transition will play out through 2026 and 2027, and Sheng Siong is the most natural beneficiary of any short-term operational dislocation at the rebranded competitor stores. Investors should monitor Sheng Siong’s half-year comparable-store sales for any visible step-up in 2026 attributable to this transition.

Looking forward, the major dates and catalysts to watch are:

1 April 2026. Beverage Container Return Scheme implementation begins, adding small operational complexity that supermarkets will absorb across their stores.

29 April 2026. AGM and final dividend approval.

15 May 2026. Final dividend payment date.

3Q 2026. New store at 11 Rivervale Crescent expected to open.

Late 2026 / early 2027. Johor Bahru–Singapore RTS Link scheduled commencement, with potential cross-border shopping diversion that is genuinely difficult to model in advance [10].

2026–2027. DFI / Macrovalue transition plays out at competing Cold Storage and Giant stores.

2029–2030. New Sungei Kadut distribution centre operational. The biggest single multi-year catalyst from within Sheng Siong’s own control, and also the multi-year capital-expenditure peak.

Top Institutional Holders: A Note on the Free Float

A point of distinction worth flagging is that Sheng Siong does not show up as a top holding in the major institutional Form 13F filings disclosed to the US Securities and Exchange Commission (SEC) [9]. The disclosed top holders below the Lim family are mostly Singapore-based nominee accounts: Citibank Nominees (8.37%), DBS Nominees (4.43%), DBSN Services (4.20%), Raffles Nominees (2.55%), HSBC Singapore Nominees (2.29%), OCBC Securities (1.38%) and UOB Nominees (1.34%). These obscure the underlying beneficial owners. Smaller nominee blocks include Moomoo Financial Singapore (0.89%), BNP Paribas (0.68%), iFAST Financial (0.67%) and Phillip Securities (0.66%). The free float, while officially 46.7%, is functionally dominated by Singapore-domiciled retail and high-net-worth investors holding via local custodians rather than by international long-only institutions. This shareholding structure has a real consequence: institutional analyst coverage is thin, and price discovery often runs through retail flows. That is both a liquidity risk and, occasionally, a source of mispricing for patient investors.

Bull vs Bear

The Bull Case

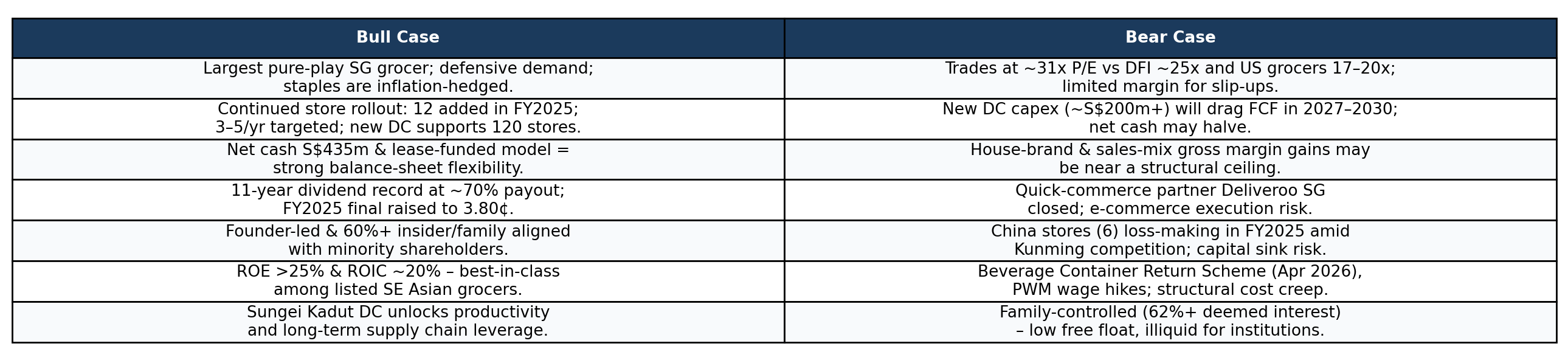

The bull case for Sheng Siong rests on five reinforcing observations:

It is the largest pure-play Singapore-grocery operator on the SGX, in a defensive category, with no listed Singapore competitor of comparable quality.

The store rollout pipeline has accelerated rather than slowed (twelve openings in FY2025 versus the long-run guidance of three to five), with the new distribution centre sized to support a network of at least 120 stores in the medium term.

The S$435 million net cash position, plus a lease-funded operating model, gives the company unusual balance-sheet flexibility to fund the new distribution centre, ride out a recession, and continue raising the dividend.

An interim and final dividend has been paid every year since the IPO, and the FY2025 final has been raised again, providing a yield baseline on top of organic earnings growth.

ROE above 25% and ROIC near 20% are best-in-class among listed Southeast Asian grocers, with founder-led ownership aligning insiders and minority shareholders.

The thread running through these is that the gross-margin expansion engine (sales-mix optimisation plus house brands plus direct sourcing) has been quietly running for more than a decade with no signs of stalling. An illustrative bull scenario, not a price target, is that mid-single-digit revenue growth combined with continued modest margin expansion drives earnings per share to around 12 cents within three years. Sustained at the current ~31x multiple, that scenario implies a stock price meaningfully higher than today.

The Bear Case

The bear case begins with the multiple. At roughly 31x trailing earnings, Sheng Siong trades at a premium to DFI Retail (about 25x) and well above global grocery averages of 17–20x [8]. There is limited margin for error built into the price. The new distribution centre capex cycle (estimated at S$200 million-plus over multiple years) will halve the net cash buffer over 2027–2030 and depress free-cash-flow cover during that period. House-brand and sales-mix gross-margin gains may be approaching a structural ceiling, and any compression here would compound with the wage-cost ratchet from the Progressive Wage Model and Beverage Container Return Scheme. Quick-commerce execution remains an open question after the Deliveroo Singapore exit. China stores are still loss-making and represent an ongoing capital sink unless management demonstrates unit economics work. Founder ownership of 60-plus per cent on a deemed-interest basis is a corporate-governance double-edged sword: alignment, yes, but also a low free float that limits institutional absorption capacity. Finally, the company has never operated through a genuinely deep Singapore consumer recession as a listed entity; COVID was a stockpiling-driven supply-side shock, not a demand-side contraction. An illustrative bear scenario is that a 100–200 basis point gross-margin compression, combined with capital expenditure that runs above expectations, drives earnings per share lower for two consecutive years. Under those conditions a multiple compression to the low-twenties range is plausible, with corresponding share-price downside.

A Variant View: Why Margin Durability Is the Single Question

Strip away the competing scenarios, the macro context, and the management appraisal, and the investment case at S$3.08 ultimately rests on one variable: whether the gross-margin expansion engine that has added more than six percentage points to gross margin over the past decade can continue to grind higher from here. House brands, direct sourcing and sales-mix optimisation have done the heavy lifting for ten years. The market is implicitly underwriting a continuation of that engine, and at roughly 31x trailing earnings, that expectation is not unreasonable. It does, however, leave limited room for deviation.

The variant bullish reading is that the market is underestimating how much margin-expansion runway is still left. House-brand penetration in Sheng Siong’s portfolio, although growing steadily through 2,035 SKUs across twenty-eight brands, is still structurally lower than at the most penetrated global grocers, where private-label products account for a substantially higher share of total sales. Incremental house-brand and sales-mix gains, layered onto a S$1.57 billion revenue base, can still translate into meaningful profit growth. In this framing, Sheng Siong is less a traditional grocer and more a capital-light consumer compounder still early in its margin journey, and the current multiple is, if anything, a reasonable price for an underappreciated runway.

The variant bearish reading is that the easy gains have already been harvested. The next 100 basis points of gross margin will be harder to extract than the last, because the obvious sales-mix shifts and the lowest-hanging house-brand categories have already been worked. At the same time, wage inflation under the Progressive Wage Model, Beverage Container Return Scheme compliance costs, and a competitive landscape under reshuffled DFI ownership may offset further mix improvements, placing a soft ceiling on operating margin precisely as the Group enters a heavier capital-expenditure cycle for Sungei Kadut. In that scenario, earnings growth slows while the valuation multiple stays elevated, a combination that rarely sustains for long.

Positioning: When Does This Setup Work?

At current levels, the investment case is less about multiple expansion and more about execution. If the Group delivers continued store rollouts at 4–5% per year, stable or slightly expanding gross margins, and disciplined capital deployment through the Sungei Kadut cycle, then mid-single-digit earnings growth combined with a 2–3% dividend yield can support a low double-digit total return profile, with little contribution from any change in valuation multiple. The margin for error, however, is narrow. Any evidence of gross-margin compression, negative comparable-store sales, or capital-expenditure overruns would likely re-rate the stock to a lower multiple.

In practical terms, this is the kind of stock that tends to become more attractive during periods of operational noise, when short-term pressures temporarily obscure what is otherwise a stable long-term profile. Buying high-quality compounders during their less interesting quarters has historically been a more reliable path than buying them after a string of clean results.

A Single-Variable Decision Framework

If the investment thesis can be reduced to a single question, that question is margin durability. If you believe Sheng Siong can continue to extract incremental gross margin through sales mix, scale and sourcing advantages over the next five to ten years, then the current valuation is defensible as a fair price for a high-quality consumer compounder. If you believe gross margin is near a structural ceiling, then the stock is pricing in a level of future profitability that will be difficult to exceed and easy to disappoint. At S$3.08, the market is not obviously wrong, but it is also not leaving much room for it to be.

What Would Break the Thesis

If you own Sheng Siong, or are thinking about it, the leading indicators to watch are concrete and few. Five matter most:

Half-year gross-profit margin. A drop below 30% in any half-year would suggest either a competitive pricing reset, a US-dollar-driven raw-material shock, or a labour-cost step that cannot be passed on.

Comparable-store sales growth. Comparable stores grew 1.4% in FY2025. A persistent negative number in subsequent half-years would indicate either heightened competition (most plausibly NTUC FairPrice undercutting) or genuine consumer-demand erosion.

Sungei Kadut distribution centre capex schedule. If the budget materially exceeds expectations or delivery slips beyond 2030, free-cash-flow cover and dividend cover thin out.

China profit and loss trajectory. A larger China net deficit, or any decision to expand China meaningfully, would mark a step-change in capital-allocation discipline that would have to be re-priced.

Ownership transition. A material change in the Lim family’s deemed interest, or the resignation of any of the three brothers without a clear handover, would force a re-pricing of the management premium currently embedded in the stock.

The Bottom Line

Sheng Siong remains one of the cleanest consumer-staples businesses on the SGX. High returns on capital, strong free-cash-flow generation, eleven straight years of dividends, and a balance sheet that provides both resilience and optionality. None of that has changed in the last three years, the last five years, or the last decade. What has changed is not the business, but the price.

From here, returns are less likely to be driven by multiple re-rating and more by the company’s ability to keep executing the same model that has delivered for four decades. The bull case is execution-led: keep doing what the family has been doing for forty years, just with more stores, a bigger distribution centre, and a slowly-modernising omnichannel. The bear case is ceiling-led: the company is great, but is now perhaps priced as if it were even greater, and the deliberate decision to cap regional ambition means the upside on revenue growth is anchored to Singapore’s HDB pipeline rather than to a multi-country roll-out story.

For investors, the question therefore shifts from “Is this a good business?”, which it clearly is, to “How much of that goodness is already reflected in the price?” Watching the half-year gross-profit margin, comparable-store growth and the Sungei Kadut capex schedule will tell you which scenario is unfolding well before the multiple does.

References

Market Data Sources

Yahoo Finance, Growbeansprout, TradingView (sg.finance.yahoo.com/quote/OV8.SI; growbeansprout.com/quote/OV8.SI; tradingview.com/symbols/SGX-OV8). Share price (S$3.08 as at 20 April 2026), 52-week high (S$3.25 on 9 April 2026), market capitalisation (approximately S$3.97–4.01 billion), trailing P/E and dividend yield references. Accessed April 2026.

Stock Analysis (stockanalysis.com/quote/sgx/OV8) and consensus dividend forecast data. FY2025 yield of approximately 2.27% on a 7.0¢ dividend; FY2026 consensus dividend per share of approximately 8.0 cents; consensus target price of approximately S$3.04. Accessed April 2026.

Mordor Intelligence. Singapore retail/supermarket industry market size of approximately US$36.25 billion in 2024. (mordorintelligence.com/industry-reports/retail-industry-in-singapore)

Singapore Ministry of Trade and Industry (MTI). 2026 GDP growth forecast range of 2.0–4.0%. Referenced via the Group’s FY2025 results announcement and supporting MTI press releases.

Gourmet Pro. Singapore supermarket landscape and the FairPrice / DFI / Sheng Siong triopoly composition. (gourmetpro.co/blog/biggest-supermarkets-singapore)

Monetary Authority of Singapore (MAS). Singapore Core Inflation: 2.8% in 2024, 0.7% average in 2025, projected 1–2% in 2026. Referenced via the Group’s Chairman’s Statement (FY2025 Annual Report) and supporting MAS publications.

Singapore Department of Statistics / National Population and Talent Division. Population and HDB housing background context referenced for the heartland-store-rollout thesis.

Industry and Peer Comparison Sources

Stock Analysis, Stockopedia, Simply Wall St. DFI Retail Group (SGX: D01) peer multiples; DFI trailing P/E of approximately 20–25x as referenced in published valuation pages, and analyst consensus target ranges. Accessed April 2026. (stockopedia.com/share-prices/dfi-retail-group-SGX:D01; simplywall.st/stock/sgx/d01)

Fintel.io and Yahoo Finance. Third-party institutional ownership analysis for Sheng Siong, indicating no disclosed Form 13F-filing institutional holders above the substantial-shareholder threshold; ownership functionally dominated by retail and Singapore-domiciled custodial accounts. Accessed April 2026. (fintel.io/so/sg/ov8)

Johor-Singapore Special Economic Zone (JS-SEZ) and Land Transport Authority Singapore. Johor Bahru–Singapore RTS Link scheduled commencement late 2026 / early 2027; cross-border consumer flow context cited in the Group’s FY2025 commentary as well as supporting public infrastructure briefings.

Other Public References

The Edge Billion Dollar Club. “Highest Weighted ROE Over Three Years (Consumer Defensive Industry)” awarded to Sheng Siong for the third consecutive year, as cited in the FY2025 Chairman’s Statement.

DFI Retail Group / Macrovalue transaction announcements (March 2025). DFI Retail Group’s divestment of its Singapore food business (Cold Storage, CS Fresh, Jason’s Deli and Giant; 89 stores plus two distribution centres) to Macrovalue for S$125 million, expected to close in the second half of 2025. Source of: deal price, store count, segment operating margin context (food 1.8% versus Health & Beauty 8.6% and Convenience 4.3% in FY2024), and the prior 2023 Macrovalue acquisition of DFI’s Malaysian food business. (Coverage referenced via DBS Insights, The Smart Investor, Dr Wealth, theedgemalaysia.com, theonlinecitizen.com.) Accessed April 2026.

Sheng Siong Group Ltd FY2025 Annual Report, Board of Directors profiles. Source of: founders’ employment in their family’s hog-rearing business prior to founding the Group; the Group’s establishment in 1985; Lim brothers’ service as directors of Sheng Siong Supermarket Pte Ltd since 1983 (Lim Hock Eng and Lim Hock Chee) and 1994 (Lim Hock Leng).

Singapore Department of Statistics, Population in Brief 2024 / National Population and Talent Division. Projection that residents aged 65 and over will reach approximately 24% of total resident population by 2030, up from 18.4% in 2023.

Yahoo Finance, stockanalysis.com, Bloomberg consensus pages for COST, WMT and KR. Indicative Price-to-Earnings reference points for Costco Wholesale Corp., Walmart Inc. and Kroger Co. as at April 2026. Multiples vary across data providers and reporting periods; the article uses approximate ranges only as cross-references.

Notes on Data Integrity

Historical financial figures from FY2015 through FY2024 are sourced from Sheng Siong Group’s published Annual Reports for those years. FY2025 figures are sourced from the SGX Results Announcement dated 27 February 2026 (”SSG-Results-Announcement-2HFY2025”). Where the FY2024 comparative differs slightly between the FY2024 and FY2025 filings, this article uses the figures as restated in the most recent FY2025 announcement.

Estimates of free cash flow, ROIC, and EBITDA are author-derived from disclosed P&L, balance-sheet and cash-flow line items. Pre-2018 operating cash flow and capex figures used in the cash-flow chart are approximations based on the closest disclosed proxies in earlier annual reports.

The Sungei Kadut distribution centre capital-expenditure figure has not been disclosed in primary filings as a single committed budget. References to “hundreds of millions of Singapore dollars” or to a “multi-year project” reflect indicative project-scale estimates only. Investors should rely on the Group’s own subsequent disclosures for the actual budget and schedule.

Peer P/E multiples for global grocers (Costco, Walmart, Kroger) are indicative reference points sourced from third-party data providers (see reference 15) and vary by source and reporting period. They are intended only as illustrative cross-checks against Sheng Siong’s multiple, not as authoritative comparables.

The illustrative bull and bear scenarios are editorial in nature and are not derived from a formal discounted-cash-flow or earnings model.

All financial data drawn from Sheng Siong Group SGX filings (FY2014–FY2025) and Annual Reports unless otherwise indicated. Market data references are as at April 2026.

IMPORTANT DISCLAIMERS

General Disclaimer: This article is published for informational and educational purposes only. It does not constitute financial advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The views expressed are based on publicly available data from Sheng Siong Group Ltd’ SGX filings and publicly accessible market data, and may not reflect the most current developments.

Not Licensed Financial Advice: The author is not a licensed financial adviser, and this publication is not issued by a holder of a Capital Markets Services Licence under the Securities and Futures Act 2001 of Singapore. This content does not fall within the definition of “financial advisory service” under the Financial Advisers Act 2001 of Singapore. Readers in Singapore should note that this content is exempt from the requirements of the Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication.

MAS Compliance Notice: In accordance with the Monetary Authority of Singapore’s guidelines, this publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, you should consult a licensed financial adviser who can provide advice tailored to your personal circumstances. Past performance of any security discussed herein is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author may or may not hold positions in the securities discussed. No compensation has been received from any company mentioned in this article.

Thanks for laying out the history and the variables to determine the investment case. Wanted to share an anecdote from 2014 when I first met the founders. When I expressed concern about FairPrice’s scale and potential lack of profit motive (government influencing them to drive down pricing) which might affect margins, was taken aback by management’s response. The CEO narrated an incident where Sheng Siong were running an aggressive price campaign on a product in 2012. The supplier of the product requested a meeting and told management to moderate or even stop the promotion. Intrigued the CEO asked the supplier ‘aren’t you happy that your volumes are rising?’ The supplier said if SS kept at it, his product might be taken off the shelves of FairPrice! I understood that to be a subtle message from FairPrice to SS via the supplier that price competition is mutually destructive and better to appear competitive rather than destroy value for both. This benign competitive landscape, DFI’s mismanagement along with the benefits of the central warehouse drove gross margins to the levels they are today!

The SEA Analyst, thanks for sharing your analysis of Sheng Siong Group Ltd (OV8; SSG SP).

(1) How do you assess the threat from new entrants like Scarlett?

Scarlett started in 2020 with just 1 store. Now, they have over 40 stores.

Mainland Chinese businesses carry a reputation of being aggressive competitors.

(2) It will be interesting to see how the RTS will impact same-store-sales and margins.

Like you said, it's very difficult to predict the impact.

The best precedent we have is in Hong Kong. The Shenzhen-HK high-speed rail (HSR) opened in 2018.

Since then, the businesses in HK were badly hurt. Café de Coral, one of HK's most popular eateries, experienced > -50% decline in operating margins.

That said, it is easier to travel and dine. Groceries are a hassle to carry.

I suspect Sheng Shiong will probably feel some negative impact, but not as much as F&B businesses.

Let's see how it plays out.