S$41 Million in Profit. S$14 Million for Shareholders. Foundation Healthcare's IPO Maths

Foundation Healthcare lists 8 July at S$0.76 to S$0.92. A pre-IPO share swap explains the gap, and is struck cheaper than the listing.

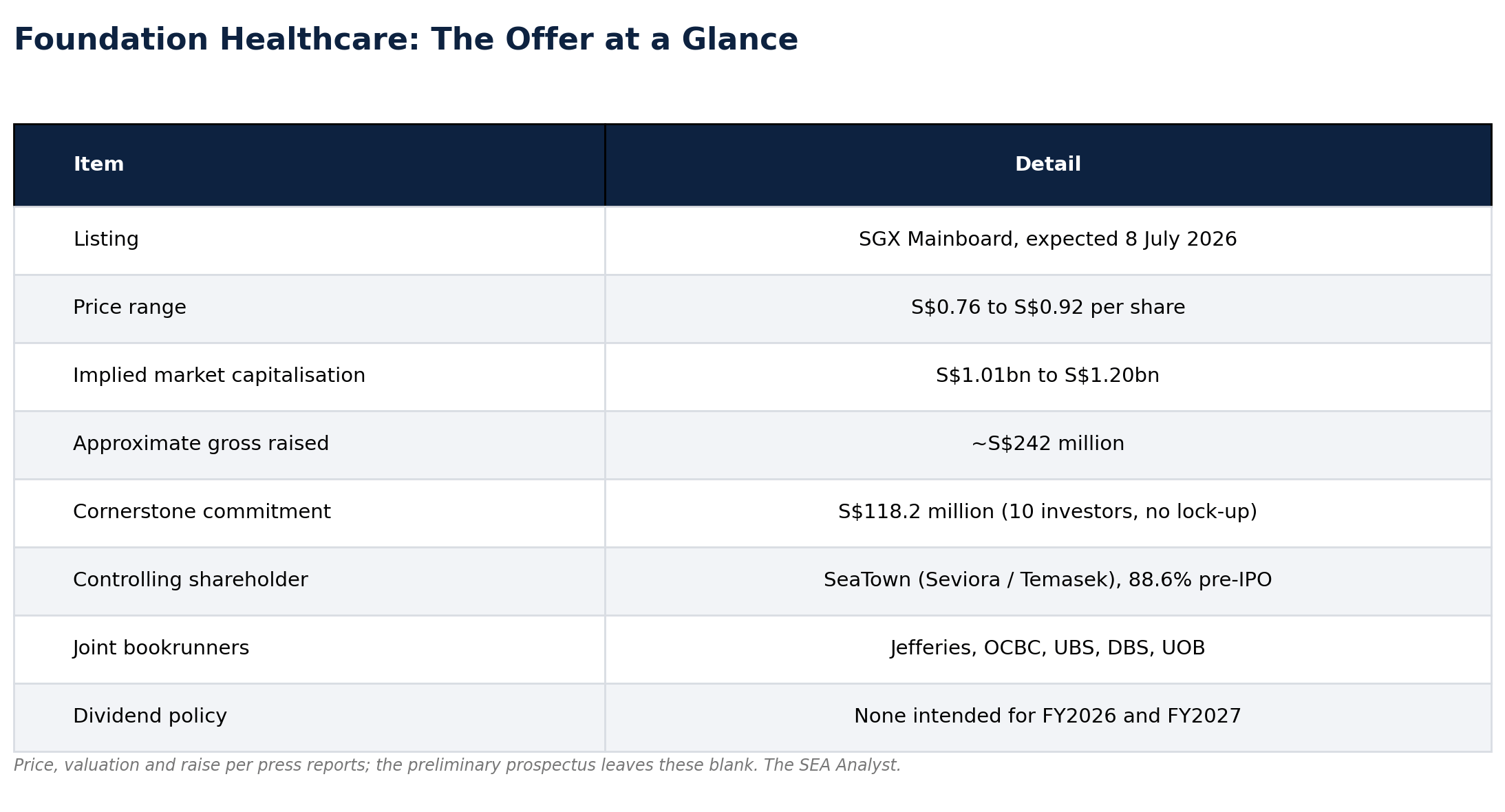

If you have seen a specialist at Mount Elizabeth Novena, Gleneagles, Farrer Park or Mount Alvernia in the past two years, there is a fair chance that doctor now works, indirectly, for a company Temasek helped seed in 2022. In under four years Foundation Healthcare Holdings has bought control of established specialist practices across Singapore, and it is now asking the market to value the result at S$1.01 billion to S$1.20 billion: a price range of S$0.76 to S$0.92 a share, raising around S$242 million, with SGX Mainboard trading expected from 8 July 2026 [3].

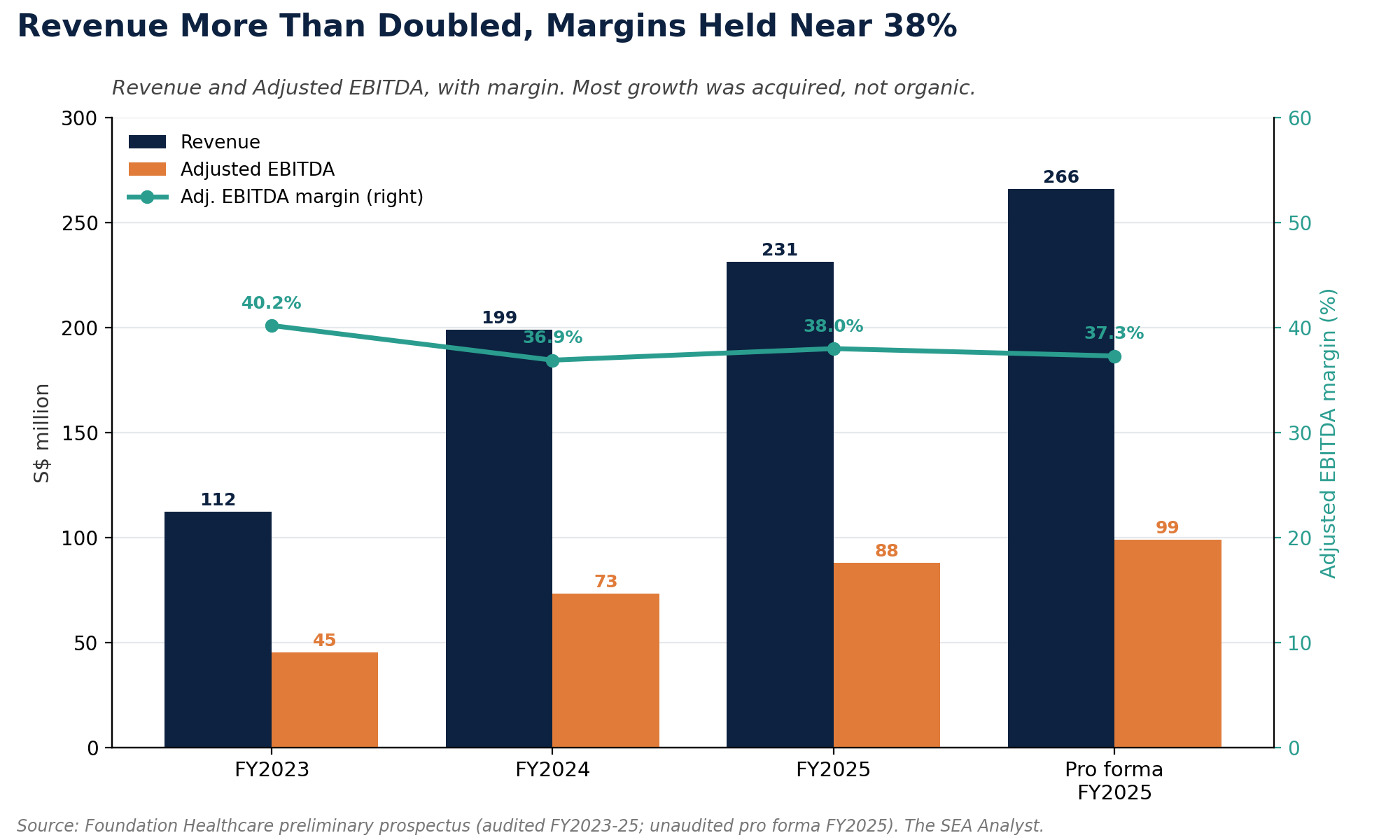

The headline numbers are genuinely impressive. Revenue grew from S$112.4 million in FY2023 to S$231.2 million in FY2025. Group profit rose from S$7.3 million to S$41.2 million over the same two years. Among the key private specialist groups in Frost & Sullivan’s comparison, it is the largest by number of doctors and clinics, and the fastest growing by revenue from FY2024 to FY2025 [2]. Ten cornerstone investors, including the International Finance Corporation, Manulife, RBC, UBS and Lion Global, have committed S$118.2 million between them.

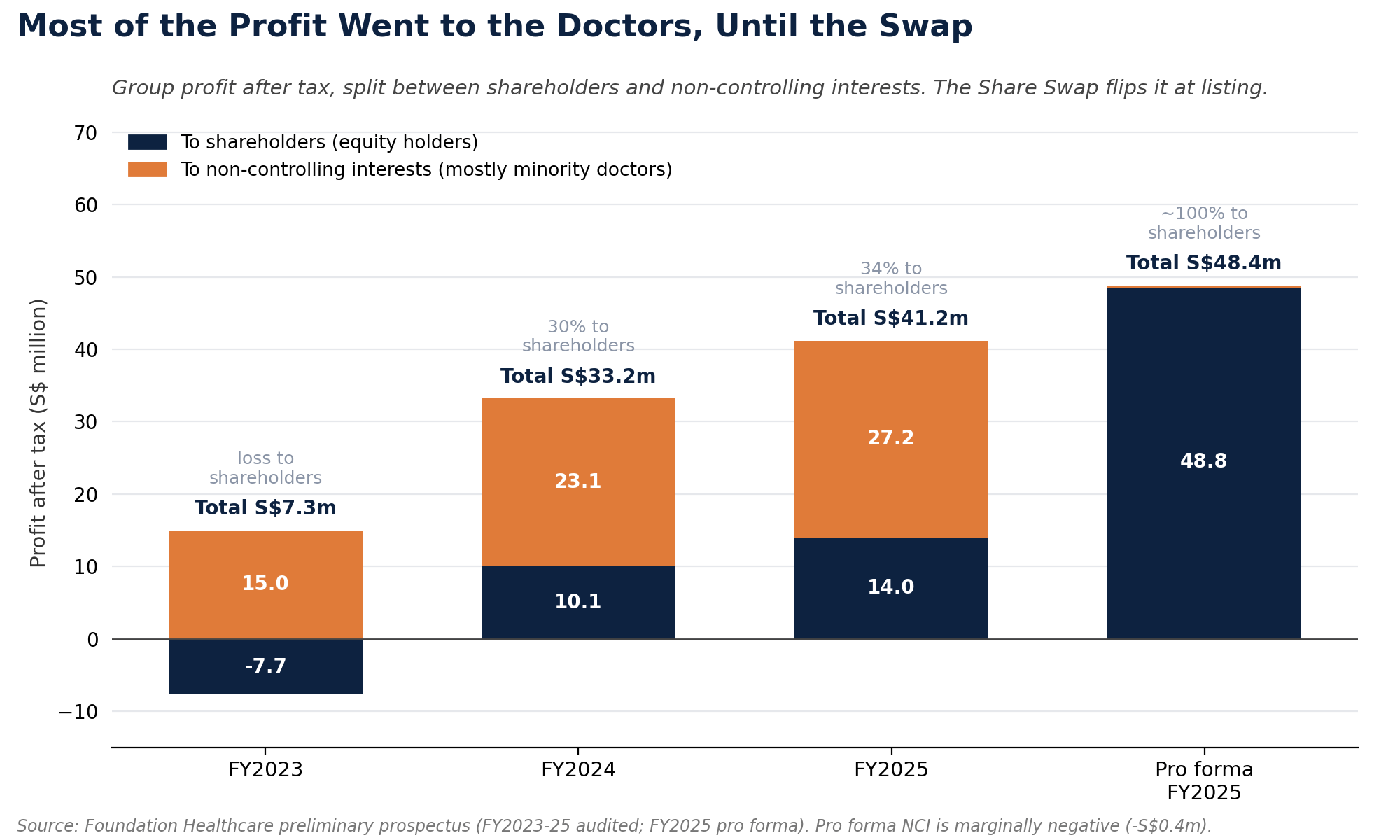

The number that matters most, though, is none of those. Of the S$41.2 million the group earned in FY2025, only S$14.0 million was attributable to shareholders of the parent company. The other S$27.2 million, two thirds of the total, was attributable to non-controlling shareholders, principally the minority owners of its part-owned specialist practices. How the company closes that gap, and what closing it costs, is the question the rest of this piece is about.

From a Temasek bet to Singapore’s largest specialist platform

Foundation Healthcare was incorporated in August 2022, but its founders had worked together far longer. CEO Liaw Yit Ming was a vice president at Khazanah Nasional, then ran strategy and M&A at IHH Healthcare, owner of the Parkway and Gleneagles hospitals. COO Dr Lee Hong Huei spent almost two decades in senior roles at Parkway Pantai. CCO Choy Shook Yee came through IHH and AIA. Liaw had co-founded Smarter Health, an insurtech in which Lee and Choy were also shareholders and which is now a wholly owned subsidiary. They know the Singapore private-hospital world from the inside.

The capital came from SeaTown Private Capital Master Fund, part of Seviora Holdings and ultimately Temasek-owned, which committed S$150 million of preference funding in 2022, completed in 2023. With that and a S$192.5 million debt facility from March 2023, the company moved fast: in FY2023 alone it bought effective 60% stakes in 23 specialist practices plus a medical centre for S$337.2 million cash, adding the Care IVF fertility clinic and the Orchard day-surgery centre. By 31 March 2026 it ran 108 specialists across 16 specialties, 74 clinics and four medical centres, including a new Novena day-surgery centre that management, citing Frost & Sullivan, calls the largest standalone facility of its kind in Singapore [2].

The structure across almost every acquisition was the same: buy 60%, leave 40% with the selling doctor. That single design choice is the key to reading the financials.

What the offer actually contains

The offer mixes new shares from the company with vendor shares sold by SeaTown and the founders, plus an over-allotment option (UBS is stabilising manager). The company’s net proceeds are earmarked, in order, for more clinic and medical-centre acquisitions in Singapore, for expansion into Malaysia and Hong Kong (the IFC’s cornerstone money is tagged to Malaysia), and for working capital. None goes to repaying debt.

The cornerstone tranche is worth pausing on. S$118.2 million across ten credible institutions is genuine institutional validation of the offer. One structural detail the marketing will not emphasise, though, is that the cornerstones carry no lock-up: the six-month lock-up binds the company, and longer moratoria bind SeaTown and the two founder-directors, but the institutions that anchored the book are free to sell from day one. That is not a prediction about the aftermarket, only a reminder that a cornerstone book signals confidence at the offer price, not a floor under it once trading begins.

The S$27 million that did not reach shareholders

Notice what is missing from the group’s reported profit. In FY2025, Foundation earned S$41.2 million after tax, but S$27.2 million of that, fully 66%, was attributable to non-controlling interests, principally the minority owners of the group’s part-owned operating companies, above all the 60%-owned specialist practices. Only S$14.0 million flowed to equity holders of the parent. Basic earnings were 2.13 cents per share. This is the honest starting point, and it is far less flattering than the group revenue line.

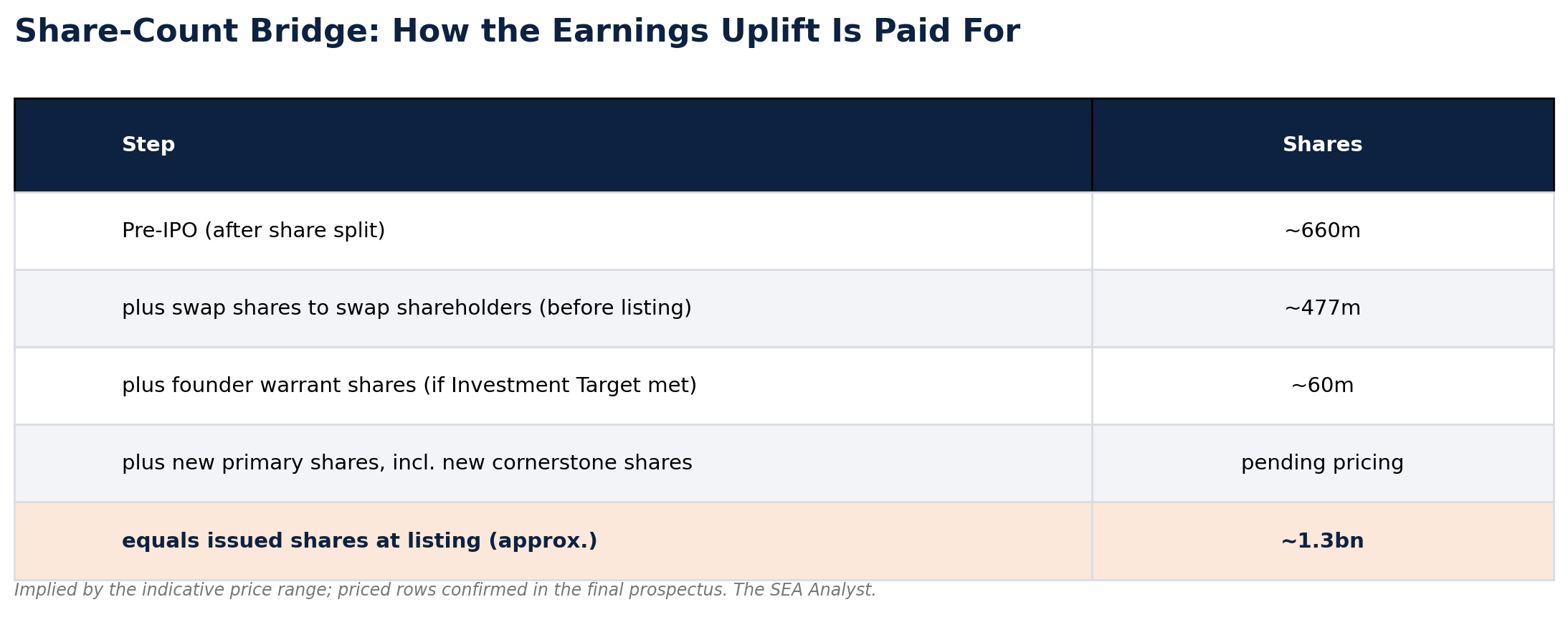

The prospectus addresses this with a step taken just before listing, the Share Swap: the company issues 477,101,524 new shares to 82 Swap Shareholders and 10 Employee Specialists to acquire the remaining interests in 35 specialist-practice companies and the Orchard medical-centre company, lifting its effective ownership to 100%. The stake bought in is generally 40%, except for the Orchard centre at 39.5%. After that, all of each practice's profit belongs to the listed group rather than leaking to non-controlling interests, and on a pro forma basis attributable profit jumps to S$48.8 million, or 4.08 cents per share. Pro forma simply means "as if": it restates the year as though the swap and all the year's acquisitions had been in place on 1 January 2025, rather than counting each clinic only from the date its deal closed. Think of totting up a full year's pay on a salary you only started in September. The prospectus calls this information illustrative and not necessarily indicative of future results, which is the right way to read it. Adjusted profit after tax, the company's preferred measure, which strips out acquisition and capital-raising costs, the FY2023 warrant charge, derivative fair-value movements, impairments and other company-defined one-offs, is S$51.4 million pro forma.

Both numbers are real. The swap genuinely completes before the shares trade. But the swap is not free, and the price is not paid in cash. It is paid in alignment, and in dilution.

The dilution is worth seeing as a bridge, because for this IPO the share count is almost as important as the income statement.

The arithmetic is striking. The swap shares alone, about 477 million, are roughly 37% of the post-listing company, issued to the selling Swap Shareholders and Employee Specialists. Assuming the Founder Warrant Shares are issued under the reported offer terms, SeaTown, on 88.6% before the offer, is diluted below half even before selling a single vendor share. The swap reduces the pre-swap shareholders' collective ownership to a little over half, before the primary IPO issuance dilutes it further. For new investors, that dilution is the price of turning the leaky 60/40 structure into one where every dollar of profit counts: the same trade-off as before, seen from the share count rather than the income statement. The exact primary, vendor and over-allotment splits, and SeaTown's final stake, stay blank until the final prospectus sets the price; the bridge also leaves out small pre-IPO award-share tranches [1].

There is a flip side to that dilution, and it cuts against the idea that the doctors are getting a rich deal. Those 477 million shares are worth S$363 million to S$439 million across the offer range, struck against the S$27.2 million the bought-in 40% earned in FY2025: an acquisition multiple of roughly 13 to 16 times. That is well below the 21 to 25 times the IPO asks new investors to pay for the company as a whole, so the swap is accretive. Absorbing the 40% lifts earnings per share from about 2.1 cents to about 3.6 cents before any new money is raised. The doctors are, in effect, bought in below the listing multiple, trading a higher private valuation for liquidity, a listed currency and continued pay, with the lock-ups and clawbacks attached. A like-for-like read has limits, since an acquired, locked-up minority would normally fetch less than a freely traded share, but the direction is clear: on these terms the swap favours the incoming shareholder more than the selling doctor.

The trade-off is also about incentives, though it is less binary than it first looks. Under the 60/40 model a surgeon retained a 40% equity interest in the clinic they ran. After the swap they hold shares in a roughly 1.3 billion-share group, with most of the Swap Shares (472 of the 477 million; the Orchard-centre shares are excluded) under moratoria and performance-linked release of varying lengths, backed by a clawback through the escrow agent (UOB Kay Hian) if targets are missed. Crucially, the doctors also keep being paid: the prospectus says specialists receive a base salary and/or a variable component tied to the financial performance of the specialist clinic group in which they practise, with the restricted shares layered on top. So the real question is narrower than "ownership versus shares": does base-plus-clinic-performance pay, together with locked equity in the wider group, preserve the same owner-operator intensity as a direct 40% stake in one's own practice? It is the valuation case, not the pro forma accounting, that assumes it does, through the lock-up years.

The financial scoreboard

Set the ownership question aside for a moment, because the underlying business is clearly growing and clearly profitable at the operating level.

Revenue compounded at roughly 43% a year over two years, mostly from acquisitions rather than organic growth, and the pace is slowing (up 77.0% in FY2024, 16.2% in FY2025). Adjusted EBITDA margins held in a tight 37% to 40% band, high for healthcare services and a function of a surgical, procedure-heavy mix. Company-defined adjusted return on equity (Adjusted PAT over total equity) was 18.9%, or 22.0% pro forma, and free cash flow conversion ran at 76.5% of adjusted EBITDA. The business throws off cash.

The caution sits one layer down. For the three months to 31 March 2026 the company said preliminary trends pointed to higher revenue and slightly higher Adjusted EBITDA, but lower profit and Adjusted PAT than a year earlier. The disclosed drivers: a third of its 108 specialists (34) are now “Emerging Specialists” still building their books; headquarters headcount rose from 43 to 71 for listed life; the new Novena centre is ramping; and Orchard closed in March for refurbishment. Management attributes much of the pressure to investment and ramp-up costs, though the preliminary data is not enough to rule out other operating effects. The ramp does have a rough timeline. The prospectus classifies a doctor as “Established” only after five years in private practice, and a defined cohort of Emerging Specialists employed at least twelve months generated about S$1.3 million each, against the S$2.7 million a comparable Established Specialist averaged. That points to a multi-year development period, though it does not prove revenue rises evenly or takes the full five years; either way the recovery runs over years, not a couple of quarters, which is why a doctor-heavy year depresses margins before lifting them. It also means the pro forma S$51.4 million is an everything-acquired, full-year snapshot, not a run rate proven quarter after quarter.

The cash flow and the debt

This is where the model asks for vigilance. The growth was bought, and it was bought substantially with borrowed money. At the end of FY2025, borrowings excluding lease liabilities were S$302.0 million, against S$85.3 million of cash and equivalents plus S$11.1 million of restricted cash. On the pro forma balance sheet, total borrowings including leases were S$348.0 million and cash and bank balances were S$71.6 million, implying simple net debt of about S$276.4 million, or 2.8 times pro forma Adjusted EBITDA (S$99.1 million); this is our own calculation, not the banking covenant measure. Finance expense alone was S$17.8 million in FY2025, a meaningful claim on operating cash flow. The senior facility carries interest at SORA (Singapore’s benchmark interest rate) plus a margin of 2.25% to 3.00%, with covenants that include a maximum total leverage ratio of 4.0 times and an interest-cover floor of 1.75 to 2.0 times.

Two features deserve attention. First, the facility blocks the subsidiaries from paying dividends up to the parent if that would breach the covenants, which is why the prospectus warns the company “may be constrained from paying dividends”: the cash is earned in the subsidiaries, but the listed shell sits above the covenant gate. Second, the interest-rate swaps hedging S$247 million at about 5.5% are not designated as hedges, so their mark-to-market swings run through the income statement as the “fair value loss on derivatives”, the source of those line items, not any option owed to the doctors.

The balance sheet is also unusually intangible. Goodwill represented 70.6% of total assets at the end of FY2025. That is the natural arithmetic of a roll-up that pays for established practices, and it leaves tangible asset backing thin. The pre-offering pro forma net asset value (the accounting book value per share, before the primary cash from the offer comes in) was just S$0.18; the post-offering figure will be disclosed in the final prospectus once pricing and the number of new shares are fixed. Either way, the value here is the earnings stream and the network, not the assets on the page.

The controller, the board, and negative tangible net worth

Governance is better than the typical new Singapore listing in some respects, and worth watching in others. The board is genuinely independent in form: an independent non-executive chairman (Stephen Lim), four of six directors independent, and an Audit and Risk Committee chaired by Max Loh, a former Ernst & Young Singapore managing partner. Despite owning 88.6% before the offer, SeaTown places no nominee director on the board, and Temasek’s stated policy is not to direct its portfolio companies’ operations. Executive cash pay is modest (the chief executive in the S$500,000 to S$750,000 band), and the disclosed related-party dealings are small and on ordinary commercial terms (Singtel telecoms, a SeaTown-linked medical-supplies distributor, each under S$200,000 a year). No clinics are leased from insiders.

Two things deserve a second look. The first is that the technology effort behind the platform story was bought in from related parties. Smarter Health, the insurtech Liaw co-founded, was acquired into the group in exchange for shares; the prospectus lists 27 sellers, among them Liaw, Lee and entities associated with them. It says the deal was struck on the same terms as with an unrelated party, but the founders and their associates sat on both sides of it.

The second is the balance sheet, and it is worth slowing down for. Most of what Foundation “owns” is goodwill: the premium it paid to buy profitable clinics over and above the value of their physical assets like equipment and cash. Strip that goodwill out and the company’s tangible net worth is negative, roughly S$206 million in the red at the end of FY2025. That has an unusual side-effect for small shareholders. Normally, when a listed company wants to do a sizeable deal with one of its own insiders (its controlling owner, a director, or a related party), that deal must be put to a vote of the other shareholders once it crosses 5% of the company’s tangible net worth, a built-in check against insiders extracting value. With that net worth below zero, the percentage cannot be calculated, so the SGX has let Foundation measure the limit against its market value (around S$1.1 billion) instead, until it reports its FY2026 results. That keeps the rule working, but it raises the dollar value of the 5% shareholder-approval threshold, so larger insider deals can clear on audit-committee review alone; transactions at or above that threshold still go to a shareholder vote [1].

A moat that depends on the people it just bought out

Foundation’s competitive case is real. Scale gives it buying power on drugs, supplies and payment processing, and a centralised patient funnel through its Health Connective Programme and the AVA technology platform that smaller visiting-specialist groups cannot match. Employing its doctors full-time, rather than the visiting or sessional model used by certain peer platforms, allows tighter coordination and lets it capture facility and diagnostic fees at its own medical centres. Its pro forma 18.2% net margin comfortably beats Frost & Sullivan’s anonymised peers, whose margins ran from 9.3% down to 5.2% [2].

The payor relationships are the most defensible layer. The April 2025 Great Eastern partnership and the empanelment of more than 97% of its specialists (excluding anaesthesiologists and radiologists) with two or more insurers and third-party administrators make Foundation a preferred network just as medical costs climb. The widely cited 16.9% inflation figure for 2026 (15.5% for 2025) [2][4] needs care: it traces to WTW’s Global Medical Trends survey, the most aggressive of the consultancy forecasts (Aon put 2026 at 13%, Mercer Marsh at 14%), and measures an insurer “medical trend” of utilisation and case-mix shifts, not pure prices; the Ministry of Health puts the actual Healthcare Consumer Price Index nearer 3% in 2025 [5]. Either way, insurers are squeezed and pushing toward cost containment and day-surgery settings, so a platform offering predictable pricing and cheaper outpatient procedures has a structural reason to exist.

That same pressure cuts the other way, though, and this is where the payor layer is less of a moat than it looks. To contain costs, insurers are narrowing their networks: Prudential and Great Eastern now name partner-hospital panels, and in 2025 Great Eastern briefly suspended pre-authorisation at the two Mount Elizabeth hospitals after finding bills there ran 20% to 30% above comparable facilities [5]. Foundation’s clinic footprint is heavily concentrated in exactly those higher-cost hospitals: 22 clinics at Mount Elizabeth Novena and 16 at Mount Elizabeth Orchard. The relationship that the prospectus frames as a moat is the same lever insurers are using to steer patients toward cheaper venues. It can be an advantage and an exposure at once.

One feature of the revenue base is worth being careful about. The prospectus emphasises Singapore-based channels, a funnel of local residents, insurer and third-party-administrator empanelment and GP referrals, and it contemplates patients paying providers directly and then seeking reimbursement [1]. What it does not disclose is the split of revenue by patient nationality, by insurer versus self-pay, or any foreign-patient share. So the business is clearly Singapore-centric, but the absence of any medical-tourism discussion is not evidence that there are no foreign or cash-paying patients. Unlike the hospital majors, Foundation does not market itself on foreign-patient inflows; how much that insulates it, or limits it, when insurers tighten panels is not something the filing lets us quantify.

Where the moat is weaker is the same place the earnings come from. A specialist group is, ultimately, its specialists, and the average doctor here is around 52 years old with 25 years of experience. The relationships, the referrals and the reputations belong to individuals. The Share Swap and its moratoria are explicitly designed to bind those individuals to the platform, which is an admission that, without contractual lock-ins, they could walk. A moat that has to be written into an escrow agreement is a moat under construction, not one that has weathered a cycle.

The roll-up question the prospectus does not ask

There is a precedent for buying up doctors’ practices at scale on debt and listing the result on a growth multiple. In the United States in the 1990s, physician practice management companies such as MedPartners, PhyCor and PhyMatrix did exactly that, were valued as compounders, then collapsed when acquired-practice productivity faded and the bought-in doctors’ incentives drifted from shareholders’. The lesson was not that the model cannot work, since IHH and others built durable specialist businesses, but that the moment of maximum optimism is usually the listing, while the acquisition machine is still running and the incentives are fresh. Foundation is genuinely different in important ways: a single, highly regulated, high-margin market, Temasek governance, covenant discipline, real margins and cash today, and a moratorium-with-clawback more thoughtful than a simple earnout.

The closer-to-home precedent is more pointed. The previous generation of SGX-listed medical-group roll-ups has almost all left the exchange, usually cheaply: Singapore Medical Group taken private in 2022 [8], Healthway Medical delisted in 2023 [9], TalkMed privatised at S$0.456 (about S$606 million) in 2025 [10], and Singapore Paincare’s buyout collapsing at the end of 2025, leaving a loss-making shell [11]. Singapore’s public market has not historically held a premium multiple on a listed specialist roll-up; the usual end-state has been a take-private at a modest price. Neither the 584-page prospectus nor its Frost & Sullivan market-research appendix mentions any of this. Investors should supply the history themselves.

What the market is asking you to pay

Here is the valuation stated plainly, and it depends entirely on which earnings number you accept. Across the S$0.76 to S$0.92 offer range, the company is valued at