Q&M Dental Group: From One Clinic to Asia's Dental Empire. Is the Ambition Priced In?

Singapore's largest dental chain is betting S$130 million on becoming Asia's dental empire. The data says it's a coin flip.

Most Singaporeans have walked past a Q&M clinic. There are 110 of them on the island, roughly one for every 54,000 residents. What most people don’t know is that behind those neighbourhood dental chairs sits a publicly listed company with a S$568 million market cap [1], a freshly raised S$130 million war chest, and simultaneous acquisition targets in Australia, Thailand, and China.

Q&M Dental Group has been listed on the SGX Mainboard since 2009. In that time, it has grown from a small chain into the largest private dental operator in Singapore, survived a pandemic that nearly doubled its PATMI from FY2019 to FY2021, and is now attempting to become a regional dental platform across Asia-Pacific. The question for investors is whether the stock at S$0.60 (up 114% from its 52-week low [1]) reflects the company as it is today, or the company it’s trying to become.

The Company: What Q&M Actually Does

Q&M Dental Group (全民牙科集团) was established around 1996 by Dr Ng Chin Siau — the company describes 2026 as its “30th year.” The name tells the story: “全民” (Quan Min) means “for all the people,” and from day one, Q&M was positioned as mass-market dental care, not premium boutique dentistry. Dr Ng started with a single clinic and built it into Singapore’s dominant private dental chain through relentless acquisition of small practices and organic clinic openings. The corporate entity was incorporated in 2008 and listed on the SGX Mainboard in November 2009.

As at 31 December 2025, the Group operates 110 dental outlets and 5 medical clinics in Singapore, 37 dental clinics in Malaysia, and, through its newly consolidated subsidiary Aoxin Q&M, 7 dental polyclinics and 7 dental hospitals in China, supported by 4 dental laboratories and 2 dental equipment and supplies distribution companies. That’s approximately 161 dental clinic-equivalent outlets across three countries, plus ancillary facilities, served by about 270 dentists seeing roughly 42,000 patient visits per month in Singapore alone.

Beyond clinics, Q&M runs a dental college (the first private postgraduate dental diploma programme in Singapore), a dental AI technology subsidiary (EM2AI), and dental equipment distribution businesses in Singapore and Malaysia.

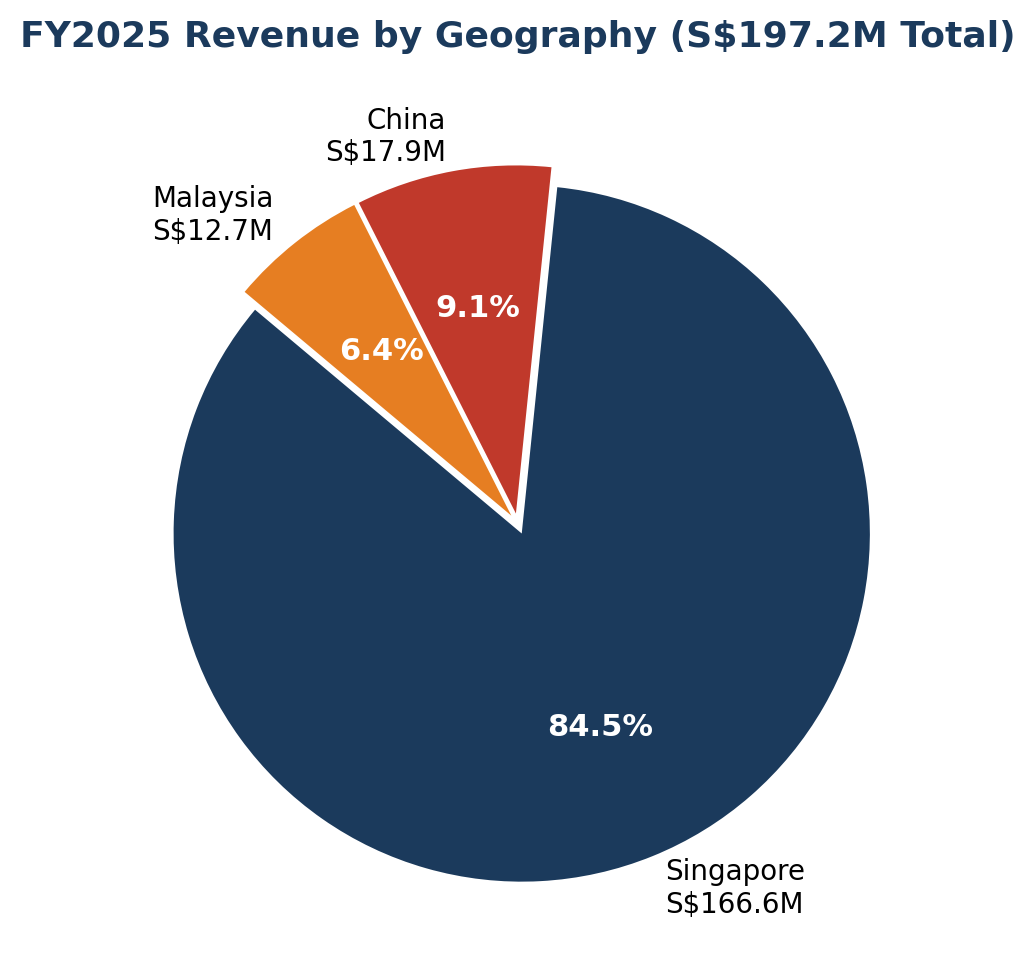

Revenue is heavily concentrated in Singapore (84% of FY2025 revenue), with Malaysia contributing 6% and China (now consolidated for the first time) adding 9%. This geographic split is about to change dramatically if the company’s acquisition plans materialise.

A Brief History: The Ups and Downs

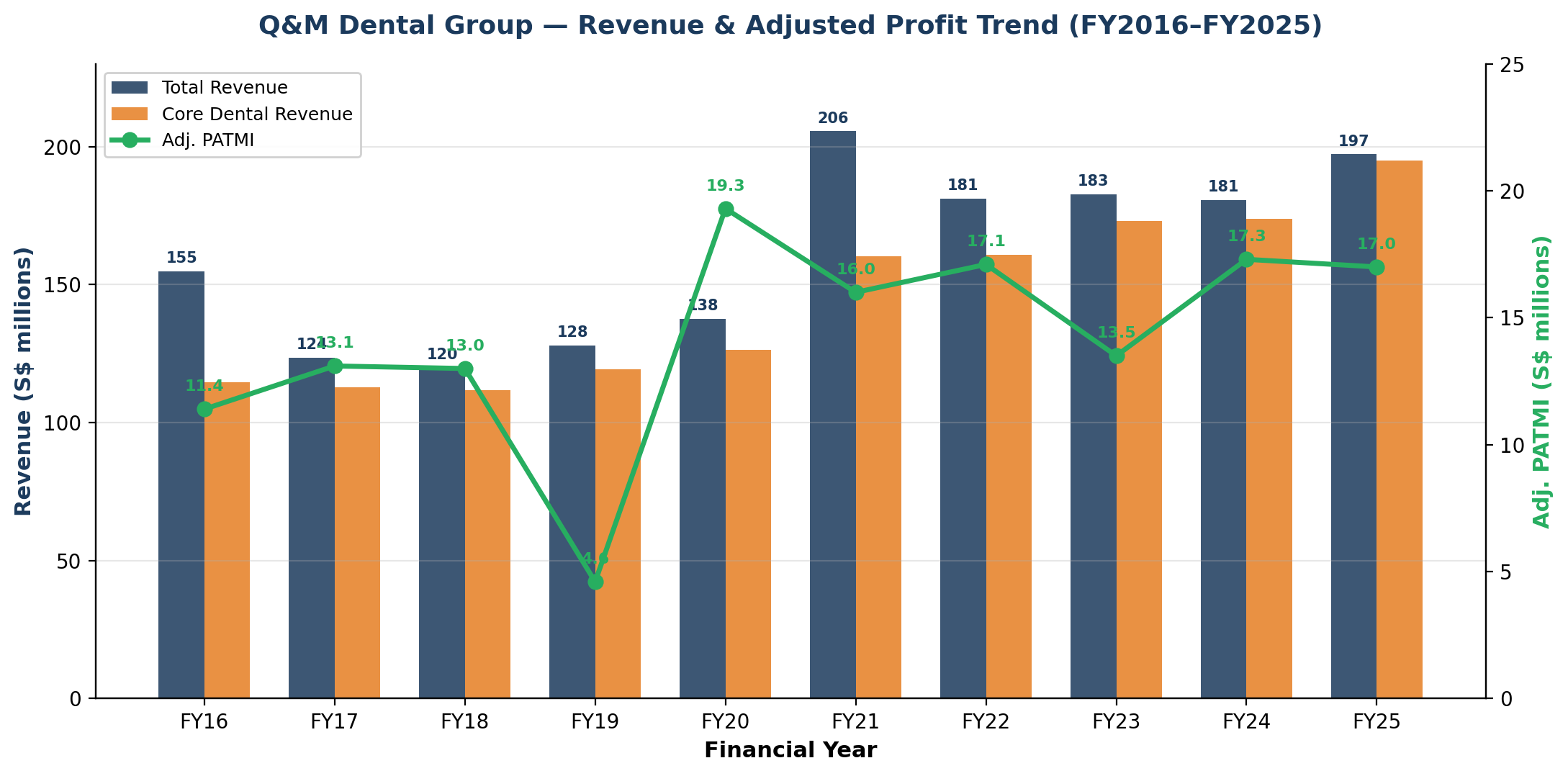

2009–2016: The Growth Machine. Listed on the SGX in November 2009, Q&M expanded aggressively through clinic acquisitions. Revenue grew from roughly S$60 million to S$155 million. A valuable stake in Aidite Technology (a Chinese dental supplies manufacturer) generated significant associate income, and FY2016 PATMI hit S$28.3 million, though much of it came from one-off disposal gains.

2017–2019: Restructuring. Q&M spun off its China operations as Aoxin Q&M, disposed of its Aidite stake, and repaid its first S$60 million Medium Term Note. Stripping out one-offs, core dental profit was roughly S$13 million per year. Revenue grew modestly to S$128 million by FY2019.

2020–2021: The COVID Windfall. Q&M pivoted into COVID-19 PCR testing, boosting medical lab segment revenue from near-zero to S$45.4 million. Total revenue hit S$205.6 million, PATMI reached S$30.5 million, and the company paid S$0.04/share in dividends. This was the peak. The testing revenue was ephemeral.

2022–2023: The Hangover. Testing revenue evaporated, PATMI fell to S$11.3–11.5 million as lab impairments and Aoxin losses dragged on results. But the core dental business proved its resilience: core healthcare EBITDA was stable at S$37–40 million throughout.

2024–2025: The M&A Pivot. Core dental profit recovered to S$26.1 million (FY2024, restated) and then S$30.4 million (FY2025) — a 16% year-on-year jump. Meanwhile, Q&M consolidated Aoxin Q&M as a subsidiary, raised S$130 million through Medium Term Notes at 3.95%, and signed non-binding MOUs to acquire dental groups in Australia (AUD 144.5M), Thailand (30+ clinics), and China. Reported PATMI fell to S$9.3 million due to one-off consolidation losses and MTN interest costs — but the core business has never been stronger.

Financial Performance: What the Numbers Tell Us

The most important insight from the financials is that Q&M’s core dental business has been remarkably stable and quietly growing, even as the headline numbers have been volatile.

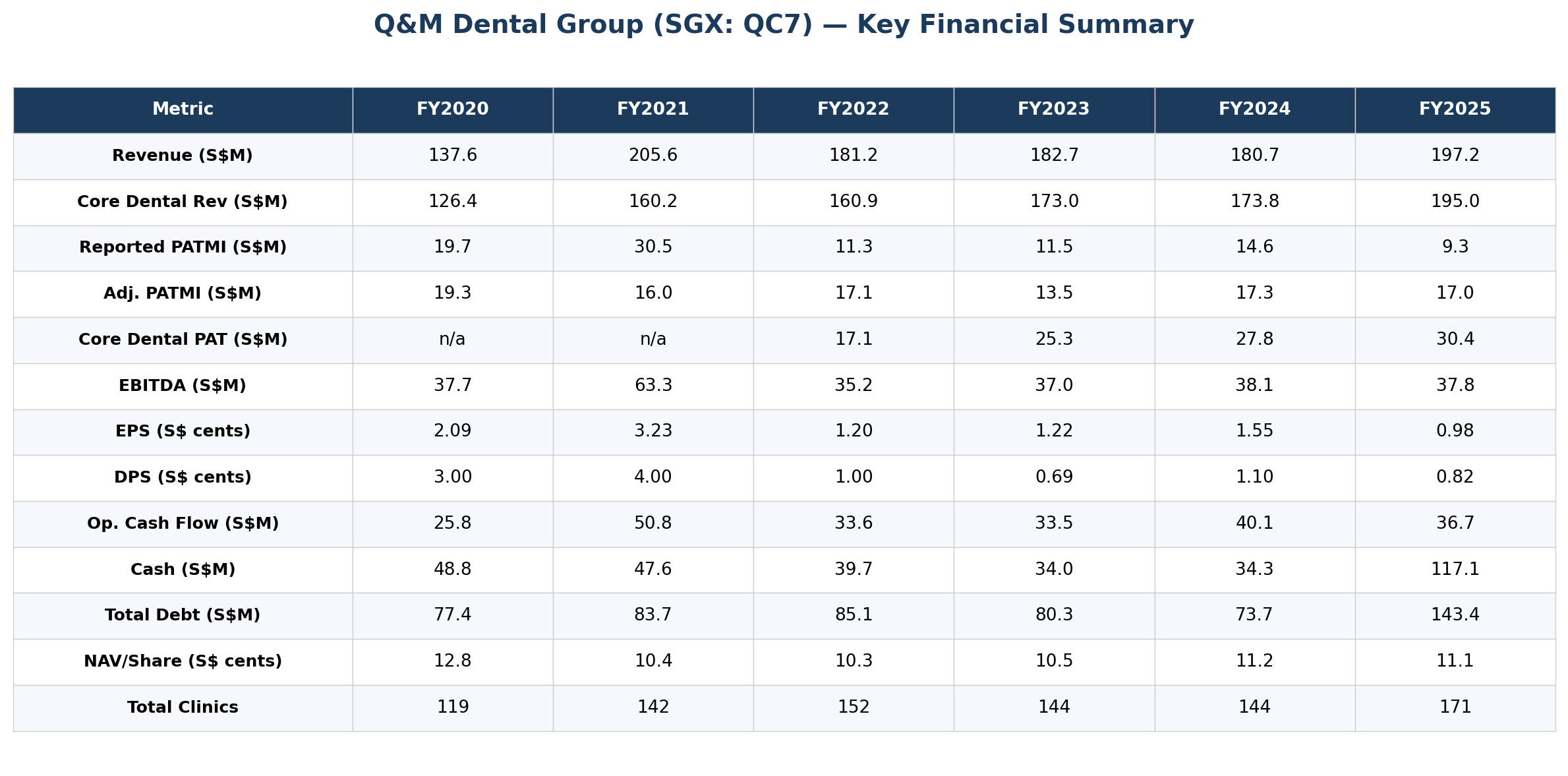

Revenue. Core dental revenue has grown at a roughly 5% CAGR over the past five years, from S$126 million in FY2020 to S$195 million in FY2025. The jump in FY2025 includes approximately S$18 million from the Aoxin consolidation. Stripping that out, organic core dental revenue growth was still solid at approximately 3–4%.

Profitability. The reported PATMI line is noisy, distorted by COVID testing profits in FY2020–21, lab impairments in FY2022–23, and consolidation losses in FY2025. The cleaner metric is core dental profit after tax, which has grown from S$17.1 million in FY2022 to S$30.4 million in FY2025, a 78% increase over three years. This is the trend that matters.

Margins. Core dental segment results (before corporate costs and finance charges) were S$55.4 million on S$195 million revenue in FY2025, implying a segment margin of roughly 28%. Employee costs are the largest expense at S$115 million (58% of revenue), followed by lease-related depreciation at S$13.8 million (7%).

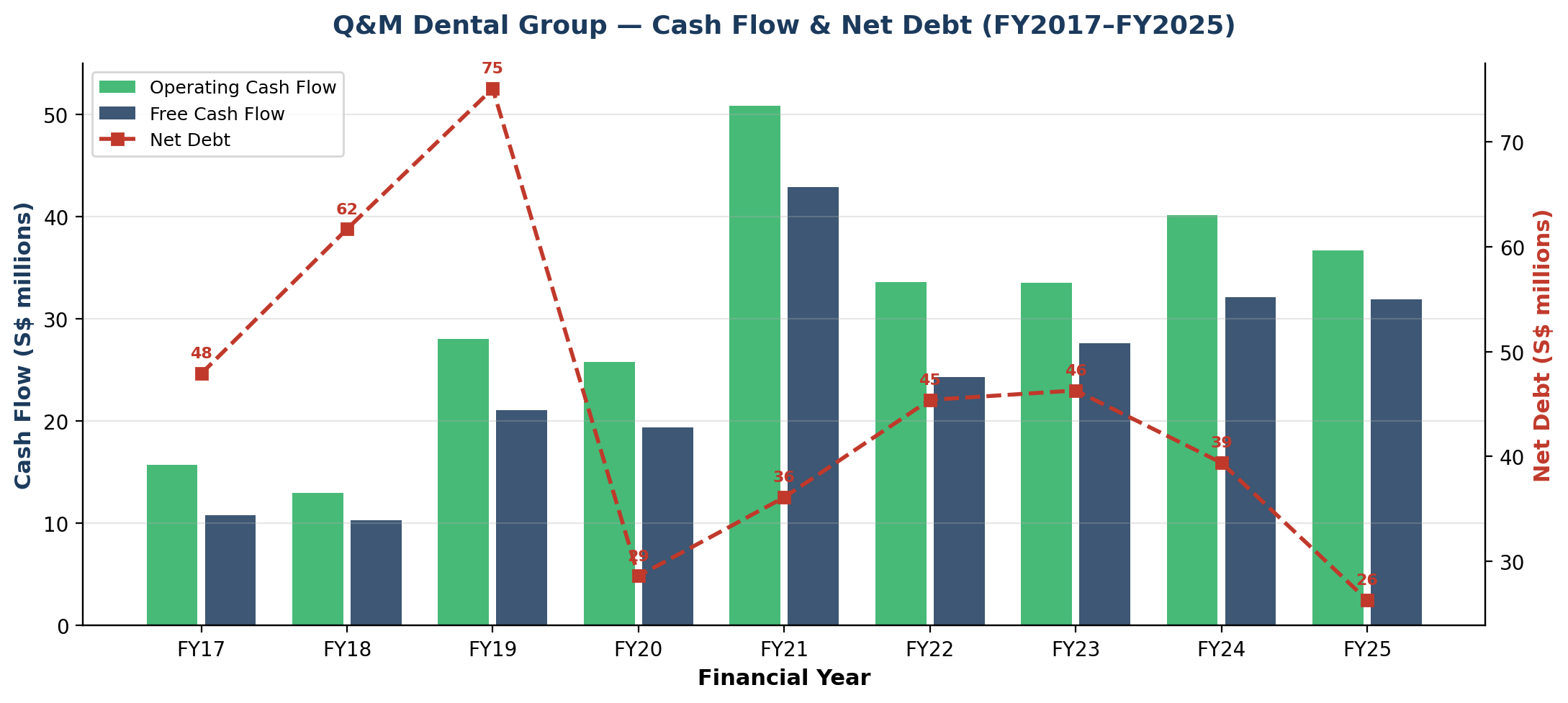

Cash Flow. Operating cash flow has been consistently strong: S$33–50 million annually. FY2025 saw S$36.7 million, sufficient to cover capex of S$4.8 million and dividend payments. The S$130 million MTN issuance in July 2025 transformed the cash position from S$34 million to S$117 million.

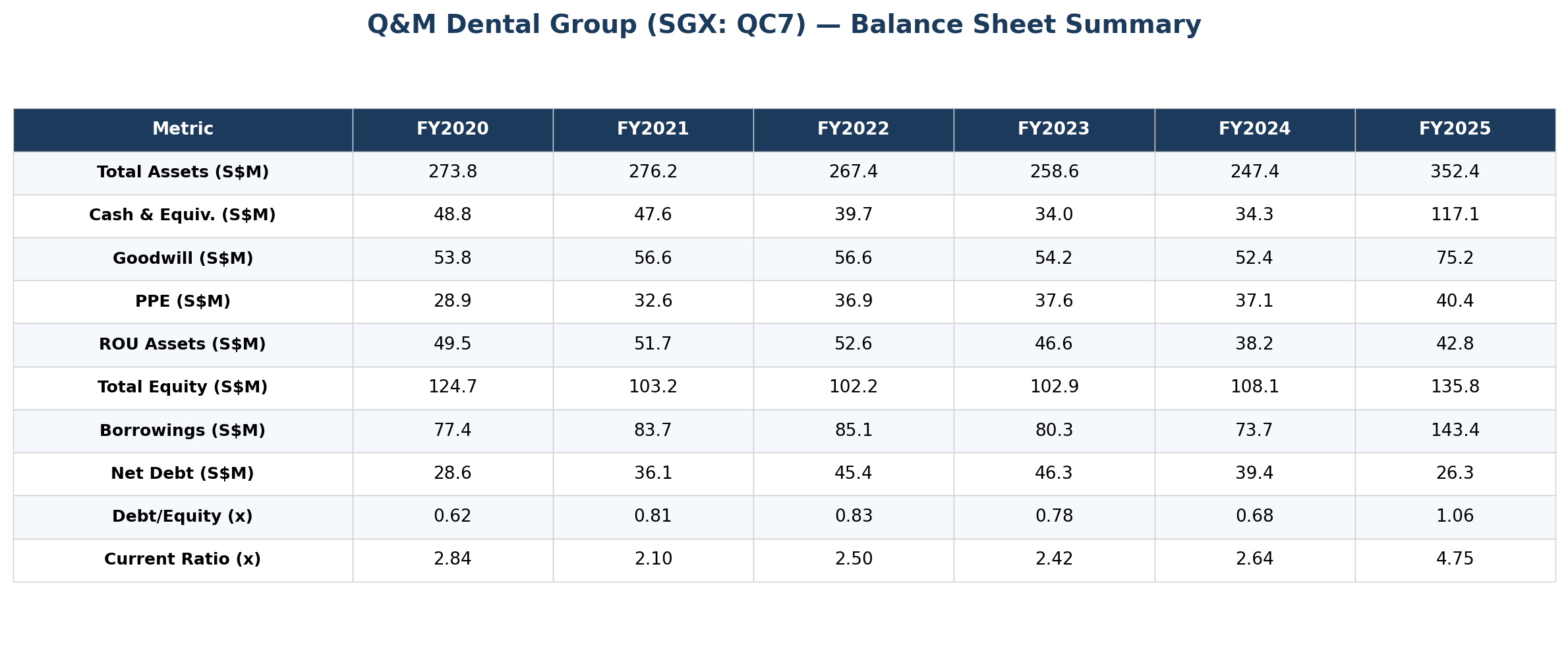

Balance Sheet: From Conservative to Leveraged

The balance sheet has undergone a significant shift. Prior to FY2025, Q&M maintained a relatively conservative balance sheet with net debt of S$39–46 million and a debt-to-equity ratio of 0.68–0.83x. The S$130 million MTN issuance changed this materially.

As at 31 December 2025, total borrowings (including finance leases) stood at S$143.4 million against cash of S$117.1 million, giving a net debt of just S$26.3 million. However, this is somewhat misleading: the cash is earmarked for acquisitions. If the Australian deal (AUD 144.5M ≈ S$130M) closes, the cash will be substantially deployed, and net debt could rise to S$100M+ depending on the financing mix.

Goodwill increased from S$52.4 million to S$75.2 million following the Aoxin consolidation. This will grow further if the M&A pipeline closes. NAV per share is S$0.1105 (equity attributable to owners of the parent divided by shares outstanding), meaning the stock trades at approximately 5.4x book value on a per-share basis.

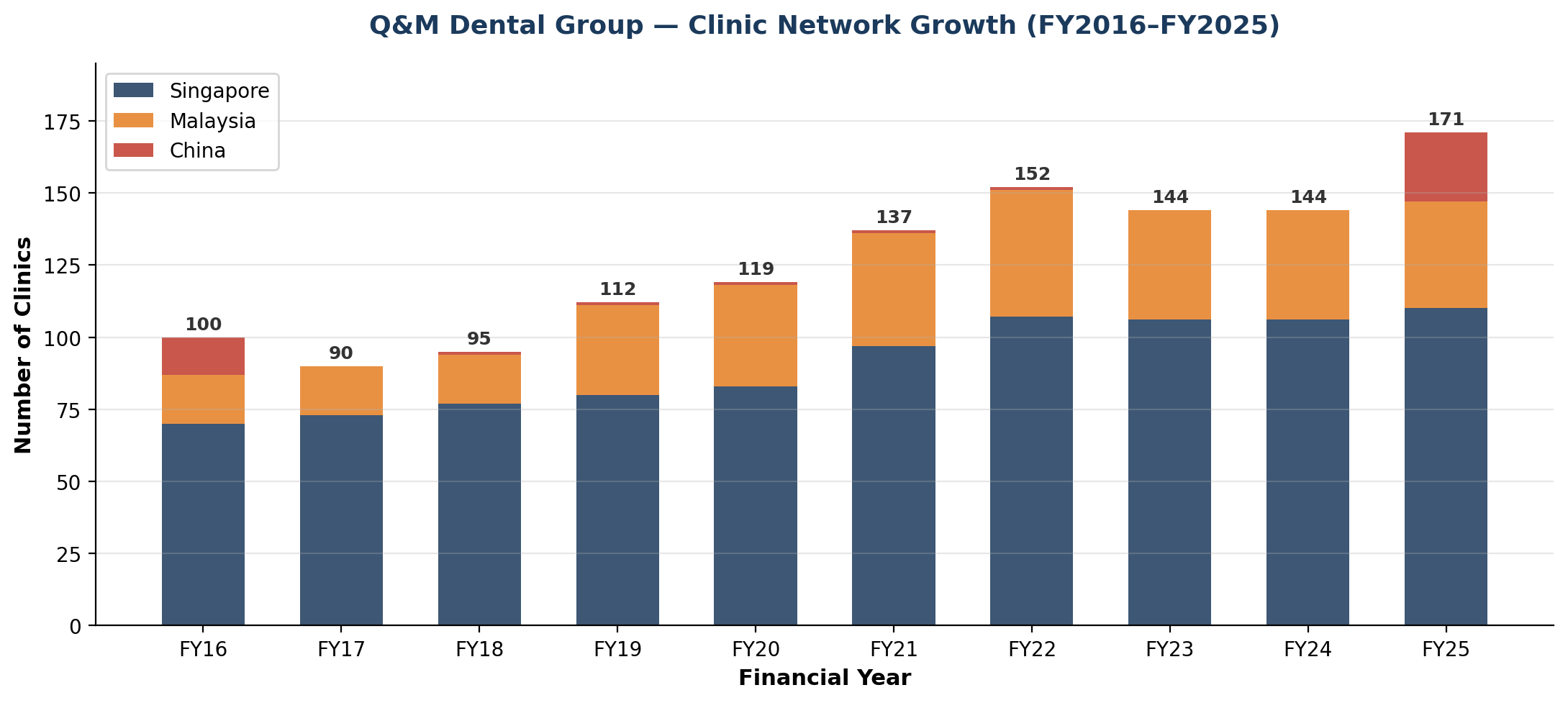

The Clinic Network: Scale as Moat

Q&M’s network of 110 dental outlets in Singapore represents the single largest private dental chain on the island. For context, Singapore has approximately 1,400 licensed dental clinics [8]; Q&M operates roughly 8% of them. The next largest chain is significantly smaller.

This scale provides several advantages. First, it gives Q&M bargaining power with landlords and suppliers. Second, it enables a training and talent pipeline through the Q&M College, where the company can recruit, train, and rotate dentists across its network, which is difficult for smaller players to replicate. Third, the CHAS (Community Health Assist Scheme) subsidy framework favours larger chains that can absorb the administrative burden of subsidy claims and fee benchmark compliance.

The enhanced CHAS subsidies effective from October 2025, covering additional restorative procedures and expanding coverage to 1.7 million cardholders [6], are a structural tailwind. Q&M’s clinics are CHAS-accredited, and management noted a roughly 3% revenue boost from the subsidy enhancements in H2 2025. The upcoming Flexi-MediSave expansion (mid-2026) allowing seniors to use S$400/year for dental work at CHAS clinics should provide further support [6].

The Johor-Singapore Special Economic Zone: Threat and Opportunity

The most disruptive near-term development for Singapore’s dental market may not come from competitors or regulation. It may come from infrastructure. The Johor Bahru–Singapore Rapid Transit System (RTS) Link, scheduled to open in December 2026, will connect Bukit Chagar in Johor to Woodlands North in Singapore with a design capacity of 10,000 passengers per hour [11]. Combined with the broader Johor-Singapore Special Economic Zone (JS-SEZ) framework, this creates a step-change in cross-border accessibility.

The implications for dental care are significant. Routine dental procedures in Johor cost 40–70% less than in Singapore. A scaling and polishing that costs S$100–180 in a Singapore private clinic runs RM80–150 (S$25–45) across the Causeway. With the RTS Link reducing crossing time to minutes rather than the current hour-plus queue at the land checkpoints, the calculus for price-sensitive Singaporean patients shifts dramatically. This is particularly relevant for elective and cosmetic procedures — crowns, veneers, implants, where the price differential runs into thousands of dollars.

Q&M is uniquely positioned on both sides of this equation. It operates 37 clinics across Malaysia — with locations in Kuala Lumpur, Selangor, Negeri Sembilan, Malacca, and Johor, more than any other Singapore-listed dental chain. If patient flow moves south, Q&M captures some of that demand in its Malaysian clinics rather than losing it entirely. However, the risk to Singapore same-store revenue is real: Q&M’s 110 Singapore outlets generate 84% of group revenue, and any meaningful patient outflow would hit the highest-margin part of the business.

Management has acknowledged the JS-SEZ in the AR2025 Operations Review, noting that Q&M continues “to explore opportunities to grow our dental business, particularly within the Johor–Singapore Special Economic Zone, with the upcoming Rapid Transit System expected to enhance connectivity and support growth in Johor.” Notably, management frames the RTS Link as a growth opportunity for its Malaysian clinics rather than a cannibalization risk to Singapore — investors should weigh whether this framing adequately addresses the downside scenario. H2 2026 same-store revenue trends will be the first real data point once the RTS Link comes online.

Singapore’s Demographic Tailwind: Ageing by the Numbers

While the JS-SEZ creates near-term uncertainty, Singapore’s demographic trajectory is an unambiguous structural tailwind for dental care demand. By 2030, 24% of Singapore’s resident population will be aged 65 or older, up from 18.4% in 2023 [5]. This is one of the fastest ageing populations in the world.

The dental implications are acute. Among Singaporeans aged 65 and above, approximately 69% wear dentures and dental disease prevalence is significantly higher than in younger cohorts [7]. Periodontal disease, tooth loss, and the need for prosthetic and restorative work all increase sharply with age. The Ministry of Health’s expansion of CHAS subsidies and the Flexi-MediSave dental benefit are direct policy responses to this demographic reality [6].

For Q&M, this means the addressable patient base for its highest-frequency services (dentures, crowns, extractions, periodontal treatment) is growing structurally, and government subsidies are reducing the out-of-pocket barrier. The company’s HDB heartland clinic locations are precisely where Singapore’s elderly population is concentrated.

The M&A Bet: Going Regional

The most significant strategic shift in Q&M’s 30-year history is happening right now. The company has simultaneously announced three major international expansion initiatives:

Australia (AUD 144.5 million). In March 2026, Q&M signed a non-binding MOU to acquire a leading Australian dental group operating 40+ clinics across NSW, VIC, QLD, TAS, and ACT with approximately 120 dentists. The purchase includes a profit guarantee of 5–8 years. To understand the significance of this deal, consider the market Q&M is entering: Australia’s dental industry is worth approximately A$13 billion annually and growing at roughly 3% per year [10], with no single dominant national chain. The market has been undergoing PE-driven consolidation — 1300 Smiles was acquired by BUPA in 2021, Abano Healthcare (NZ-listed, with Australian operations) was taken private by Adams & Co, and several mid-tier chains have attracted private equity interest. Q&M is entering this consolidation wave as a listed strategic buyer with a dental operating playbook, which differentiates it from pure financial buyers. The AUD 144.5 million price tag, however, makes this Q&M’s largest-ever acquisition by a wide margin and represents a market-entry bet where the company has zero operating history.

Thailand (30+ clinics). In October 2025, Q&M signed a non-binding MOU to acquire a Thai dental group focused on cosmetic and aesthetic dentistry, also with a profit guarantee.

China (via Aoxin Q&M). With Aoxin now a subsidiary, Q&M is deploying capital through it to acquire dental chains in China beyond Aoxin’s existing northeastern base. Two MOUs have been signed totalling approximately RMB 420 million (S$77M), targeting clinics in southern China.

The strategy is a “partnership-driven acquisition model” where founders receive a mix of cash and Q&M equity, aligning incentives. If all three deals close, Q&M could grow from approximately 161 dental outlets to potentially 300+ within two years, with a medium-term target of 300–400 clinics.

The risk is obvious: three major cross-border acquisitions simultaneously, funded partly by debt, in markets the company has limited experience operating in (Australia and Thailand are entirely new). Integration risk, currency risk, and execution risk are all elevated. This is what makes Q&M a coin flip: the upside from successful execution is transformative, but the company is attempting it all at once with no margin for error.

Competitive Advantages and Their Durability

Q&M’s moat rests on four pillars.

Network density in Singapore. With 110 outlets, Q&M has the largest private dental footprint. This is difficult to replicate because good clinic locations (typically in HDB heartlands and shopping centres) are scarce, and the company has 30 years of landlord relationships. Durability: strong in Singapore, not yet established regionally.

Talent pipeline and the dentist shortage. The Q&M College of Dentistry, now EduTrust-certified for four years, provides a training advantage. The company employs 270 dentists and can offer them a career progression path across its network. This matters more than it might appear: Singapore faces a genuine supply constraint in dental professionals. The country’s only domestic dental school (NUS Faculty of Dentistry) graduates approximately 50–60 dentists per year [9], and foreign-trained dentists must pass a rigorous licensing examination. The total number of registered dentists in Singapore is roughly 2,600 [8], serving a population of 5.9 million. This supply bottleneck is Q&M’s single biggest constraint on organic growth (you cannot open new clinics without dentists), but it is simultaneously a structural moat: any competitor looking to build a rival chain faces the same limited talent pool and the same multi-year lead time to train and credential new practitioners. Durability: strong — the licensing regime and limited training capacity are structural, not easily disrupted.

CHAS accreditation and government relationships. As the largest CHAS-accredited dental chain, Q&M benefits disproportionately from subsidy enhancements. The upcoming requirement for non-accredited clinics to be offboarded by December 2026 further entrenches incumbents [6]. Durability: strong, but dependent on government policy.

Founder leadership. Dr Ng Chin Siau controls approximately 56% of shares through Quan Min Holdings and has been CEO since founding the company. This provides strategic continuity but creates key-man risk. Durability: inherently fragile.

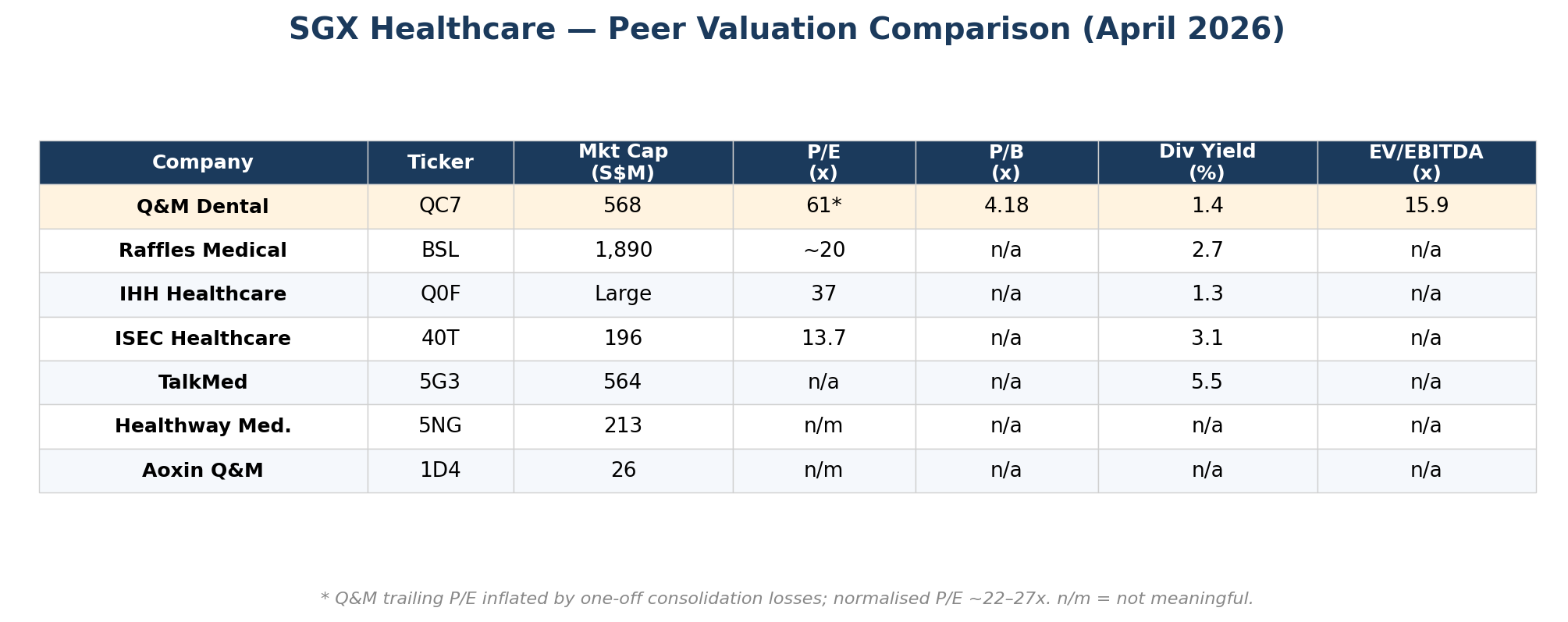

Valuation: What You Pay vs. What You Get

Q&M’s valuation is complicated by the noisy earnings picture. The metric that matters most here is the normalised P/E, because reported earnings are so distorted by one-offs that trailing multiples are meaningless, and EV/EBITDA doesn’t capture the finance cost burden from the new S$130 million debt.

Trailing P/E: 61x [1]. This is based on FY2025 reported PATMI of S$9.3 million, which is distorted by a S$4.2 million loss on the deemed disposal and consolidation of Aoxin Q&M and EM2AI, S$2.4 million MTN interest, and PSP-related expenses. This is not a meaningful number.

Normalised P/E: 22–27x. Using adjusted PATMI of S$17 million (excluding one-offs), the P/E is approximately 33x. Using core dental profit of S$30.4 million and attributing it more generously, the multiple drops further. Morningstar calculates a normalised P/E of 22.4x [2].

EV/EBITDA: 15.9x [1]. EBITDA was S$37.8 million in FY2025. At an enterprise value of S$671 million [1], this is roughly in line with IHH Healthcare but significantly above Raffles Medical.

P/B: 5.4x — NAV per share is S$0.1105 (based on equity attributable to parent of S$104.4 million divided by approximately 947 million shares). At S$0.60, the stock trades at a substantial premium to book. Third-party data providers report P/B ratios in the range of 4.2–5.4x depending on whether total equity (including minority interests) or parent-only equity is used. Either way, the premium reflects the market’s view that Q&M’s intangible assets (brand, network, relationships) are worth significantly more than their accounting value.

Dividend Yield: 1.4% [2]. At S$0.0082 per share, the yield is modest. However, management has historically been flexible with dividends, paying 4 cents in FY2021 (7% yield at the time) and as low as 0.69 cents in FY2023.

Relationship with Aoxin Q&M (SGX: 1D4). Aoxin’s market cap is just S$26 million [3] despite operating 24 facilities in China. Q&M’s 52.65% stake is worth roughly S$13.5 million at market, a tiny fraction of Q&M’s S$568 million market cap [1]. If Aoxin’s China expansion succeeds, there could be significant value embedded in this subsidiary. If it fails, the write-downs would be manageable relative to Q&M’s overall business.

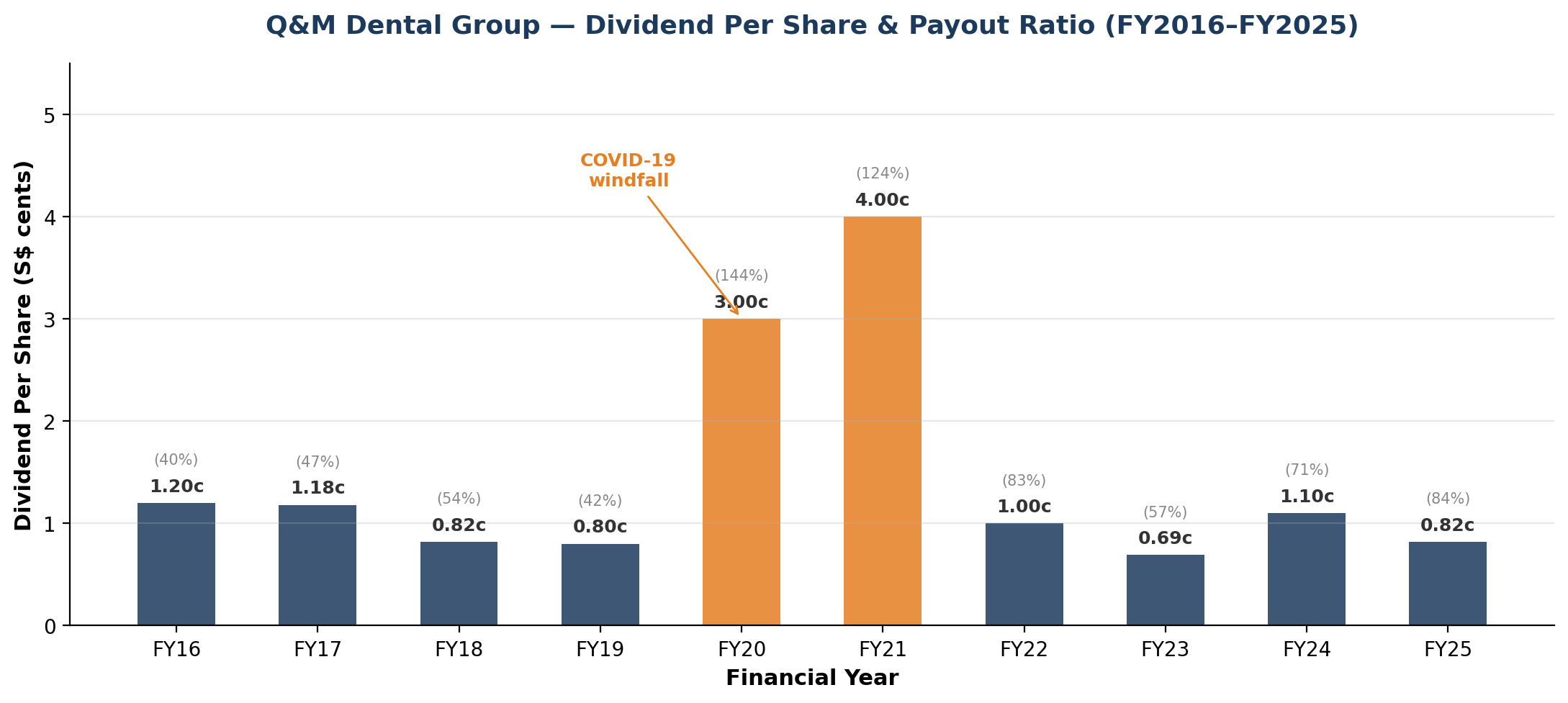

Dividend History: Feast and Famine

Q&M’s dividend track record is lumpy. During the COVID windfall years (FY2020–21), the company paid out S$0.03 and S$0.04 per share, extraordinary payouts funded by extraordinary testing profits. Since then, dividends have normalised to S$0.0069–S$0.011 per share, with payout ratios of 57–83%.

In FY2025, the payout ratio was 83% of reported earnings but only about 46% of core dental profit, suggesting the current S$0.0082 per share dividend is sustainable even without M&A-driven earnings growth.

For yield-focused investors, Q&M is not the right vehicle at current prices. The 1.4% yield is below the SGX healthcare average. The investment case here is about capital appreciation from the M&A-driven growth thesis, not income.

Key Growth Drivers (2026–2030)

1. Australian dental market entry. If the AUD 144.5M acquisition closes, Q&M immediately gains scale in a large, fragmented, and high-margin developed market. Australia’s dental industry is approximately A$13 billion [10], with no single dominant chain. The profit guarantee de-risks the near-term earnings impact.

2. Enhanced CHAS subsidies and Flexi-MediSave. The expansion of government dental subsidies is a multi-year tailwind for Singapore revenue. Q&M is the largest beneficiary by virtue of its network size. The Flexi-MediSave expansion in mid-2026 will further boost demand at CHAS clinics.

3. China expansion via Aoxin. Aoxin’s move into southern China through acquisitions diversifies away from its northeastern base. China’s dental market is growing rapidly. Private dental chains are consolidating in Tier 1–2 cities, and Q&M has a platform to participate.

4. Thailand entry. Cosmetic and aesthetic dentistry in Thailand is a growing niche, driven by both domestic demand and medical tourism. The 30-clinic acquisition would provide immediate market presence.

5. Technology and EM2AI. Q&M’s investment in dental technology through its subsidiary EM2AI deserves more attention than it typically receives. EM2AI is developing AI-assisted dental imaging and treatment planning tools — essentially using machine learning to analyse dental X-rays, detect pathologies, and recommend treatment options. The technology is still in its early commercial stages, and Q&M has not disclosed standalone revenue or profitability for EM2AI. What is clear from the annual reports is that EM2AI is being positioned as both an internal efficiency tool (improving diagnostic speed and consistency across 270 dentists) and a potential external licensing play. If the technology proves clinically robust, it could be deployed across the entire expanded clinic network post-acquisition — creating operating leverage that is distinct from simply adding more clinics. For now, EM2AI remains more of an R&D cost centre than an earnings contributor, but it is the kind of optionality that could differentiate Q&M from pure brick-and-mortar dental chains in 3–5 years.

Macro Environment: Headwinds the Market Isn’t Discussing

No analysis of Q&M is complete without acknowledging the macro backdrop. The US–China trade war has intensified through 2025–2026, with US tariffs of 10–26% now applied across ASEAN imports. Singapore’s Ministry of Trade and Industry (MTI) has upgraded its 2026 GDP growth forecast to 2.0–4.0% [4], after the economy expanded 5.0% in 2025, and business confidence surveys show softening consumer sentiment.

Dental care occupies an unusual position in a downturn. Basic dental services (check-ups, fillings, extractions) are relatively recession-resilient; toothache doesn’t wait for an economic recovery. However, elective and cosmetic procedures (orthodontics, veneers, implants, whitening) are highly deferrable and carry the highest margins. If consumer confidence weakens, these procedures are among the first discretionary healthcare expenses to be postponed. Q&M does not break out its revenue between basic and elective procedures, which makes it difficult to model the sensitivity. As a rough guide, dental industry surveys suggest that elective and cosmetic work typically accounts for 25–35% of private dental revenue in developed Asian markets (an estimate, not a verified Q&M-specific figure).

The tariff environment [12] also creates indirect risk for Q&M’s China operations. Aoxin Q&M’s patient base in northeastern China is concentrated in provinces with heavy manufacturing exposure. A trade-war-induced slowdown in Chinese industrial activity could depress dental demand in precisely the regions where Aoxin operates.

More broadly, if Singapore's growth disappoints the upgraded forecast — not the base case, but tariff uncertainty makes it possible — Q&M’s fixed-cost base (clinic leases, salaried dentists, equipment depreciation) means operating leverage works in reverse. A 5–10% decline in same-store revenue would flow through to a disproportionately larger decline in operating profit, given that employee costs alone account for 58% of revenue. The company — listed in November 2009, after the Global Financial Crisis — has never stress-tested its clinic economics through a genuine consumer recession as a public company. COVID was a supply-side demand shock with a massive government spending offset, not a consumer spending contraction.

Major Risks and Bear Case

Execution risk on concurrent M&A. Three major cross-border acquisitions simultaneously is ambitious for a company of Q&M’s size. Each market has different regulatory, cultural, and operational challenges. The management team’s experience is overwhelmingly in Singapore and Malaysia.

Leverage risk. The S$130 million MTN at 3.95% adds approximately S$5.1 million in annual interest expense. If the Australian deal is partly debt-funded, leverage could increase further. In a rising-rate environment, this is a drag on earnings.

Key-man risk. Dr Ng Chin Siau is the founder, CEO, and controlling shareholder. The company’s strategic direction, acquisition strategy, and talent relationships are heavily concentrated in one individual. There is no disclosed succession plan.

Integration risk. Dental practices are relationship-driven businesses. When you acquire a clinic, the dentist might leave, and take the patients with them. Profit guarantees provide protection but only for 5–8 years.

Aoxin Q&M drag. The China operations through Aoxin have been loss-making at the associate level for several years. Now that Aoxin is consolidated, these losses flow through Q&M’s P&L. If the China expansion fails, impairment charges could be significant (goodwill from Aoxin is already S$22+ million).

Currency and interest rate risk. Q&M’s regional expansion introduces multi-currency exposure that the company has not historically managed. Revenue will soon be earned in SGD, MYR, RMB, and AUD — each with different drivers and volatility profiles. The Australian dollar has weakened against the SGD in recent quarters, meaning AUD-denominated earnings will translate into fewer Singapore dollars. The RMB faces structural pressure from the US–China trade war [12]. On the financing side, the S$130 million MTN at 3.95% fixed rate is well-structured, but any additional debt to fund the Australian acquisition may carry a higher coupon in the current rate environment. Total finance costs rose from S$5.4 million in FY2024 to S$6.4 million in FY2025 — and will rise further if the M&A pipeline is partly debt-funded.

Regulatory risk. Changes to CHAS subsidies, dental licensing regulations, or foreign ownership rules in target markets could impact growth plans.

Management Quality and Capital Allocation

Dr Ng Chin Siau has led Q&M from one clinic to over 160 dental outlets over 30 years, an impressive track record of organic and acquisitive growth. The management team is small and lean, with CFO Ng Sook Hwa (since 2002, CFO since 2022) and COO Dr Ang Ee Peng Raymond providing continuity.

The board has been strengthened with the appointment of independent chairman Ted Tan (former Deputy CEO of Enterprise Singapore) and Professor Chew Chong Yin (former Dean, NUS Faculty of Dentistry). These appointments bring M&A expertise and dental industry credibility.

Capital allocation has been mixed. The COVID-era dividends (S$0.04/share declared for FY2021) were generous. Cash dividends paid to equity owners totalled S$48.8 million during calendar year 2021 (this figure includes both FY2020 final dividends and FY2021 interim dividends paid during that year), a level of distribution that proved unsustainable as testing profits evaporated. Share buybacks have been more disciplined, with the company repurchasing shares at prices below current levels.

The S$130 million MTN issuance was well-timed (3.95% fixed rate), and the recent allocation of up to 90 million shares for buyback provides flexibility.

Insider buying by Quan Min Holdings (Dr Ng’s vehicle) in April 2026, totalling approximately S$4.6 million, is a positive signal.

One underappreciated aspect of Q&M’s corporate profile is its community dental programme. The company operates a free dental clinic providing pro bono dental care to low-income patients, one of very few listed healthcare companies in Singapore to run a sustained charitable healthcare service rather than writing a cheque to a foundation. For ESG-focused investors increasingly screening healthcare companies on social impact metrics, this is a tangible differentiator. It also speaks to the company’s social licence to operate as the largest private dental chain in a market where dental care affordability is a growing policy concern.

Who Owns Q&M: The Shareholder Register

Understanding who owns Q&M is critical to understanding how this stock trades, and what happens if things go wrong.

As at 1 April 2026, the top 20 registered shareholders hold 82.6% of shares outstanding [14]. Only 33.9% of issued shares are in public hands. The register is dominated by three distinct groups:

The Founder Block (55.8%). Dr Ng Chin Siau’s control over Q&M flows primarily through Quan Min Holdings Pte Ltd, which holds 528.3 million shares — 236.7 million registered under its own name (25.0%) and 291.6 million held via various nominees (30.8%), totalling 55.79% of shares outstanding [14]. Dr Ng holds 49.80% of Quan Min Holdings directly and is deemed interested in a further 121,200 shares held by his spouse, giving him a total deemed interest of 55.80% [14]. He also holds 6.6 million shares (0.70%) in his own name. Two other entities with the Quan Min name — Quan Min Plus (1.82%) and Quan Min Plus 2 (0.79%) — appear in the top 20 register, but the AR2025 does not list them as giving Dr Ng any deemed interest; their beneficial ownership is not disclosed [14]. Taking only the disclosed interests, Dr Ng’s effective voting power is approximately 56.5% — an outright majority. He can pass or block any ordinary resolution unilaterally. For investors, this means governance is effectively a one-man show: whatever Dr Ng wants to do, including the current triple-acquisition strategy, will happen unless it requires a supermajority vote. The recent April 2026 purchases by Quan Min Holdings (approximately S$4.6 million in open-market buying) reinforce that the founder is putting personal capital behind the M&A thesis at current prices.

The Tsao Family / OCTAVE Block (6.8%). IMC Dynamic Investments holds 64.1 million shares (6.77%), making it the only other substantial shareholder besides Dr Ng [14]. IMC Dynamic is wholly owned by IMC Heritas Investments, which is in turn wholly owned by Tsao Pao Chee Group [14], a multi-generational Singaporean family conglomerate (the family describes itself as fourth-generation [15]) with interests spanning shipping, real estate, and healthcare-focused impact investing through its OCTAVE Capital arm. This is not a passive index fund parking capital. It is a strategic family office with a stated focus on healthcare investments across Asia [15]. Their presence at 6.8% as at April 2026 suggests alignment with Q&M’s regional healthcare expansion thesis. SGX substantial shareholder disclosure rules require notification when crossing the 5% threshold, so we know IMC Dynamic has remained above 5% continuously — but movements within that band are not publicly disclosed, and we cannot confirm the exact size of their position at any earlier point.

Nominee, Brokerage, and Individual Accounts. The remaining top 20 shareholders fall into two categories. The first is custodian and brokerage accounts — OCBC Securities (8.7%), Raffles Nominees (8.6%), Phillip Securities (7.2%), KGI Securities (6.5%), Sing Investments & Finance Nominees (5.0%), DBS Nominees (3.8%), and several smaller custodians including Citibank, HSBC, Maybank, UOB, Moomoo, and iFAST nominees [14]. These accounts collectively hold a large share of the register, but without beneficial ownership disclosure it is impossible to determine how much of this block is institutional versus high-net-worth retail. No single institutional fund has disclosed a substantial (5%+) position in Q&M. Among US-registered funds, SEC filings show Dimensional Fund Advisors (DFA) holding Q&M through its small-cap international index funds [16] — a passive, systematic allocation rather than a conviction bet. Non-US institutional holders would not appear in SEC filings and could hold positions through the nominee accounts above. The second category is named individuals: Chan Pui Kee (1.55%) and Lai Ming Chun (1.38%) are the largest individual holders outside the Ng family [14]. Their relationship to the company, if any, is not disclosed in the AR2025.

What This Means for the Investment Thesis. The shareholder structure has three important implications.

First, liquidity is thin. With approximately 56% locked up by the founder and 6.8% by a strategic family office, only about a third of shares trade freely. This amplifies price moves in both directions, partly explaining the 114% rally from the 52-week low. It also means any attempt to build or exit a meaningful position will move the price.

Second, institutional underownership is both a risk and an opportunity. Third-party ownership analyses estimate institutional ownership at less than 5% [16], meaning Q&M lacks the analyst coverage and fund flows that typically support valuation re-ratings. However, if the M&A strategy executes well and the company’s market cap grows into the S$800M–1B range, it could cross the threshold for inclusion in more small-cap indices and attract passive fund inflows — a catalyst that is entirely absent today.

Third, minority shareholder protection is a legitimate concern. With 55.8% control through Quan Min Holdings alone, Dr Ng has the votes to approve related-party transactions, share issuances, and strategic pivots without minority consent. The partnership-driven acquisition model — where founders of acquired businesses receive Q&M equity — means dilution is a structural feature of the growth strategy, not a one-off event. The board’s independent directors (Ted Tan, Prof Chew Chong Yin) provide some governance guardrails, but the power asymmetry is stark. Investors buying at S$0.60 are essentially betting on Dr Ng’s judgment and integrity with limited structural protections beyond SGX listing rules. The coin flip, ultimately, lands on one man’s ability to execute.

Bull vs Bear Investment Thesis

The Bull Case

Q&M is at an inflection point. The core Singapore dental business is growing steadily, generating S$30+ million in annual profit with strong operating cash flow. The enhanced CHAS subsidies provide a structural tailwind. The S$130 million war chest enables transformative M&A. If the Australian, Thai, and Chinese acquisitions all close with profit guarantees, FY2027–28 earnings could step-change higher. The profit guarantees alone suggest EPS could more than double from FY2025 levels. The stock trades at a normalised P/E of 22–27x, which is reasonable for a healthcare company with multi-year growth visibility. The founder’s 56% stake and recent insider buying provide alignment. Illustrative scenario (not a price target): S$0.65–0.75, implying 10–25% upside from S$0.60.

The Bear Case

The stock has already run 114% from its 52-week low [1], and much of the M&A optionality is priced in. Three concurrent cross-border acquisitions by a management team with limited international experience is high-risk. The S$143 million in debt creates earnings drag through S$6.4 million in annual finance costs. Aoxin Q&M has been a persistent drag on earnings and is now fully consolidated. If any major deal falls through or integration stumbles, the stock could de-rate quickly. The trailing P/E of 61x leaves no margin for disappointment. Key-man risk is unmitigated.

Consider a simple stress scenario: if a macro downturn drives a 5–10% decline in same-store revenue across Singapore — not implausible if the JS-SEZ diverts patients to Johor while a tariff-induced slowdown dampens elective procedure demand — the impact on profitability is amplified by Q&M’s fixed-cost structure. Employee costs (S$115 million) and lease depreciation (S$13.8 million) are largely fixed in the near term. A 7% revenue decline (roughly S$14 million) would fall almost entirely to the bottom line, potentially halving core dental operating profit. The company has never been tested through a genuine consumer recession as a listed entity — and it would enter one at higher leverage than at any previous point in its history.

Illustrative scenario (not a price target): S$0.40–0.50, implying 15–33% downside from S$0.60.

What Could Break the Thesis

For bulls: If the Australian deal falls through (it’s a non-binding MOU), the growth narrative collapses. If integration of Aoxin leads to sustained losses that offset Singapore profits, the quality of the business deteriorates. A sharp deterioration in Singapore dental demand (recession, regulatory change) would undermine the base business.

For bears: If all three acquisitions close on favourable terms with strong profit guarantees, the earnings step-change could be dramatic enough to justify current valuations. A re-rating to peer multiples (IHH at 37x, Raffles at 20x) on higher earnings would drive significant upside.

The Bottom Line

At S$0.60, you are not buying a dental business. You are underwriting one man’s ability to simultaneously execute three cross-border acquisitions — in Australia, Thailand, and China — while managing S$143 million in debt, a thin public float, and a core Singapore business that has never been tested through a consumer recession.

The data says the core business deserves its premium: 5–7% revenue growth, 28% segment margins, S$35–40 million in annual operating cash flow, and a founder with 30 years of compounding behind him. But it also says Q&M has zero operating history in any of its target markets, and the entire M&A pipeline rests on non-binding MOUs.

That’s the coin flip. The fundamentals are real. The ambition is extraordinary. And the gap between the two is where the risk lives.

References

Market Data Sources

Stock Analysis (stockanalysis.com) — Q&M share price (S$0.60), market cap (S$568M), trailing P/E (61x), EV/EBITDA (15.94x), enterprise value (S$671M), shares outstanding (~947M), 52-week low (S$0.245–0.25), 52-week price change (+114%). Data as at 20 April 2026.

Morningstar — Normalised P/E (22.42x), dividend yield range (1.37–2.12%). Accessed April 2026.

Yahoo Finance / MarketScreener — Aoxin Q&M (SGX: 1D4) share price (S$0.194), market cap (~S$25.6M). Accessed April 2026.

Industry and Macro Data Sources

Singapore Ministry of Trade and Industry (MTI) — 2026 GDP growth forecast upgraded to 2.0–4.0%; 2025 full-year GDP growth of 5.0%. MTI press release, 10 February 2026. https://www.mti.gov.sg/newsroom/mti-upgrades-2026-gdp-growth-forecast-to--2-0-to-4-0-per-cent-/

National Population and Talent Division, Singapore — Population projections: 24% of residents aged 65+ by 2030, up from 18.4% in 2023. https://www.population.gov.sg/our-population/population-trends/longevity/

Ministry of Health, Singapore / CHAS.sg — Enhanced CHAS dental subsidies effective 1 October 2025; Flexi-MediSave expansion for seniors (S$400/year) effective mid-2026; non-accredited clinic offboarding by 31 December 2026; 1.7 million CHAS cardholders. https://www.moh.gov.sg/newsroom/enhanced-financing-support-for-chas-dental-procedures-and-financial-governance-of-chas-clinics/

MOH Singapore — Oral health survey data: approximately 69% denture prevalence among Singaporeans aged 65+. (Note: exact survey year varies by source; figure is from publicly available MOH oral health statistics.) https://www.ndcs.com.sg/news/patient-care/closing-the-gap-in-elderly-oral-healthcare-in-singapore-with-smartrpd

Singapore Dental Council (SDC) — Approximate number of registered dentists in Singapore (~2,600). Registry data accessed via public sources. https://data.gov.sg/datasets/d_6c8cf7ce0c6830608637418fcd0979a7/view

NUS Faculty of Dentistry — Approximate annual graduate output of 50–60 dentists. Based on publicly available faculty information. https://sgschoolkaki.com/statistics/university-graduates/dentistry

IBISWorld — Australian dental services industry: approximately A$13 billion market size, ~3% annual growth. Industry report data. https://www.aihw.gov.au/reports/dental-oral-health/oral-health-and-dental-care-in-australia/contents/costs

JB-SG RTS Link project authority — RTS Link design capacity of 10,000 passengers per hour; scheduled opening December 2026; connecting Bukit Chagar (Johor) to Woodlands North (Singapore). https://www.lta.gov.sg/content/ltagov/en/upcoming_projects/rail_expansion/JB-Singapore_RTS_link.html

US Trade Representative / Singapore government sources — US tariffs of 10–26% on ASEAN goods, referenced in the context of the 2025–2026 trade environment. https://www.aseanbriefing.com/news/u-s-tariffs-in-asia-2025-a-regional-investment-map/

Ken Research — Singapore dental services market revenue estimate (~USD 2.4 billion in 2026). https://www.kenresearch.com/industry-reports/singapore-dental-services-market

Q&M Dental Group — Statistics of Shareholdings as at 1 April 2026 (AR2025, pp.128–129). Source of: top 20 registered shareholders, substantial shareholders list, public float (33.93%), Quan Min Holdings total stake (55.79% including nominees), Dr Ng Chin Siau’s deemed interest (55.80%), IMC Dynamic Investments (6.77%), Tsao Pao Chee Group corporate chain, Quan Min Plus (1.82%), Quan Min Plus 2 (0.79%), and named individual shareholders.

Tsao Pao Chee Group / OCTAVE Capital — corporate website (tsaopaochee.com) and OCTAVE Capital website (octavecapital.co). Source of: Tsao family generational history (”fourth-generation”), OCTAVE Capital’s healthcare investment focus across Asia, and IMC Group corporate structure.

Fintel / Simply Wall St / Yahoo Finance — Institutional ownership estimates for Q&M Dental (<5% institutional), Dimensional Fund Advisors (DFA) holdings via small-cap international index funds. Accessed April 2026. Note: these are third-party estimates based on disclosed filings; actual institutional ownership may differ as non-US funds and nominee-held positions are not fully captured.

Notes on Data Integrity

FY2024 figures throughout this article use the restated numbers as reported in the FY2025 filing (Note 18), which differ from the originally published FY2024 figures. Where relevant, this is noted in the text.

Dental price comparisons between Singapore and Johor (scaling: S$100–180 vs RM80–150) are indicative ranges based on publicly available clinic fee schedules and are not sourced from a single authoritative database.

The estimate that elective/cosmetic work accounts for 25–35% of private dental revenue is an industry-level approximation, not a Q&M-specific disclosure.

Bull and bear illustrative scenarios are editorial in nature and are not derived from a formal discounted cash flow or earnings model.

All financial data sourced from Q&M Dental Group SGX filings (FY2015–FY2025) and Annual Reports. Market data as at 20 April 2026.

IMPORTANT DISCLAIMERS

General Disclaimer: This article is published for informational and educational purposes only. It does not constitute financial advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The views expressed are based on publicly available data from Q & M Dental Group (Singapore) Limited’ SGX filings and publicly accessible market data, and may not reflect the most current developments.

Not Licensed Financial Advice: The author is not a licensed financial adviser, and this publication is not issued by a holder of a Capital Markets Services Licence under the Securities and Futures Act 2001 of Singapore. This content does not fall within the definition of “financial advisory service” under the Financial Advisers Act 2001 of Singapore. Readers in Singapore should note that this content is exempt from the requirements of the Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication.

MAS Compliance Notice: In accordance with the Monetary Authority of Singapore’s guidelines, this publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, you should consult a licensed financial adviser who can provide advice tailored to your personal circumstances. Past performance of any security discussed herein is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author may or may not hold positions in the securities discussed. No compensation has been received from any company mentioned in this article.

The SEA Analyst,

I find it interesting that Q & M Dental Group (Singapore) Limited (QC7; QNM SP) recognised SGD 15 mn gain on bargain purchase from its acquisition of Aoxin Q & M Dental Group Limited (1D4; AOXIN SP).