JustCo's IPO: A S$100 Million Raise on a US$2.7 Million Profit

That works out to about 130 times earnings. GIC and Frasers are anchoring the offer anyway.

If you have rented desk space in Singapore in the last decade, you have probably worked out of a JustCo, or walked past one. The company runs flexible workspace centres in office towers from One-North to the Central Business District, the kind of place a startup takes three desks in and a multinational takes three floors. Flexible office space has gone from a fringe product to a standard line item in corporate real estate, and JustCo is one of the larger names in the region that built it.

The company behind those desks, though, has drawn far less scrutiny than the product it sells. On 22 May 2026, JustCo Holdings Limited lists on the SGX Mainboard, and the offer document gives us the first proper look at the numbers. The headline tension is visible from the first page. JustCo is raising S$100 million in gross proceeds. In its most recent financial year it earned a net profit of US$2.7 million. A raise of that size against a profit of that size implies the market is being asked to pay a very full price, and it invites the comparison every flexible-office IPO now has to answer: is this the next WeWork story, or something sturdier? We read the prospectus to find out.

From JustOffice to JustCo

JustCo began in 2011, not 2018. The 2018 date on the prospectus cover is when the current holding company was incorporated; the business is older. Founder Kong Wan Sing started it with two co-founders as “JustOffice”, a single 3,132 square foot space in Samsung Hub in the heart of the Singapore CBD. The bet was simple: office supply was tight, rents were rising, and the way companies wanted to use space was changing faster than traditional leases allowed.

Growth came in stages. Between 2017 and 2019, equity from Sansiri, GIC and Frasers Property turned a Singapore operator into a regional one, and JustCo expanded into Australia, Taiwan, Thailand, South Korea and Japan at a pace of roughly one new centre every three weeks. The pandemic was the first real test: occupancy fell to just above 60% at the worst of it. The company’s response is worth noting, because it is the opposite of the WeWork playbook. JustCo exited mainland China and Indonesia rather than defend every market. Today it operates 54 centres across 12 cities, with around 37,500 workstations, and it sells under three brands: The Collective at the luxury end, JustCo as the core premium product, and the boring office as an essentials line.

What the offer actually contains

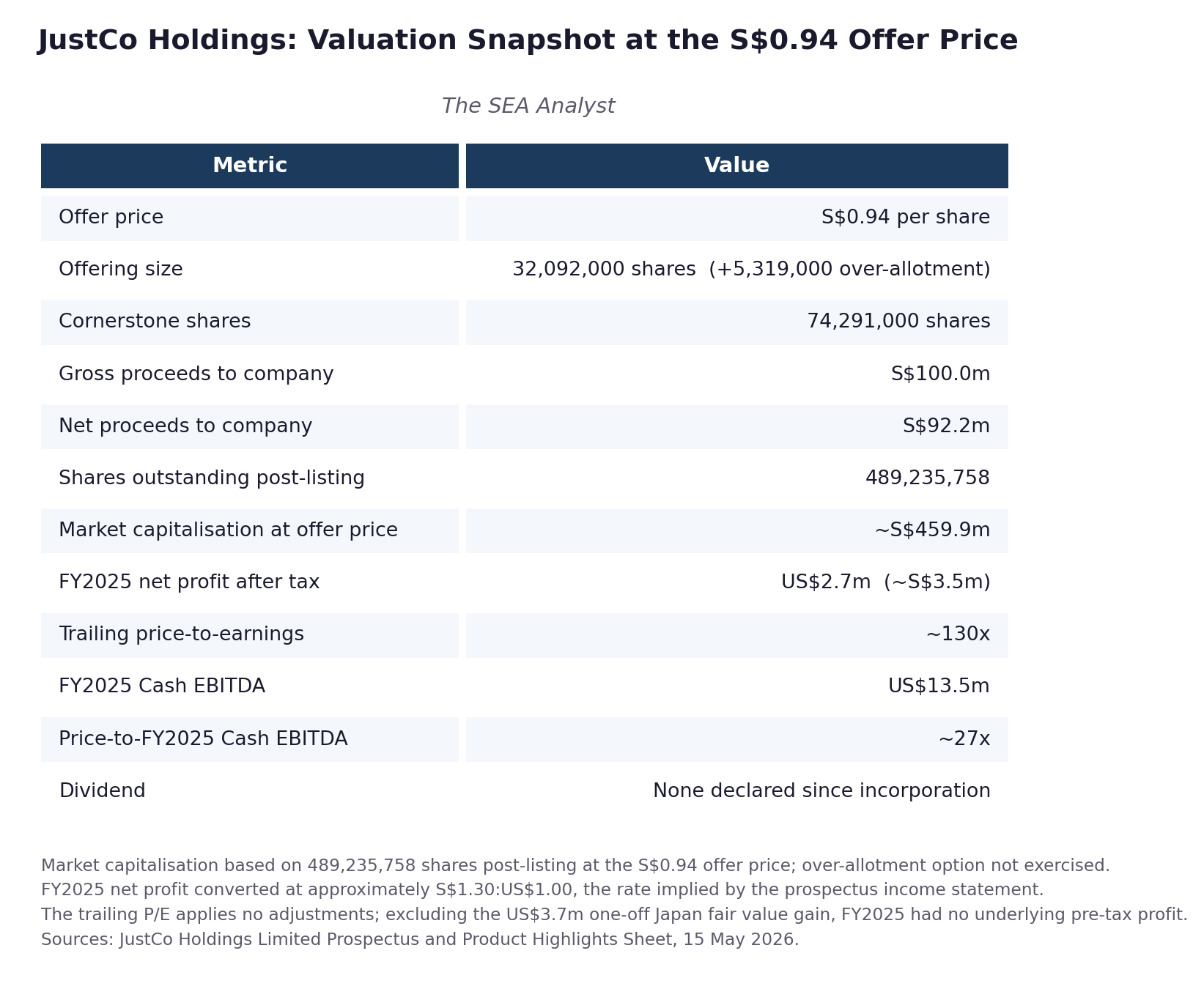

The offer is 32,092,000 new shares at S$0.94 each, with a further 5,319,000 vendor shares available through an over-allotment option. Sitting alongside it is a much larger cornerstone tranche of 74,291,000 shares. Together the new shares raise S$100.0 million gross and S$92.2 million net to the company. After listing, JustCo will have 489,235,758 shares in issue, which at the offer price puts the market capitalisation just under S$460 million.

The register is heavily anchored. GIC holds 22.74% after listing, Frasers Property and the Charoen Sirivadhanabhakdi interests hold 17.63%, and founder Kong Wan Sing’s family vehicle holds 17.79%. The cornerstone investors, a group that includes JPMorgan Asset Management, Fullerton, Maybank Asset Management, Avanda and Amova, take another 15.19%. Hsieh Fu Hua, a familiar name in Singapore capital markets, chairs the board as lead independent director.

The money has a clear job. S$81.7 million of the gross proceeds is earmarked for expansion, fit-outs and capital expenditure, with S$56.8 million of that tied to 20 committed new centres. Another S$10.0 million is for working capital, and S$8.3 million covers the fees of the offering. In total, JustCo plans to open around 28 new centres in 2026.

A small float by design, not by accident

Notice what is missing from those numbers: any meaningful sale of existing shares. The 5.3 million over-allotment is just over 1% of the company, and it comes from the Kong family’s holding vehicle. GIC, Frasers, the Kong family and Pinetree are not using this listing to cash out. That leaves an unusually small free float of about 6.6%, rising to 7.6% if the over-allotment is fully taken up. A typical SGX Mainboard listing sells 15% to 25% of the company; JustCo sold the minimum needed to raise the capital it wanted, and not a share more.

Three things follow. The deal raised what was needed and no more, which is a capital-discipline signal in a market where IPOs are often sized to deliver an exit rather than to fund growth. The existing register is genuinely committed: GIC and Frasers came in between 2017 and 2019 and are choosing to mark their investment publicly rather than monetise it. And the tradable float will grow mechanically as lock-ups unwind. The standard SGX six-month moratorium releases the cornerstone tranche around the fourth quarter of 2026, taking effective float past 21%, with the controlling-shareholder shares coming off lock-up at twelve months. The post-listing share price in those early months will therefore partly reflect scarcity rather than fundamentals, which flatters it now and creates an overhang later, when supply normalises even if nothing about the business has changed.

The point underneath all of this is that the tight float is a design choice, not a forced outcome. JustCo could have sold more shares and produced a normal float, and it chose not to. That signals confidence in being able to come back to market later, and a reluctance to dilute further at what the existing register evidently sees as a still-early price.

The financial scoreboard

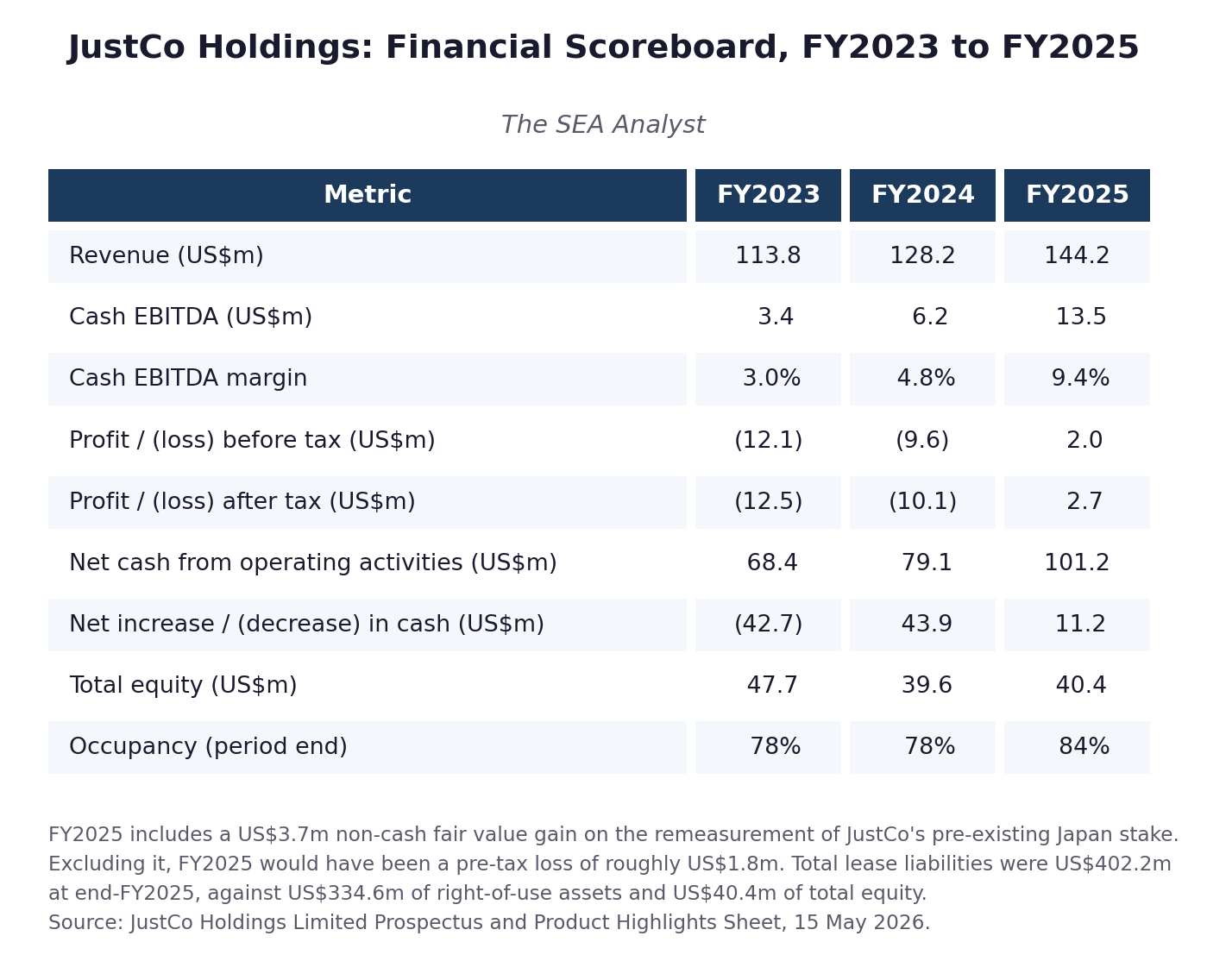

Revenue has compounded steadily, from US$113.8 million in FY2023 to US$128.2 million in FY2024 to US$144.2 million in FY2025, a little under 13% a year. The profit line is the part that needs care. JustCo lost US$12.5 million after tax in FY2023 and US$10.1 million in FY2024 before reporting a US$2.7 million profit in FY2025. That maiden profit, though, leans on a one-off. FY2025 other income included a US$3.7 million non-cash fair value gain on the remeasurement of JustCo’s pre-existing stake in its Japan operations, recognised when it bought out the rest of that business. Strip that gain out and FY2025 would have been a pre-tax loss of roughly US$1.8 million. The turn to profit is real on the reported line, but the underlying business has not quite crossed into the black yet.

The more useful trend is Cash EBITDA, the company’s measure of cash generated at centre level after actual rent is paid. It rose from US$3.4 million to US$6.2 million to US$13.5 million across the three years, and the margin widened from 3.0% to 9.4%. Occupancy improved from 78% to 84%, and the renewal rate climbed from 64.7% to 72.0%. The operating story is one of a business getting steadily more efficient as its centres mature.

The cash flow puzzle

One number in the scoreboard looks too good, and it is worth slowing down on. JustCo generated US$101.2 million of net cash from operating activities in FY2025. That is more than seven times its FY2025 Cash EBITDA of US$13.5 million, and around thirty-seven times its reported net profit. It is not a sign of a cash machine hiding inside the income statement. It is an accounting effect.

Under the lease accounting standard that applies here, the rent JustCo pays on its centres does not all run through operating cash flow. The interest portion does, but the much larger principal portion is recorded as a financing outflow. In FY2025 net cash used in financing was US$77.1 million, most of it lease repayments. So the US$101 million operating figure is, in plain terms, cash generated before paying most of the rent. The honest measure of what the business kept is further down: after rent, after capital expenditure, and after everything else, cash on the balance sheet rose by US$11.2 million. JustCo is cash generative. It is generative in the low tens of millions, not the hundred-million range the operating line first suggests.

A moat that is strongest when you need it least

A moat is whatever stops a competitor from copying a business and taking its customers. JustCo has one. The question for this offer is not whether it exists, but how well it holds when conditions turn, because the whole investment case rests on occupancy staying high and new centres filling up on schedule.

Start with what is genuinely defensible. JustCo is neither the biggest flexible-office operator in Asia nor the oldest. It competes against IWG, the listed owner of Regus and Spaces that has run this business since 1989, against the long-established premium operators The Executive Centre and Servcorp, and against a restructured WeWork. What JustCo has built instead is density in a handful of cities. The market study commissioned for the prospectus puts its share of flexible workspace stock at around 16% in Singapore, a comparable level in Bangkok, and higher in Taipei [1]. In those cities, a corporate real estate team drawing up a shortlist of options will almost always include JustCo. Being the default option in your core markets is a real advantage, and it is the strongest layer of the moat.

But notice what that advantage depends on. A network of workspace centres is only valuable to a member when the centres are full and active. This is what economists call a network effect: the product gets better for each customer as more customers use it. In a good year, full centres generate referrals, landlords compete to host JustCo, and the density looks like a fortress. In a bad year, the same network is a row of half-empty floors with the rent still due on every one of them. The moat, in other words, is pro-cyclical. It reinforces itself when times are good and erodes when times are hard. That is the opposite of what an investor wants from a moat, because the entire point of a moat is to protect a business when the cycle turns against it. JustCo’s is strongest exactly when it is needed least.

The management-contract model softens this, but only on one side. When a landlord funds the fit-out and shares the revenue, a weak year hurts JustCo less on those centres, because the pain is shared with the building owner. That protects the balance sheet. It does not make a single member more loyal, so it is not a demand-side moat.

And the demand side is where the moat is thinnest. JustCo’s members stay an average of about 15 months, so the moat has to be re-won, customer by customer, on a rolling basis: roughly 28% of the workstations due for renewal in 2025 were not renewed. The product itself is substitutable, because one operator’s private office differs from another’s mainly on location, price and fit-out quality, all of which a well-funded rival can match. Landlords who have watched the model work can choose to run flexible space themselves. And the city-level density, real as it is, sits inside a small niche. Flexible space is only about 6% of all office space in the region, so a 16% share of Singapore’s flexible market works out closer to 1% of the city’s total office stock. JustCo is a meaningful operator in a young, still-small slice of the property market, not an entrenched one in a large and mature market.

The WeWork question

The comparison is unavoidable, so we will take it head on. JustCo itself seems to know it: a sign in its centres reads “Let’s Make Work Better”, and the wordplay against the name of its largest cautionary tale is almost certainly deliberate. JustCo’s prospectus does not mention WeWork in its risk factors, but the structural feature that broke WeWork is present here too. JustCo signs leases with initial terms generally running three to ten years. Its members sign up for an average of about 15 months. That gap between long, fixed commitments on one side and short, cancellable revenue on the other is the central vulnerability of the leased-office model. It is why, at end-FY2025, JustCo carried US$402.2 million of lease liabilities against just US$40.4 million of total equity. When occupancy holds, this works. When occupancy falls, the rent does not.

What is genuinely different is almost everything else. WeWork at its 2019 IPO attempt carried around US$47 billion of lease commitments against roughly US$4 billion of rental income, was burning cash at scale, and had governance problems that became their own story. JustCo is a fraction of that size, grew at a measured pace, walked away from China and Indonesia rather than chase every flag on the map, and runs about three-quarters of its mature space under management contracts in which the landlord funds the fit-out and shares the risk. It is cash positive after everything. Its register is GIC and Frasers, not a single dominant venture backer. The honest answer is that JustCo is not WeWork. But it shares WeWork’s core structural risk, and an investor buying the IPO is buying that risk at a price that leaves little room for the occupancy cycle to disappoint.

What the market is asking you to pay

At S$0.94, the post-listing market capitalisation is just under S$460 million. Against FY2025 net profit after tax of US$2.7 million, about S$3.5 million at the rate the prospectus uses, that is a trailing price-to-earnings multiple of roughly 130 times. And because the maiden profit rests on a one-off gain, the underlying business produced no profit to multiply at all. On the company’s preferred measure, the offer values JustCo at around 27 times its FY2025 Cash EBITDA of US$13.5 million. There is no dividend policy, and none has ever been paid.

We are deliberately not putting a forward number on this article. Whether 130 times trailing earnings is the wrong price or simply an early price depends entirely on what FY2026 and FY2027 look like as 28 new centres open and season, and that forward build is a separate piece of work. What we will say plainly is what the offer price is, and what it is not. It is not a value entry point. It is a growth price, and it asks the buyer to underwrite the next two years of expansion going broadly to plan.

The bull, the bear, and the honest answer

The bull case is that JustCo is a real franchise at an inflection. Occupancy and renewal rates are both rising, the Cash EBITDA margin has tripled in three years, and the management-contract model lets the company keep growing without putting every fit-out dollar on its own balance sheet. The flexible-office market across Asia Pacific is still lightly penetrated relative to mature markets like central London, which leaves room to grow into [1]. And the quality of the register matters: GIC, Frasers and a serious cornerstone book do not anchor a business they expect to unravel.

The bear case is that the price gives you no margin for error. The maiden profit is flattered by a one-off, the structural lease-versus-membership mismatch is real and large, the free float is thin enough to make the early share price as much about scarcity as about fundamentals, there is no dividend to wait on, and the raise itself adds 28 centres of fresh lease liability and the associated drag before those centres mature. Every one of the bull points depends on the occupancy cycle staying friendly, and the moat that is supposed to hold occupancy up is, as we have seen, weakest precisely when the cycle turns against it.

The honest answer is that both cases are true at once, and the IPO price is what forces the choice. JustCo has built something durable enough that GIC and Frasers want to own it, and fragile enough, structurally, that the WeWork question is fair to ask. At nearly S$460 million on a business that has not yet made an underlying profit, the market is being asked to pay for the growth before it arrives. Whether that is a price worth paying is the question the offer puts to each investor, and it is not one we will answer for them.

Notes on data integrity

All financial figures in this article are drawn from the JustCo Holdings Limited Prospectus and the accompanying Product Highlights Sheet, both dated 15 May 2026. JustCo reports in US dollars; the offer is priced in Singapore dollars. Where we convert between the two, we use the rates the prospectus itself uses: approximately S$1.30 to US$1.00 for the FY2025 income statement, and S$1.2784 to US$1.00 as at the prospectus’s Latest Practicable Date. The trailing price-to-earnings multiple, the price-to-Cash EBITDA multiple, the post-listing market capitalisation and the underlying pre-tax loss excluding the Japan fair value gain are our own calculations from disclosed figures. “Cash EBITDA” is the company’s defined measure and is not a standard accounting metric; we use it as the company presents it. Flexible-office market penetration data is from the CBRE Independent Market Research Report commissioned for and reproduced in the prospectus. This is a focused first-look analysis of the offer, not a full research initiation, and it does not attempt a forward earnings estimate or a valuation target.

References

[1] CBRE Pte Ltd, “Market Due Diligence Report on Flexible Working Sector in Asia Pacific”, Independent Market Research Report reproduced as Appendix C in the JustCo Holdings Limited Prospectus dated 15 May 2026.

[2] JustCo Holdings Limited, “Prospectus dated 15 May 2026” and “Appendix 3 Product Highlights Sheet dated 15 May 2026”, lodged with and registered by the Monetary Authority of Singapore. Available via the SGX-ST website and the MAS OPERA portal.

[3] WeWork: comparative figures on its withdrawn September 2019 initial public offering and its lease commitments are drawn from contemporaneous public reporting; WeWork subsequently filed for Chapter 11 bankruptcy protection in November 2023.

IMPORTANT DISCLAIMERS

This article is published for informational and educational purposes only. It does not constitute financial or investment advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The author is not a licensed financial adviser under the Financial Advisers Act 2001 of Singapore. This content is exempt from the requirements of the Singapore Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication. This publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, readers should consult a licensed financial or investment adviser in their relevant jurisdiction. Past performance is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author may or may not hold positions in the securities discussed. No compensation has been received from any company mentioned in this article.

Very good analysis, especially on how IFRS 16 'overstates' operating cash flow.

I would also say that JustCo is highly leveraged. It doesn't borrow from the banks, but it 'borrows' from its lenders through leases.

Borrowing from the bank to buy an office is similar to leasing it from the landlord.

An analyst told me leases are not debt because he can always just walk away from the leases. The landlord can't do anything. I am not convinced.

JustCo is a good example why leases are debt.