HRnetGroup: A S$336m Treasury, a Dividend to Watch, and a Profit Pool Leaving Singapore

A family owns nearly 80% of HRnetGroup (SGX: CHZ) and decides what happens to the cash. We separate what is owned from what a minority can actually reach.

In March 2026, the chief corporate officer of HRnetGroup, Adeline Sim, sat for an interview and described a change in how her clients now talk. The first question a company asks is no longer whether to hire in Singapore or to send the role to a cheaper market. It is whether the role needs a person at all. “Can you just use a chatbot or something?” she summarised. “Now even in Jakarta, people will say, can you just use AI?” [1]

That is the demand backdrop for Singapore’s largest home-grown recruiter, and it shows up in the filings with some precision. HRnetGroup’s gross profit from its Singapore operations has now fallen for four consecutive years. In FY2025 it dropped another S$4.1 million. The company still reported its highest net profit since FY2023, S$51.2 million, up 15% year on year. Both of those statements are true at the same time, and reconciling them is the entire exercise.

The headline most readers will have seen is the one about the cash. Management describes a “cash moat” of about S$336 million, which against a market value of roughly S$737 million is a striking figure: close to half the company’s market capitalisation sits in cash and near-cash. The number is real. What is less examined is how much of it a minority shareholder can actually reach, what the operating business looks like once you strip the income that cash throws off, and whether the dividend that pays you to wait is as secure as the balance sheet makes it look.

Those questions live in the segments, not the headline profit. We start there.

How the Company Was Built

HRnetGroup was founded in Singapore in 1992 by Peter Sim, who remains executive chairman at roughly 73 years of age and who, his daughter notes, “has always said he wants to work until he’s 100.” [1] The business began as a single recruitment firm and grew into what the company describes as the largest Asia-based recruitment agency in the Asia-Pacific outside Japan, operating today across 18 Asian cities.

The structural decision that defines the company came early: the co-ownership model. Rather than running branches staffed by salaried managers, HRnetGroup makes its senior people part-owners of the specific city-business they run. These “Business Leaders” hold equity in their own units; their appointments are disclosed individually through SGX filings, and by April 2026 the count had reached 47, up from 22 at the 2017 IPO. Management attributes the company’s consistency, having stayed profitable through every major crisis in its 33-year history, to this structure, and the mechanism is plausible: the people generating the gross profit have a direct claim on it and a strong reason not to leave. We cannot prove the model caused the profitability rather than accompanying it, but it is the most credible explanation on offer, and it is the organising principle of the whole company.

HRnetGroup listed on the SGX mainboard on 16 June 2017 at an offer price of S$0.90, opening at S$0.95. It was nearly a Hong Kong listing instead. By Adeline Sim’s account, cornerstone investors offered the same valuation in either venue and the family chose Singapore because it is headquartered there: “why not be where we are wanted.” [1] The stock has spent most of its listed life below its offer price, touching an all-time low of S$0.41 in March 2020 during the COVID crash and, on management’s own description, hovering between 75 and 80 cents since mid-2021. [1]

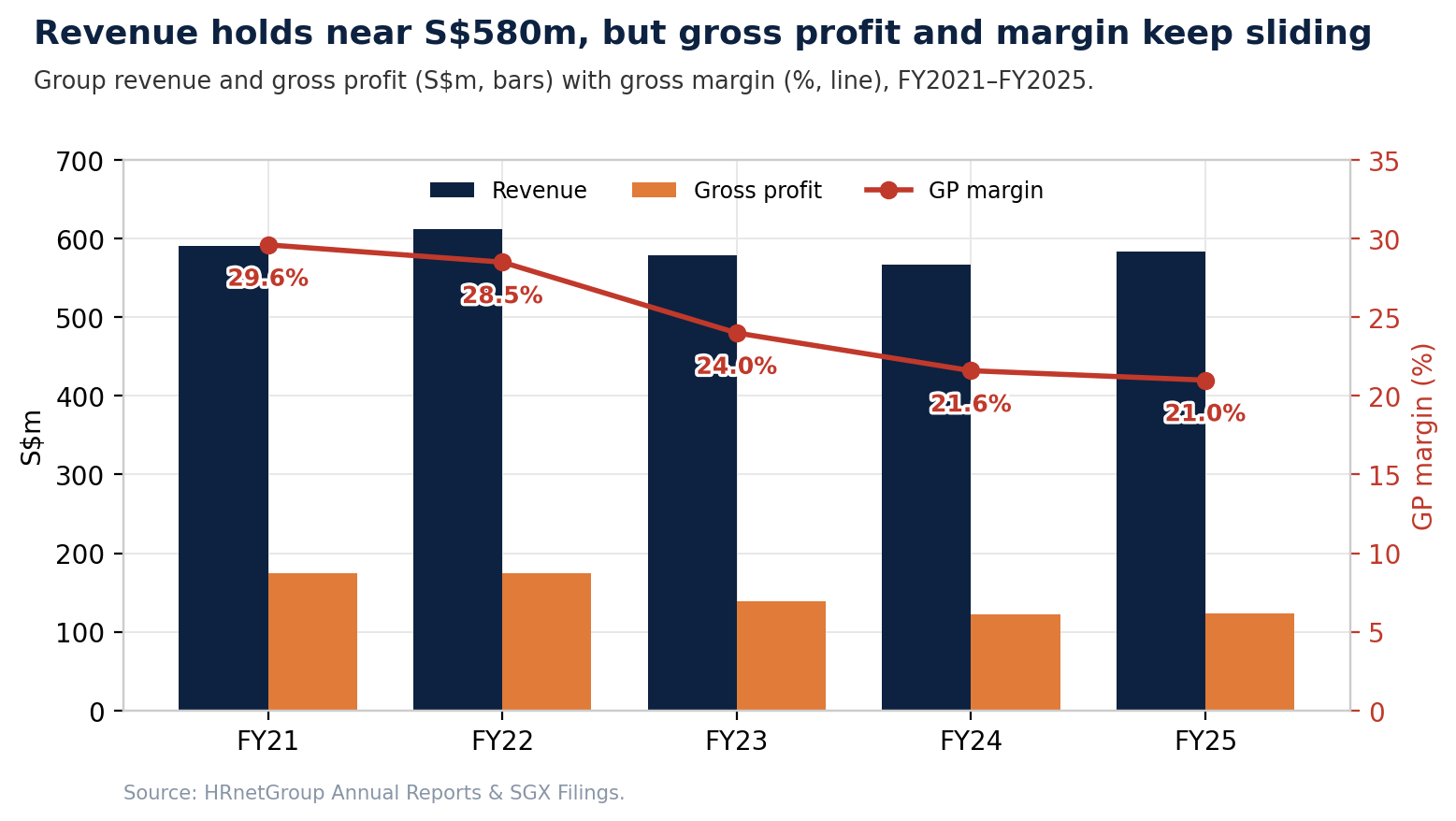

Gross profit plateaued at its peak across FY2021 and FY2022, S$174.9 million and S$174.2 million respectively, with attributable profit around S$67.5 million in FY2022, a figure Adeline Sim confirmed directly in a July 2024 interview. [2] What followed was a sustained decline in the core business that the headline profit number has since partly masked. Gross profit fell to S$139.0 million in FY2023, then S$122.2 million in FY2024, and was essentially flat at S$122.9 million in FY2025. That is a 29% fall in gross profit from the peak. Net profit fell less dramatically, from S$67.5 million to a low of S$44.5 million in FY2024, before recovering to S$51.2 million in FY2025, and the reason it recovered is the heart of this article.

The most recent piece of corporate history is the September 2025 incorporation of AllwaysFirst in Ho Chi Minh City, the group's 18th city and its entry into Vietnam, a wholly owned subsidiary focused on professional recruitment in technology. [4] Management has said directly that "any immediate contribution from the new subsidiary may not be material." [4] We treat it accordingly.

What the Company Actually Does

HRnetGroup sells two things, and they look almost nothing alike in the accounts.

The first is Professional Recruitment, the placement of permanent staff, typically mid-to-senior white-collar roles. The company is paid by the employer, not the candidate, and the standard form is a one-time placement fee set as a percentage of the successful hire’s first-year remuneration. Most of that work is contingency-based, meaning the fee is earned only if the client actually hires the candidate, with senior executive search more often run on staged retainers. In FY2025 this segment produced revenue of S$55.8 million and gross profit of S$55.6 million. The reported gross margin of about 99.6% is an accounting artefact, not an economic one: in permanent placement there is no separately allocated cost of sales, so the fee is essentially all “gross profit,” and the cost of the consultants who earn it sits below the gross-profit line as employee expense. The consultant who makes the placement is paid a base salary plus commission on the fees they bring in, and under the co-ownership model the Business Leader running that desk owns a share of the unit’s profit, which is the alignment mechanism described earlier. So the right way to judge this segment is not its headline margin but its gross profit per consultant and its placement volume. On that basis FY2025 was flat: PR gross profit grew S$0.7 million, or 1.3%, and placement volumes were modest. This is the high-margin, cyclical engine, and right now it is idling.

The second is Flexible Staffing, the supply of contract and temporary workers, where HRnetGroup employs the worker itself and bills the client. The economics are a spread: HRnetGroup pays the contractor a wage and bills the client a charge rate set above it, keeping the difference. The contractor wage is the cost of sales here, which is why the FY2025 gross margin was only 12.2%, down from 12.6%, against the near-100% optical margin of permanent placement. Because HRnetGroup pays the worker before the client pays HRnetGroup, it also funds the payroll float across a one-week-to-two-month billing cycle, so this engine ties up working capital as well as earning a thinner margin. In FY2025 it produced revenue of S$524.1 million, up 3.2%, and gross profit of S$63.8 million, down marginally. This is the lower-margin, higher-volume, more defensive engine. It is also where Singapore's weakness is most visible, because Singapore is where most of the flexible-staffing book sits.

A third line, reported as "Others," houses Octomate and assorted payroll and employer-of-record services. It produced revenue of S$4.1 million, broadly flat, and gross profit of S$3.5 million, up about 7%, in FY2025. Octomate is a cloud workforce-management and instant-payment platform that HRnetGroup took a 51% stake in during October 2022; its payment engine integrates with HRnetGroup's own Ease Works app to give contractors earned-wage access the moment a timesheet is approved. [3] Daily active users have grown from about 3,000 at acquisition to, on the company's own reporting, roughly 15,000 by January 2026 [14], with Amazon, H&M and Hyundai among named users. [3] We read Octomate less as a standalone software business than as an internal tool that lowers friction and supports retention in flexible staffing, which is why the flat "Others" revenue (a line that also bundles payroll outsourcing and employer-of-record services) is probably the wrong test of its value. Either way we attach no number to it, and the investment case does not need it.

A client has alternatives, and they differ by segment. For permanent recruitment it can run the search in-house, use a rival agency, or lean on AI sourcing tools. For flexible staffing, which is closer to a commodity, large clients run vendor-management systems that pit suppliers against each other on price, or bring payroll in-house. That commodity dynamic is what the 12.2% flexible-staffing margin, and its slippage, looks like in the accounts. What actually defends the business against these alternatives, and where AI helps rather than hurts, is the subject of the moat section.

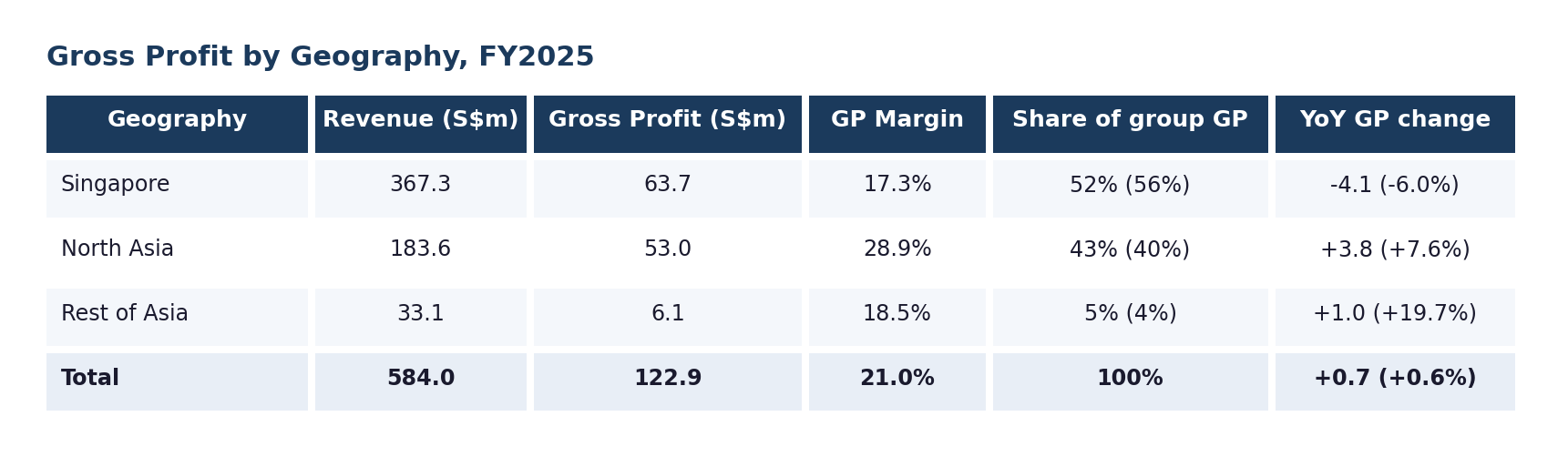

Geographically, FY2025 is where the real story sits.

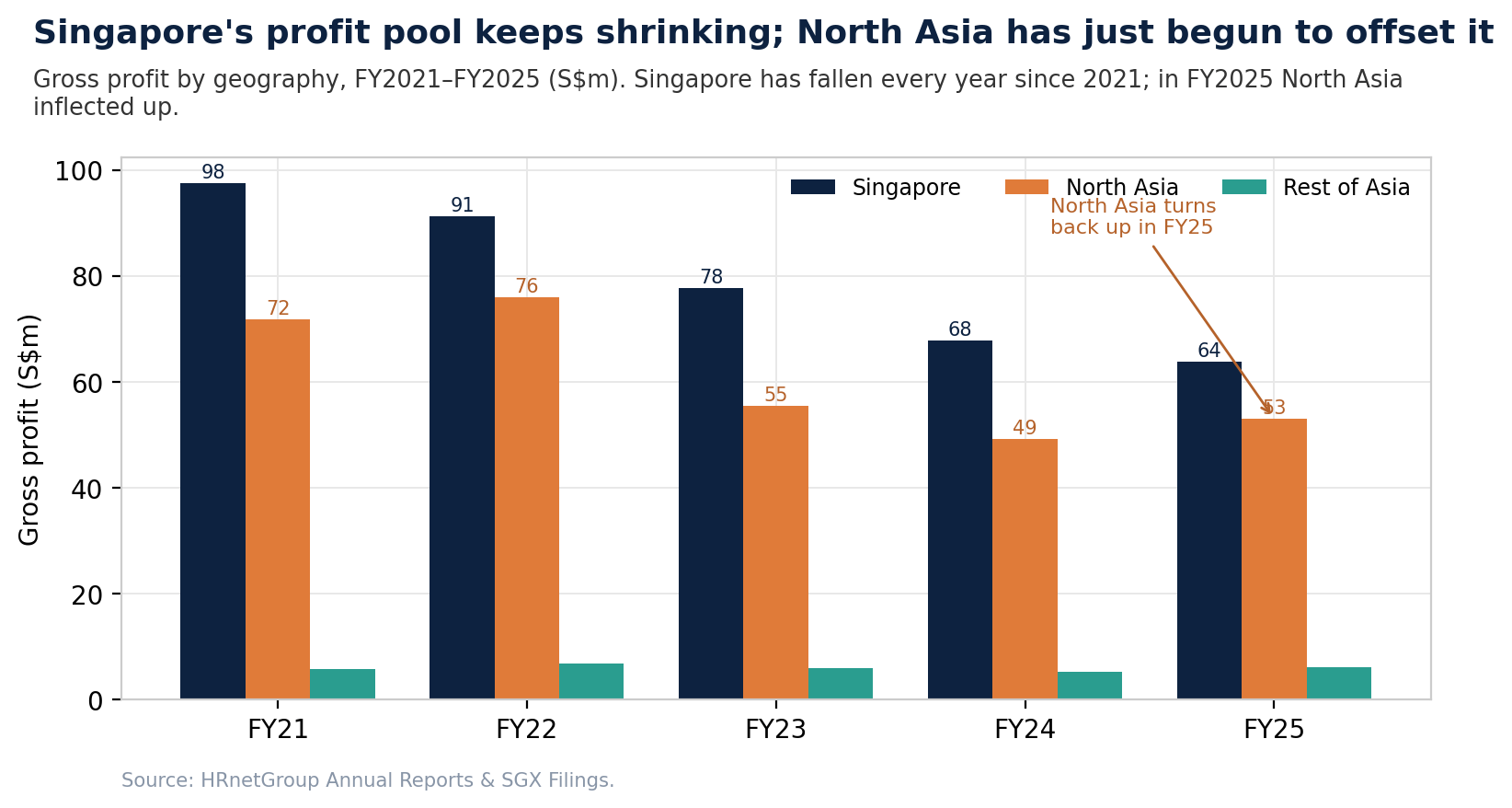

Read across the bottom row first. Group gross profit grew S$0.7 million, six-tenths of one percent. Now read the column above it. Singapore gross profit fell S$4.1 million. Everything outside Singapore grew S$4.8 million, almost exactly offsetting the decline. That near-perfect cancellation is the company in FY2025: a shrinking home market held level by a growing regional one. The blended gross margin outside Singapore, about 27.3%, is materially higher than Singapore’s 17.3%, so as the mix shifts away from Singapore the group’s average margin quality improves even when total volume does not. That improvement is not purely geographic, though. North Asia’s higher margin reflects a heavier weighting to permanent recruitment, which carries a near-100% accounting margin, while Singapore’s lower margin reflects its heavier flexible-staffing mix at about 12%. So the shift out of Singapore is also a shift from lower-margin, defensive flexible staffing toward higher-margin but more cyclical permanent recruitment. That lifts margin quality and, at the same time, makes the earnings mix less defensive than the income framing implies. It is also the only thing standing between the group and an outright decline in gross profit.

The last structural fact a reader needs concerns the treasury, because it dominates the valuation. We deal with the precise composition in the investment case. Here we state only what it is: as at end-FY2025 the group held S$262.9 million of cash and equivalents, plus credit-linked notes and government securities of S$62.7 million and S$10.7 million of gold and commodity-linked assets, which management aggregates to a “cash moat” of about S$336 million. [1] Strategically held quoted equities are excluded from that figure. There is no bank debt. The only borrowings are S$14.7 million of lease liabilities under accounting rules for office space.

The Industry: A Cycle Down and a Structural Question

Two forces act on this business, and they should not be confused. One is cyclical and global. The other is structural and local.

The cyclical force is the worldwide downturn in professional recruitment that began after the 2021 to 2022 hiring boom. It is not specific to HRnetGroup, and the peer numbers make that clear. Hays, the UK-listed global recruiter, reported net fees (its term for gross profit) of £972.4 million for the year to June 2025, down 13% year on year, and cut its core dividend by 59%. [7] PageGroup reported gross profit of £769.5 million for 2025, down 7.6%, with operating profit down 59%. [8] Robert Half’s revenue fell 7.2% to US$5.38 billion, with operating income down roughly two-thirds. [9] Against that field, HRnetGroup’s flat gross profit is, relatively, a good outcome: it held up better than the three large global recruiters, though not better than Staffline, which grew gross profit 10.6% after restructuring out of a loss-making division. [10]

The structural force is the one that should hold an investor's attention, because it is specific to where HRnetGroup makes most of its money. Singapore gross profit has fallen for four straight years. The proximate cause in FY2025 was a soft labour market: by the first quarter of 2026, Singapore job vacancies had eased to 73,300 from 77,700 three months earlier, the ratio of vacancies to unemployed persons had slipped to 1.46 from 1.58, and the share of firms expecting to hire in the next three months had dropped sharply, from 54.6% in February to 44.6% in March. [12] A forward-looking read points the same way: employers' net hiring outlook for Singapore in the third quarter of 2026 fell to 13%, down 11 points both on the quarter and on the year, with the decline led by large organisations, whose outlook was a net negative 26% on what the survey calls optimization-led consolidation. [22]

That is cyclical softness. But layered underneath it is something management describes as a change in kind, not degree: AI is making clients more selective about whether a role exists at all, undercutting even the old labour-arbitrage logic of sending a Singapore role to a cheaper market. [1] AI cuts both ways for a recruiter, though, and we should be even-handed about it. It automates the junior, high-volume, searchable end of hiring and lets large clients source directly, which is a real threat; but it raises the value of agencies at the other end, in senior and specialist search where relationships matter, and in candidate verification, as AI-generated CVs, forged credentials and deepfake interviews make trust scarcer. [17] Which side HRnetGroup lands on depends on whether it keeps migrating its gross profit toward the specialist end, which is the stated aim of its senior-executive pivot.

One caution on the labour read: the easing in Singapore vacancies through early 2026 was concentrated in non-PMET roles, while professional and technical roles actually became harder to fill, so aggregate labour softness does not by itself prove that professional-recruitment demand is structurally weakening. [18] We cannot prove from filings how much of Singapore's decline is cyclical and how much is permanent, and we treat it as structural in the base case until the company shows stabilisation.

The offset to Singapore is geographic, and it is shifting the group's centre of gravity: North Asia's share of gross profit is rising as Singapore's falls, and it earns far more per dollar of revenue than the home market. North Asia spans seven mainland Chinese cities, the three Taiwan cities, Hong Kong, Tokyo and Seoul. The overseas shift is contractor-led: average monthly contractors rose 5.6% to 16,421, the increase coming from Taiwan, Indonesia and Mainland China (Indonesia sits in Rest of Asia) while Singapore's headcount fell. North Asia specifically drew stronger professional-recruitment placement activity in Taiwan, Mainland China and South Korea, with Thailand and Malaysia adding to the wider offset against a softer Singapore. Group-wide, demand is spread across industries rather than concentrated in any one: IT and technology is 24% of the business, of which 12% is AI-related roles, financial and insurance about 21%, and healthcare and life sciences and retail and consumer roughly 14% each. On the group's own brand job boards the overseas book runs the full range, from operational and retail staffing to executive search. [13] Rest of Asia contributed too, off a small base, with Vietnam a new market.

One scheme-level detail matters and is easy to get wrong. Singapore's Progressive Wage Credit Scheme, under which the government co-funds wage increases for lower-paid local workers, pays HRnetGroup meaningful grant income, and it runs through 2028: Budget 2026 set the co-funding rate at 30% for 2026 and 2027 wage increases, and 20% in the final year, 2028. [11] So the scheme is supported, not tapering, over the next two years. Why the S$9.2 million FY2025 grant figure still overstates the recurring level, and how that feeds the valuation, is in the normalised-earnings section.

The Moat: What Is Real and What the Numbers Will Not Support

A company with this balance sheet and this dividend invites the assumption that it must have a strong competitive position. Some of that assumption is warranted. Some of it is contradicted by the company’s own gross-margin history.

What is defensible is the co-ownership model. Making Business Leaders part-owners of their city-units creates retention a branch-and-salary rival cannot easily copy, because what holds a team in place is equity in the unit, not a salary another firm can beat. The observation the bullish reading skips is that the model has a recurring cash cost: recycling ownership interests as Business Leaders join, leave or change stakes consumed S$3.3 million in FY2025. The alignment is genuine; it is not free.

Also defensible, though not measurable from filings, is network depth in specific niches, executive and professional search in Hong Kong and mainland China, the breadth of an integrated group of around twenty brands spanning executive search, flexible staffing, employer-of-record and payroll across 18 Asian cities, and reach into the people who are not actively looking. Management's claim, which we cannot verify from the filings, is that roughly 90% of strong performers are not job-hunting, so the value is in knowing and attracting them. [1] This is also where AI sorts the business rather than simply threatening it: it commoditises the junior, high-volume, easily-sourced end, where clients can self-serve, and spares senior and specialist search, where the relationship still carries weight, which is the stated reason management is moving up-market toward C-suite roles. External evidence points the same way: in the same employer survey, having a person review resumes ranked as the most valued hiring resource, above AI screening and sourcing tools, consistent with the relationship end of recruitment holding its value even as the high-volume end is automated. [22]

The third advantage is the balance sheet, and it is the most concrete. The cash position lets HRnetGroup fund the contractor float described earlier, win large contracts capital-light competitors cannot, and acquire without raising money. Trade receivables of S$93.9 million carry a loss allowance of only S$104,000, consistent with strong collection history and a generally creditworthy client base. Part of that quality is structural: public-sector clients, which carry no credit risk, are 16% of revenue and rising, no single customer is a tenth of revenue, and the top five clients, at 17.2% of revenue between them, have been with the group an average of eighteen years. Ample working capital plus exceptional credit quality is a competitive advantage, not just a defensive buffer. In flexible staffing, which has the thinnest moat because the service is close to a commodity, these are the real defences, scale, the compliance and payroll machinery, and the capacity to fund contracts a thin rival cannot; and the cross-cutting AI disruption is met on the technology side through Octomate, the internal tool described earlier, rather than only absorbed.

What the record will not support is the claim that brand or scale protects pricing. Group gross margin has fallen from 29.6% in FY2021 to 21.0% in FY2025. That is not the margin path of a business with pricing power. Some of the fall is mix, as lower-margin flexible staffing grows relative to high-margin permanent placement, and some is genuine competitive and AI-driven pressure on the Singapore core. Either way, an 8.6 percentage-point gross-margin decline over four years is the single fact that disciplines any moat argument here. The advantages above are real. They have not prevented margin compression, and an honest moat assessment has to hold both ideas at once.

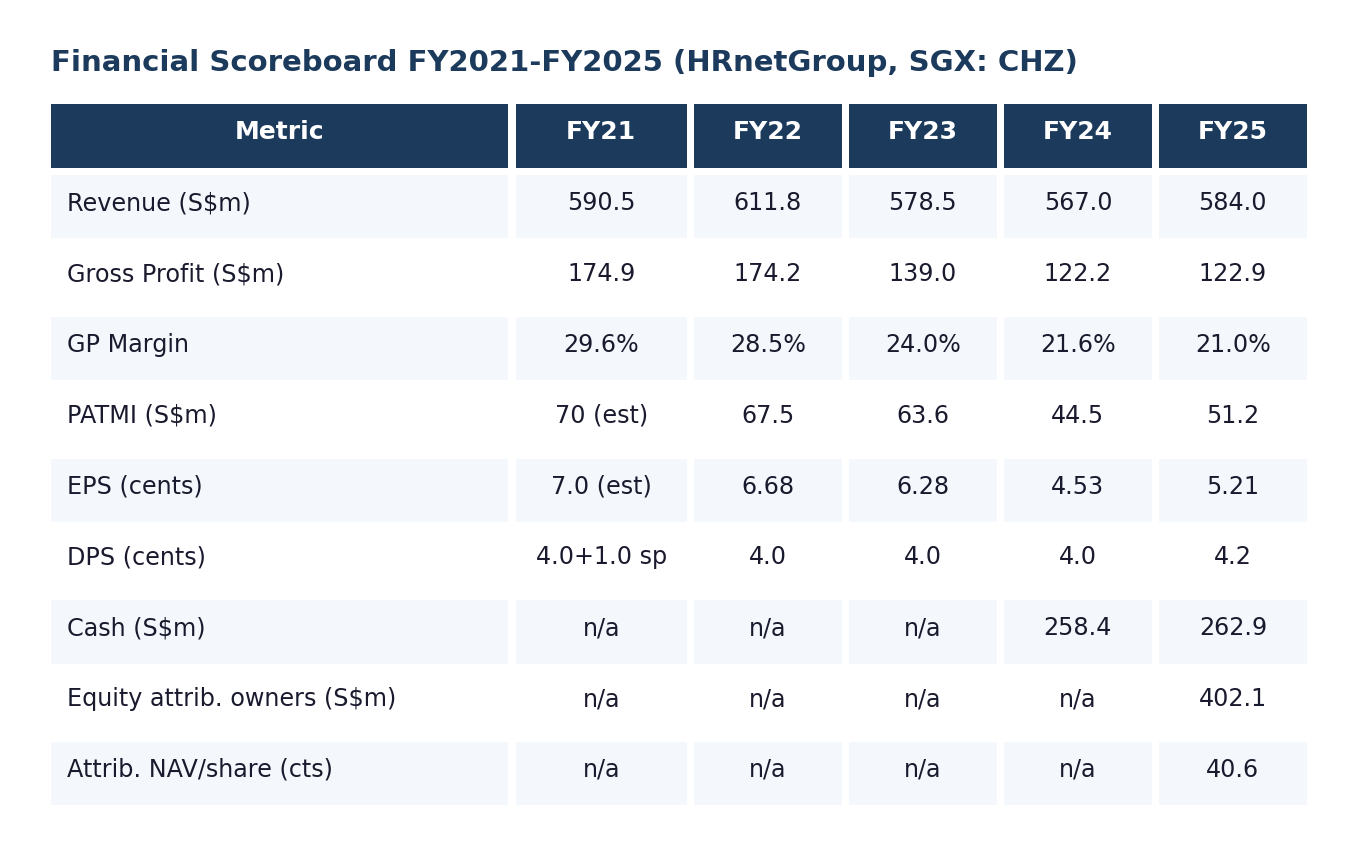

The Financial Scoreboard

Every figure below is from the company's filings, including the audited FY2021 results; FY2022's S$67.5 million attributable profit was confirmed by management directly. [2]

The shape is clear without commentary. Revenue has been range-bound around S$580 to S$610 million for five years. Gross profit and gross margin have fallen steadily. Net profit fell to FY2024 and then recovered in FY2025. The dividend has been held at 4.0 cents for four years and was raised to 4.2 cents for FY2025. A company that grows revenue slightly, earns less gross profit each year, and still raises the dividend is telling you where its priorities sit, and where the risk sits too.

Returns on Capital, Read Two Ways

On a reported basis, FY2025 return on equity was S$51.2 million of PATMI on S$402.1 million of equity attributable to owners, about 12.7% on year-end equity (13.1% on average); total equity including S$12.0 million of non-controlling interests was S$414.1 million, and we use the attributable figure throughout. That 12.7% misleads in two directions. The equity base is inflated by the treasury: roughly S$270 million earns a low yield and does almost nothing for operating returns, so the underlying operating business, which is capital-light, earns far more than 12.7% on the little capital it actually uses. Pulling the other way, the S$51.2 million is flattered by non-operating income; on normalised attributable profit of about S$38.3 million (the bridge is built in the investment case below), return on attributable equity is about 9.5% year-end, or 9.8% on average, and it is earned by a business whose gross profit has not grown in two years.

So the capital story is two-sided: a high-return operating business sitting inside a company whose blended return is mediocre because most of its capital is idle cash. Which fact matters depends on whether that idle cash ever returns to shareholders, the governance question we take up below and do not resolve in the company’s favour.

What Management Does With the Cash

For a company defined by its balance sheet, the record of what it actually does with capital is more revealing than any statement of policy, so we pulled it from the share-capital note and the statement of changes in equity rather than the headline tables.

The dividend is the primary channel and it is consistent: 4.0 cents held through FY2022 to FY2024, raised to 4.2 cents for FY2025, with a one-cent special paid in FY2021 on top of the ordinary 4.0. Cash dividends paid have run between roughly S$39 million and S$40 million in the last two years, with a higher figure of about S$52 million passing through FY2023 on dividend timing. The payout has absorbed roughly 80% of reported earnings each year.

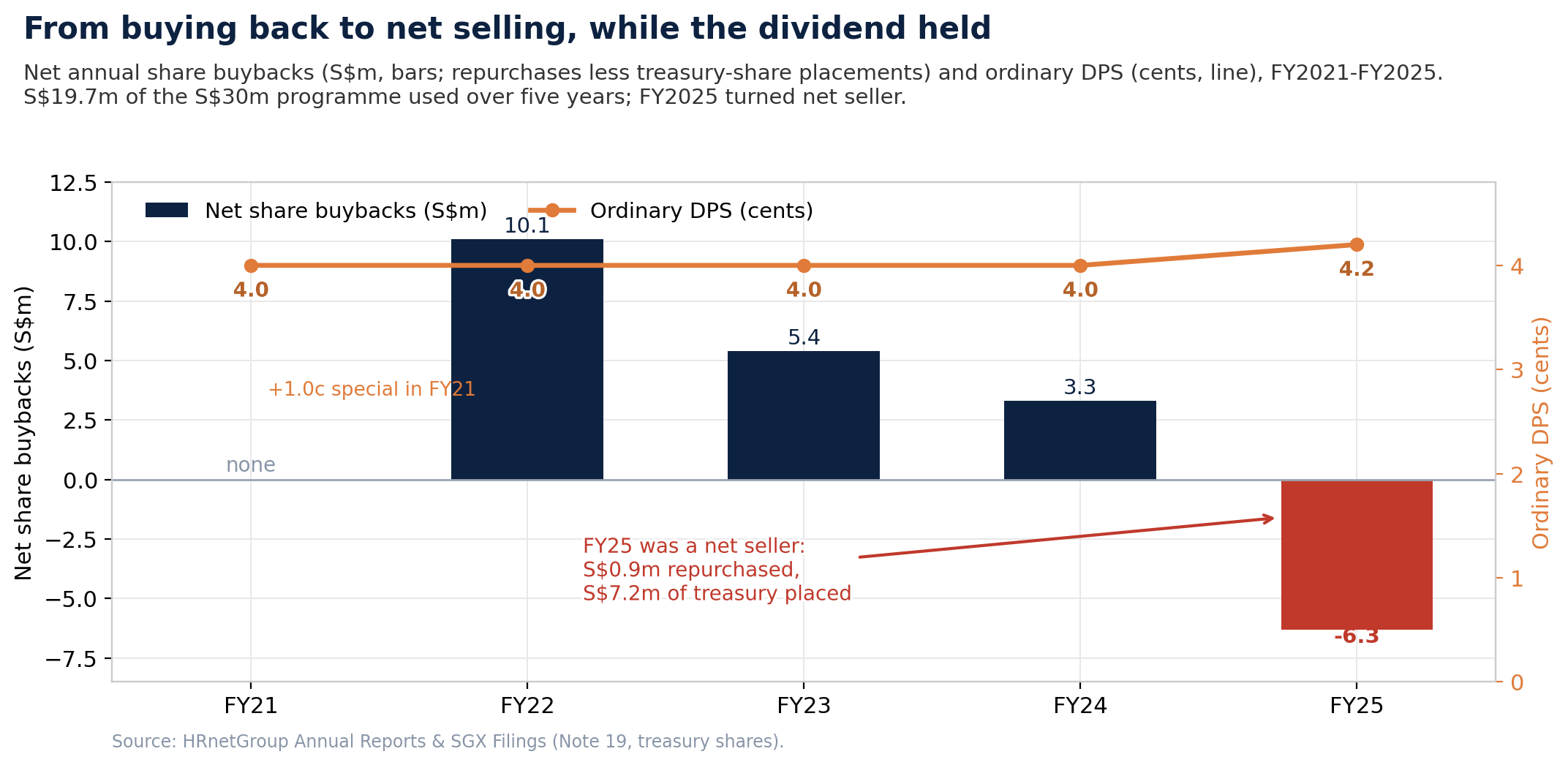

The buyback channel tells a more pointed story. The S$30 million programme launched in June 2022, near the price the stock still trades around, and the spend has fallen every year since, to just S$0.9 million in FY2025; cumulatively S$19.7 million of the S$30 million programme is used, S$10.3 million unspent. More striking, FY2025 was a net-seller year: against S$0.9 million repurchased, the company sold S$7.2 million of treasury shares, principally the October 2025 placement of 9,780,800 shares at S$0.714 to enhance liquidity and free float following a reverse inquiry. [15] The liquidity rationale is real, and a discounted placement does not by itself mean management judged S$0.714 to be fair value. But it sits awkwardly beside the rhetoric: a company that calls its shares undervalued, holding cash worth close to half its market value, was adding to supply at a discount while its buyback programme sat idle.

Keep the facts, the explanation, and the inference apart. The observed facts: the company distributed about 80% of earnings as dividends, reduced its buyback spend every year to near zero, was a net seller of its own stock in FY2025, and retained S$336 million on the balance sheet, deploying capital into growth only at the small scale of the September 2025 Vietnam start-up. Management's stated explanation is that the treasury is strategic optionality it intends to keep rather than distribute. Our inference, labelled as such, is that the declining buyback and the discounted placement are hard to reconcile with a strong conviction that the shares are cheap, and that the treasury looks retained for the long term rather than positioned for near-term return to minorities. On the facts as they stand, a minority's return comes from the dividend and operating progress, not from the treasury being put to work on their behalf, and nothing in the record points to that changing without a decision only the family can make.

The Investment Case

The central tension: reported profit versus the operating reality

In FY2025, PATMI, the profit attributable to owners of the company, rose 15.0%, from S$44.5 million to S$51.2 million. Gross profit rose 0.6%. A business whose gross profit is flat does not generate a 15% rise in attributable profit from operations. The increase came almost entirely from below the gross-profit line,