Haw Par Corporation: The Tiger Balm Conglomerate Hiding a S$3.4 Billion Portfolio

A data-driven look at the company behind Tiger Balm - and why most of its value has nothing to do with muscle rubs.

If you’ve ever used Tiger Balm, you’ve used a Haw Par product. But here’s what most people don’t realise: Tiger Balm is only the third-most important thing about this company.

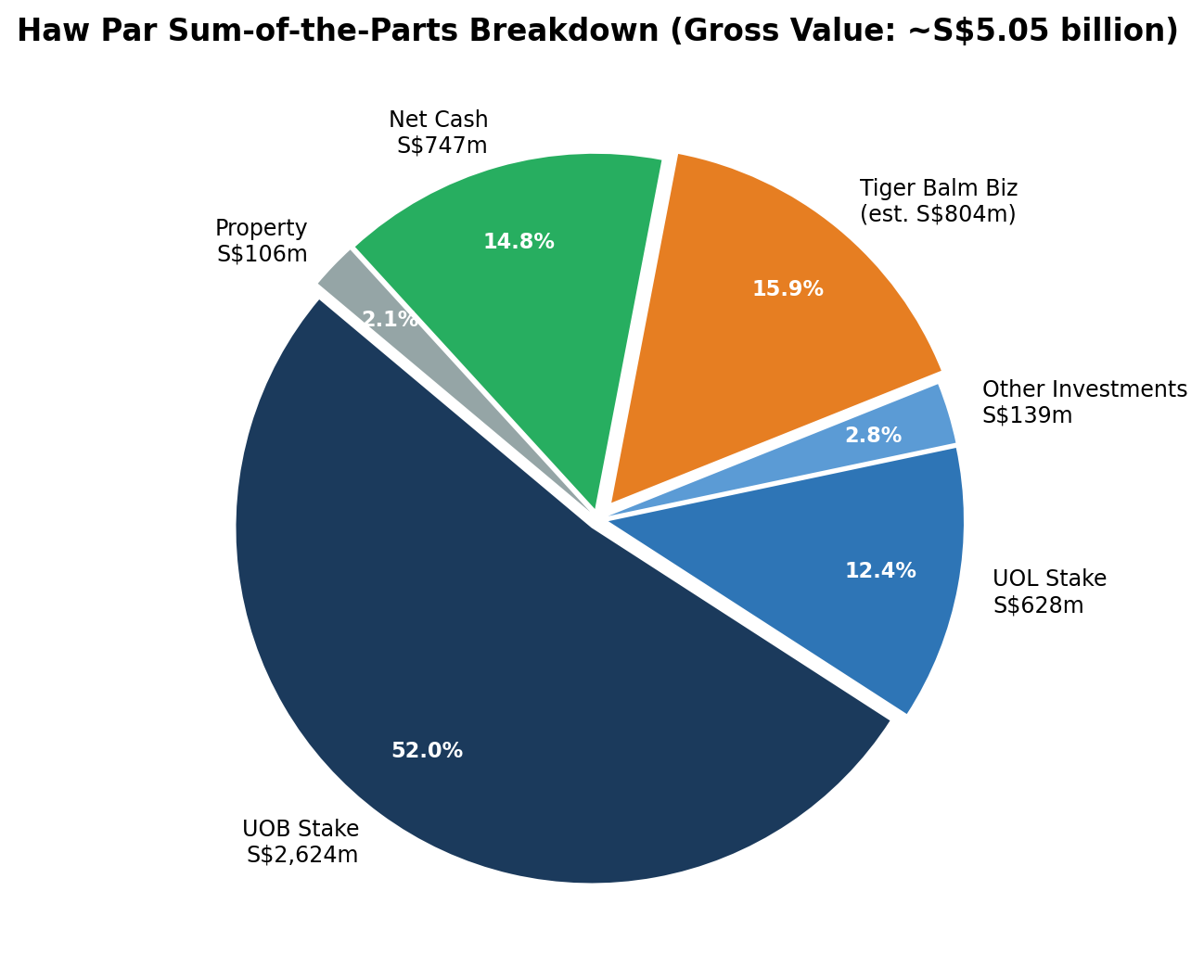

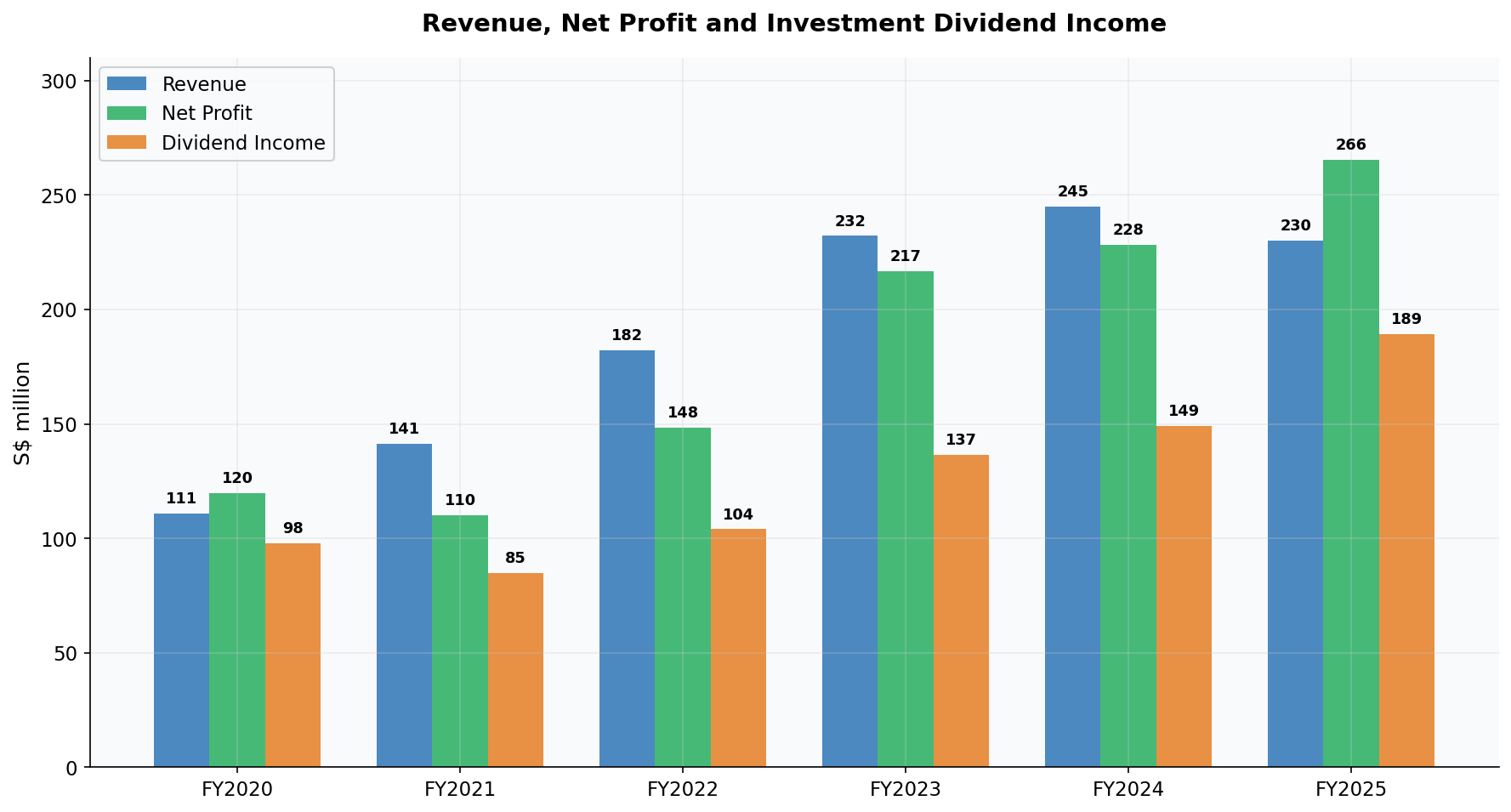

Haw Par Corporation (SGX: H02) is a Singapore-listed conglomerate that owns the globally recognised Tiger Balm brand, sold in over 100 countries. [1] But beneath the familiar red-and-gold packaging sits a S$3.4 billion strategic investment portfolio, primarily stakes in United Overseas Bank (UOB) and UOL Group, plus S$791 million in cash. The healthcare business, while iconic, contributed just 24% of FY2025 group profit.

This piece walks through the numbers, the structure, and the key questions investors should be thinking about.

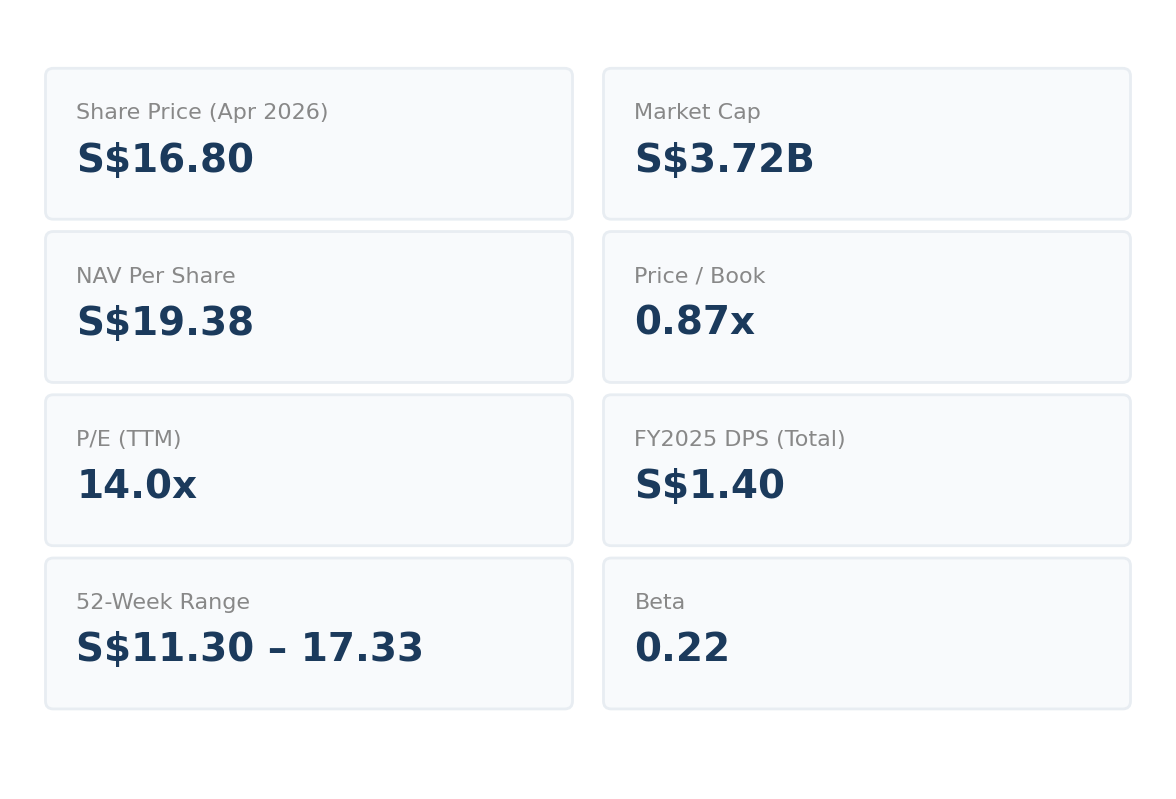

Snapshot

Three Businesses, One Stock

Haw Par reports three segments, and understanding their relative weight is crucial to understanding the stock.

Healthcare (Tiger Balm & Kwan Loong [8]): The consumer-facing brand. FY2025 revenue of S$210 million across over 100 countries, [1] with segment profit of S$67 million and margins of ~32%. This is the business most people think of when they hear “Haw Par.”

Investments: The real engine. Haw Par holds ~74.8 million UOB shares (worth S$2.6 billion) and ~72 million UOL shares (worth S$628 million) [2], plus S$139 million in other investments. In FY2025, this segment generated S$205 million in profit, three times the healthcare business, primarily through S$189 million in dividend income.

Property & Leisure: A smaller segment contributing S$19.6 million in revenue (mostly rental income) and S$10.6 million in profit from industrial and commercial properties.

Financial Performance: Recovering Healthcare, Surging Investment Income

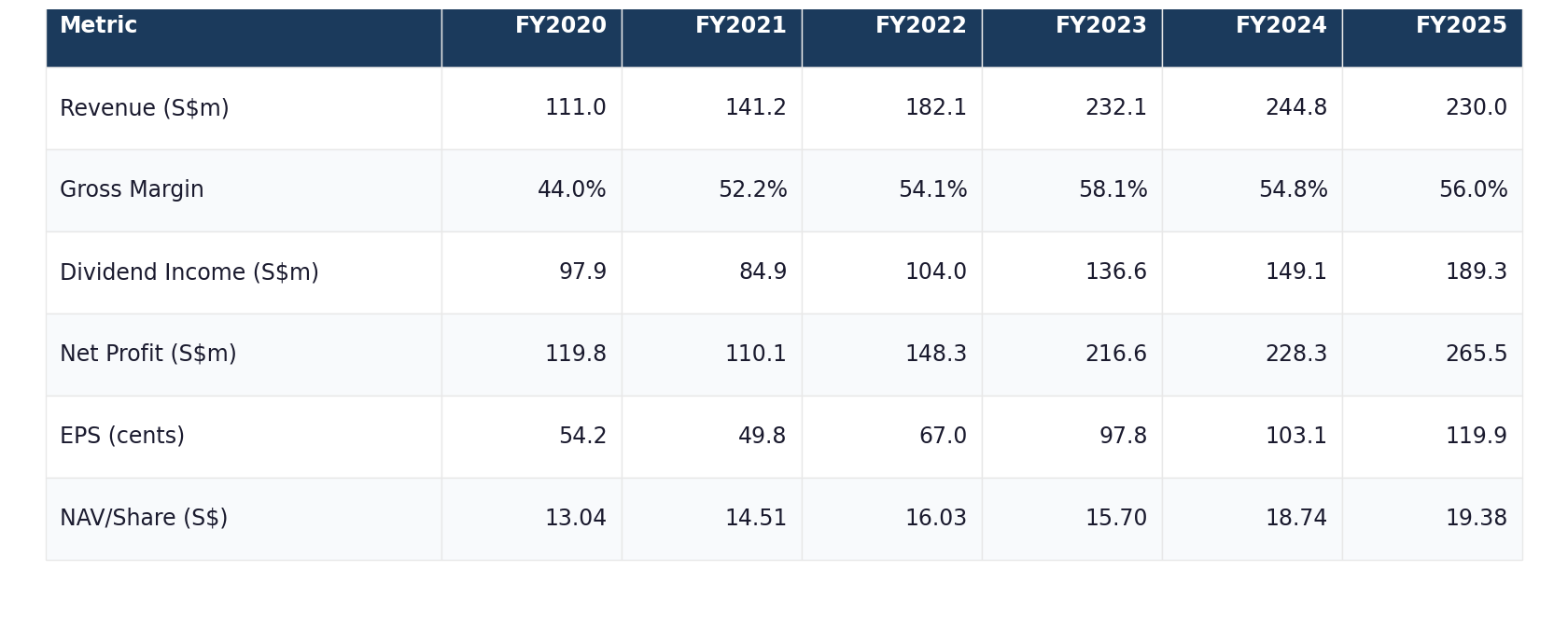

Over the past nine years, Haw Par’s story has been one of recovering healthcare revenue — which fell sharply during COVID (FY2020 revenue was just S$111 million) before rebounding strongly — paired with accelerating investment income. Healthcare revenue has grown at a modest ~2.0% CAGR over the period, but net profit has compounded at ~8.7% annually, driven almost entirely by rising dividend payouts from UOB.

Gross margins have recovered strongly from the COVID-era low of 44% in FY2020, stabilising in the 54–58% range since FY2022, reflecting Tiger Balm’s pricing power. The balance sheet is a fortress: S$791 million cash, S$44 million debt (debt-to-equity of just 1%), and S$4.29 billion in total equity.

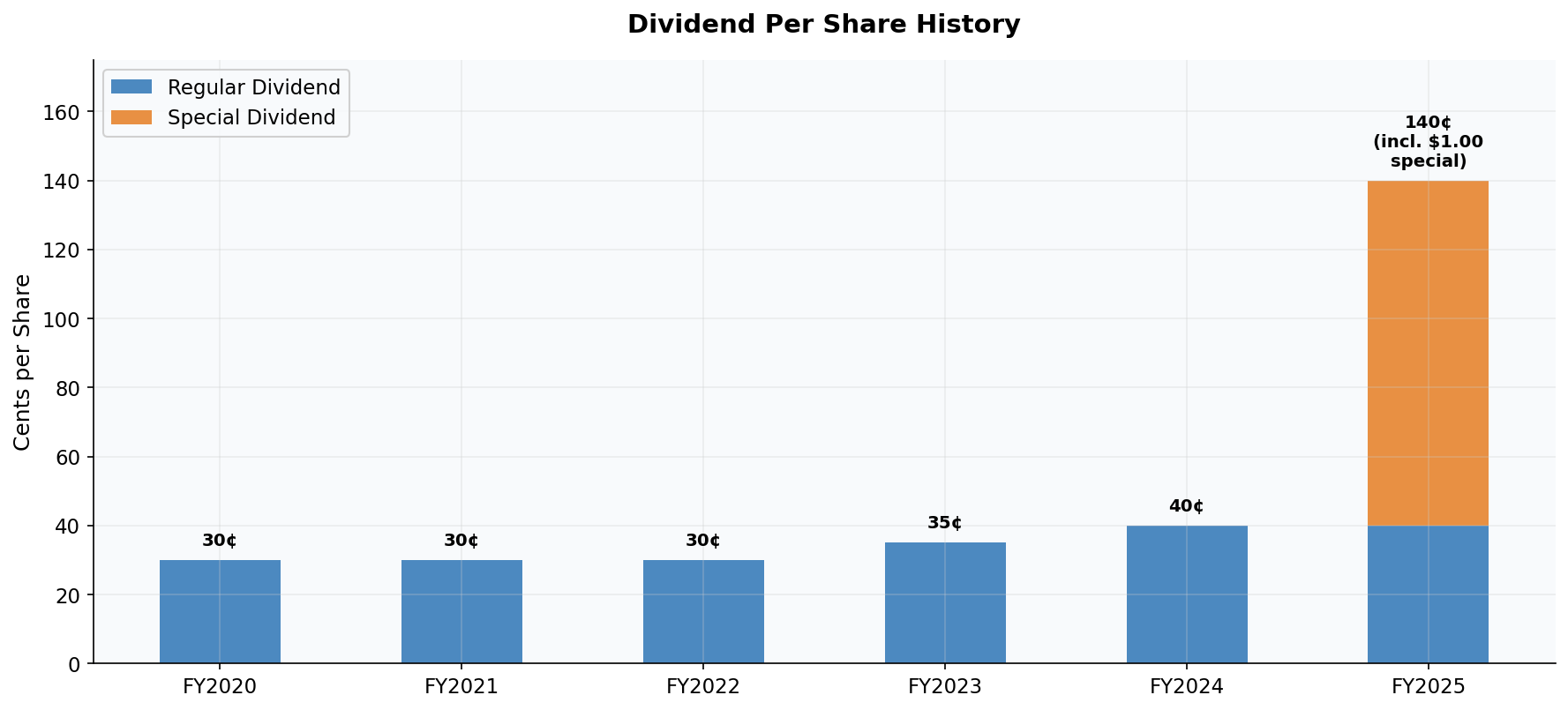

The Dividend Story: A Regime Change?

For years, Haw Par paid a predictable 30 cents per share annually (15 cents interim + 15 cents final). That started to shift in FY2023 with a bump to 35 cents, then 40 cents in FY2024, and FY2025 brought a S$1.00 special dividend on top — bringing total payout to S$1.40 per share, a 250% increase year-on-year.

Where does the dividend money come from?

UOB dividends to Haw Par: ~S$135 million (estimated based on 74.8m shares × S$1.80 regular DPS) [3]

Total investment dividends received: S$189 million

Total dividends Haw Par paid out: S$310 million

UOB alone funds ~44% of the total payout and ~72% of all investment dividend income.

The regular 40-cent dividend is well-covered by UOB income alone. But the S$1.00 special dividend required tapping cash reserves. Whether this becomes a recurring feature is one of the biggest questions for the stock.

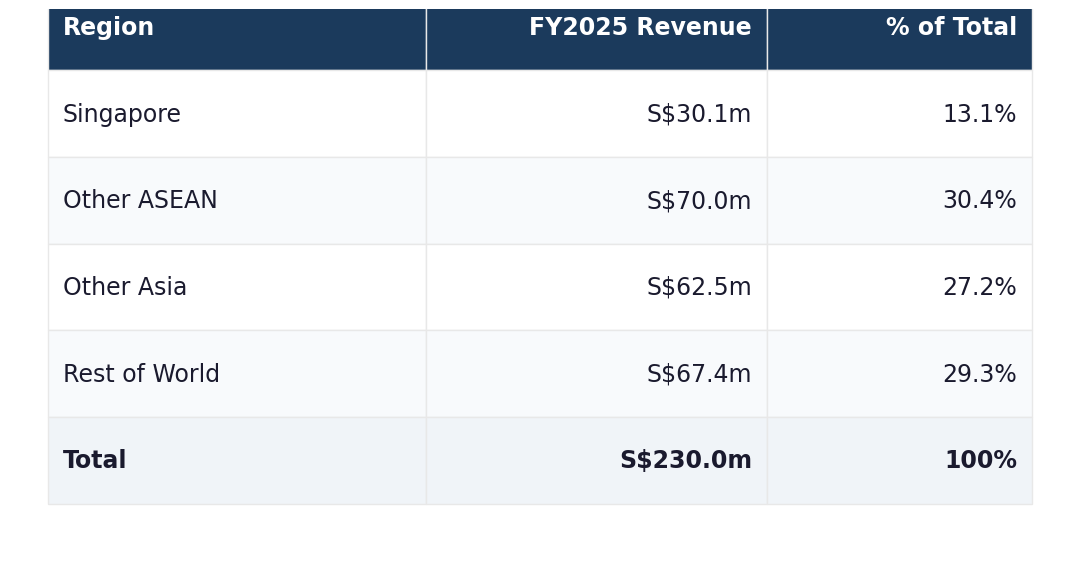

Geographic Revenue Mix

Nearly 30% of revenue now comes from outside Asia, signalling that Tiger Balm’s push into Western markets is gaining traction. The global wellness and natural remedy trend is a meaningful tailwind for the brand.

Sum-of-the-Parts: What Are You Actually Buying?

Given Haw Par’s hybrid nature, a sum-of-the-parts approach is the most useful valuation lens.

At S$16.80, the stock trades roughly in line with the discount-adjusted SOTP of ~S$17.11 — suggesting the recent rally has captured most of the obvious valuation gap. Gross SOTP of S$22.81 implies 36% upside, but the 25% holding company discount (standard for Singapore conglomerates) narrows that considerably.

What Could Go Right

Sustained special dividends — If management commits to returning excess capital regularly, the stock could re-rate as an income vehicle. A sustainable S$1.00+ annual payout would imply a yield of approximately 6%.

Tiger Balm’s international expansion — Western market penetration remains low. Successfully growing the “rest of world” segment at 8–10% annually could lift overall healthcare revenue growth meaningfully.

NAV accretion — If UOB and UOL share prices continue to appreciate, Haw Par’s NAV grows automatically, and dividend income rises in tandem.

Corporate restructuring — Minority shareholder activism at UOI (part of the Wee family holding structure) has pushed for Haw Par share distributions, [7] which could be a catalyst for value-unlocking actions.

What Could Go Wrong

⚠️ Concentration risk: UOB alone represents 59% of Haw Par’s total assets. A significant decline in UOB’s share price or a dividend cut would materially impact NAV and income.

Healthcare stagnation — Tiger Balm revenue declined 6.9% in FY2025. If the brand fails to connect with younger consumers or competition intensifies, the healthcare business could be a drag.

Dividend reversal — The special dividend is not guaranteed. If the company reverts to a regular 40-cent payout without specials, the yield drops to ~2.4% and the income thesis weakens.

Holding company discount persists — The gap between gross SOTP (S$22.81) and market price may never fully close without a structural catalyst. Patient capital is required.

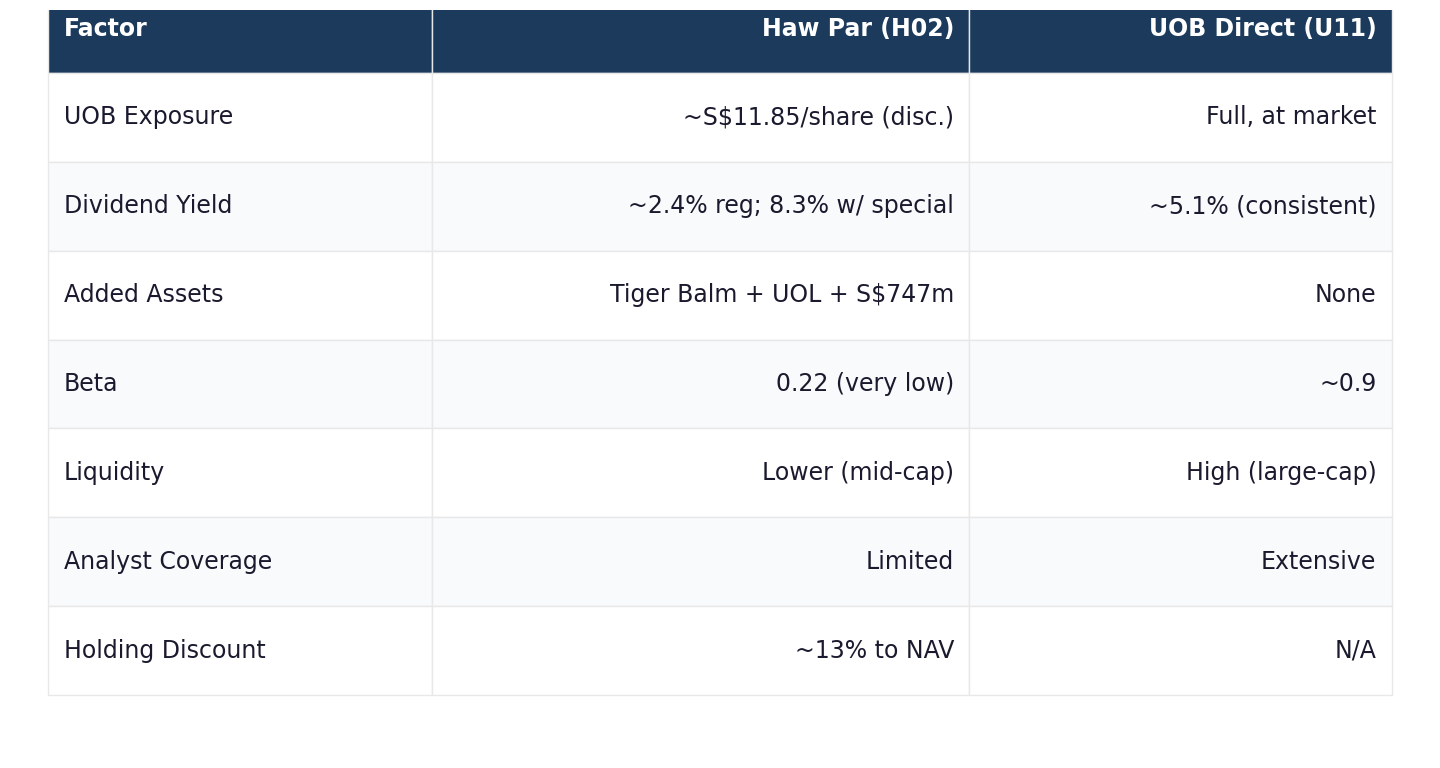

Haw Par vs Buying UOB Directly

A fair question many investors ask: why not just buy UOB? Here’s how the numbers compare.

UOB direct is simpler, more liquid, and offers a cleaner yield. Haw Par offers discounted access to a basket of Singapore blue-chip assets plus a globally recognised consumer brand — but with conglomerate complexity and a structural discount. They suit different investor profiles.

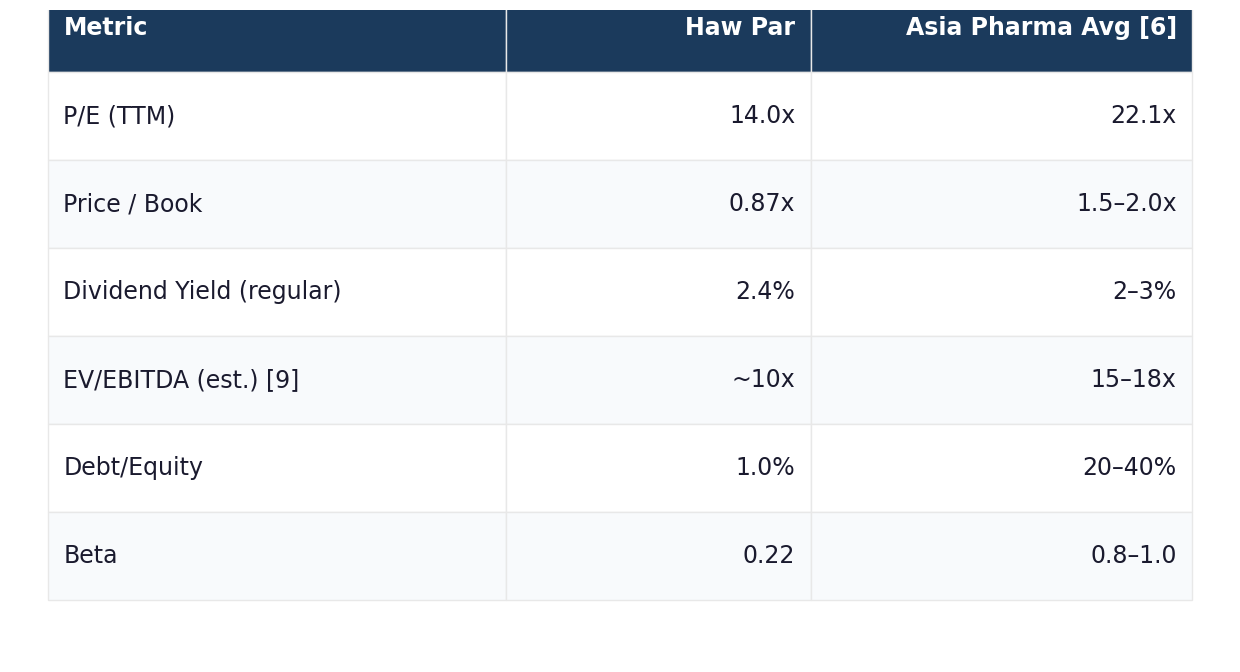

Key Metrics at a Glance

Bottom Line

Haw Par is a unique asset in the SGX universe — part heritage consumer brand, part blue-chip investment vehicle, part cash fortress. The stock offers genuine downside protection (fortress balance sheet, low beta, NAV floor), attractive income potential (if special dividends recur), and a globally recognised brand with international growth runway.

The recent rally from S$11.30 to S$16.80 has captured much of the easy upside, but total return potential remains reasonable for patient, income-oriented investors. The key catalysts to watch are dividend policy evolution, Tiger Balm’s Western market traction, and any corporate restructuring signals from the Wee family holding structure.

Whether this stock suits your portfolio depends on your investment horizon, income needs, and comfort with conglomerate structures. As always, do your own homework before making any investment decisions.

Notes & Sources

Tiger Balm sold in over 100 countries — Per Haw Par Corporation’s corporate website (hawpar.com/healthcare) and the Tiger Balm brand page. Also referenced in the Wikipedia article on Tiger Balm.

Share counts: ~74.8 million UOB shares & ~72 million UOL shares — Exact figures (74,850,539 UOB ordinary shares and 72,044,768 UOL ordinary shares) are disclosed in the Haw Par Corporation Annual Report 2024, available at investor.hawpar.com. Also confirmed in the FY2025 full-year SGX filing.

UOB FY2024 regular DPS of S$1.80 — Per UOB’s FY2024 results announcement via UOB Investor Relations. UOB declared a total ordinary dividend of S$1.80 per share for FY2024 (85 cents interim + 95 cents final). Also reported by The Edge Singapore.

Beta of 0.22 — Sourced from Stock Analysis (SGX: H02), based on 5-year monthly returns vs. the Straits Times Index. Beta values may vary by provider and calculation methodology.

52-week range (S$11.30 – S$17.33) and share price (S$16.80) — Market data sourced from Yahoo Finance (H02.SI) and SGX market data as of early April 2026.

Asia Pharma Average comparisons — Industry average multiples (P/E 22.1x, P/B 1.5–2.0x, etc.) are approximate figures derived from Aswath Damodaran’s sector-level data (pages.stern.nyu.edu/~adamodar) and Bloomberg industry composites for Asia-Pacific healthcare/pharmaceutical companies. These are indicative ranges rather than a single authoritative benchmark.

UOI minority shareholder activism — Reported by The Edge Singapore in multiple articles through 2024–2025, covering minority shareholders’ push for United Overseas Insurance (UOI) to distribute its Haw Par shares. Also discussed on Minichart.com.sg (March 2025).

Kwan Loong as a Haw Par brand — Kwan Loong is manufactured by Haw Par Healthcare and registered with the U.S. FDA (listed on Drugs.com). Also confirmed on Haw Par Corporation’s corporate website (hawpar.com).

EV/EBITDA estimate of ~10x — Author’s estimate. Haw Par does not report EBITDA directly in its SGX filings. This figure is derived by estimating EBITDA from reported operating profit plus depreciation/amortisation, against an enterprise value calculated from market capitalisation plus debt minus cash. Readers should treat this as an approximation.

IMPORTANT DISCLAIMERS

General Disclaimer: This article is published for informational and educational purposes only. It does not constitute financial advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The views expressed are based on publicly available data from Haw Par Corporation’s SGX filings and publicly accessible market data, and may not reflect the most current developments.

Not Licensed Financial Advice: The author is not a licensed financial adviser, and this publication is not issued by a holder of a Capital Markets Services Licence under the Securities and Futures Act 2001 of Singapore. This content does not fall within the definition of “financial advisory service” under the Financial Advisers Act 2001 of Singapore. Readers in Singapore should note that this content is exempt from the requirements of the Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication.

MAS Compliance Notice: In accordance with the Monetary Authority of Singapore’s guidelines, this publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, you should consult a licensed financial adviser who can provide advice tailored to your personal circumstances. Past performance of any security discussed herein is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author may or may not hold positions in the securities discussed. No compensation has been received from any company mentioned in this article.

Data Sources: Haw Par Corporation SGX filings (FY2016–FY2025), public market data from SGX, Yahoo Finance, and Bloomberg as of April 2026.

Hey man, cool stuff!

The SEA Analyst, thanks for your analysis

"Tiger Balm revenue declined 6.9% in FY2025"

Why do you think the revenue declined in FY2025?

Management's explanation is quite generic: weaker consumer sentiment and weaker tourism spending.

I suspect stronger competition and weak performance of new products also contributed to the revenue decline.

I discuss the details here: https://angsanaanderson.substack.com/p/haw-par-right-for-the-wrong-reasons?r=5rl2u5

Thanks