Coliwoo's Asset-Light Pivot Meets a Margin Question

1HFY2026 numbers, the S$218.5m freehold sale, three flip triggers fired, and what the analyst consensus is missing on SGX:W8W.

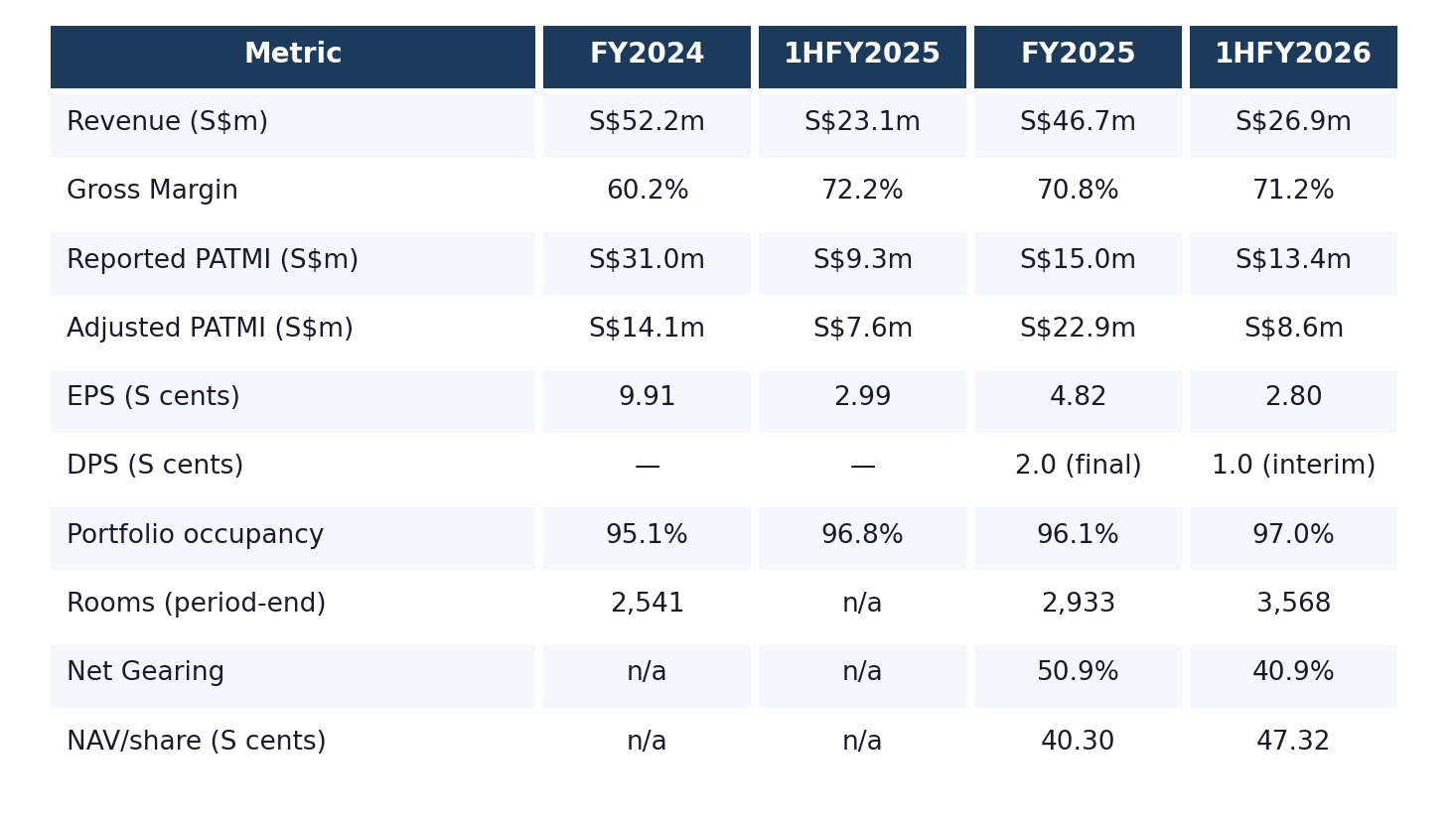

Coliwoo Holdings published its first set of half-year results as a Singapore Exchange-listed company on 6 May 2026, and the headline arithmetic was strong: revenue up 16.6% year-on-year to S$26.9 million, reported net profit attributable to shareholders up 43.9% to S$13.4 million, portfolio occupancy holding at 97.0% across 3,568 rooms, and a first post-listing interim dividend of one Singapore cent per share. The board pre-flagged the better profit on 29 April 2026 with a profit-guidance filing, attributing it primarily to “net fair value gains on the Group’s investment properties.” That hint was important. Strip out the S$5.9 million fair-value swing, the residual S$199k of IPO listing expenses, the small gain on disposal of the Pasir Panjang subsidiary, and the amortisation of an earlier sublease accounting gain, and the adjusted profit number rises 13.9% to S$8.6 million.

That is the figure to anchor on. The reported profit decelerated 51.4% in FY2025 because the FY2024 comparable was inflated by fair-value gains; the same arithmetic now runs in reverse in 1HFY2026. What investors are paying for is the cash-generative operating engine, and that engine grew 13.9%: a real number, and a deceleration from FY2025’s reported 62.6% jump in core profit. That FY2025 figure, though, needs a closer look of its own — we return to it below.

So the first read of these results is a fork. Headline strong, underlying decelerating. Where you stand depends on whether you think the underlying number is depressed by the IPO/listing transition (S$1.2 million of cost still in the bridge) and the early phase of a room-ramp drag, or whether 13.9% is the new run-rate for a business that has now reached the gross-margin ceiling at roughly 71%.

The second thing the results did was reframe the strategy. The press release stated the goal of 10,000 rooms by 2030, the first public articulation of an explicit target, and announced a portfolio sale of seven freehold hospitality and living assets at a combined indicative S$218.5 million. Cushman & Wakefield ran the expression-of-interest exercise, bids closed 13 April 2026, and negotiations are reportedly underway [1][2]. Buyers can take vacant possession or sign a leaseback at a 3.5% gross yield. The properties cluster in three districts: three on River Valley Road, three in Balestier, one at 99 Rangoon Road. Two of the seven currently operate under management contracts rather than full ownership.

The sale is the strategically loaded piece of news in this period. If it executes, Coliwoo monetises roughly half of its S$428.2 million investment-property book and redeploys proceeds into master leases, management contracts, and selective acquisitions where mispricing or repositioning upside is available. Asset-light, capital-efficient, scalable. That model is well-understood. The Assembly Place (SGX:TAP), the only other listed Singapore co-living operator, has always run it. Coliwoo is converging on TAP’s model rather than running parallel to it.