Coliwoo Holdings: Singapore's Co-Living Contender: Growth Compounder or Fairly Priced?

The stock is down 17% since IPO. The fundamentals tell a more nuanced story than either the bulls or bears suggest.

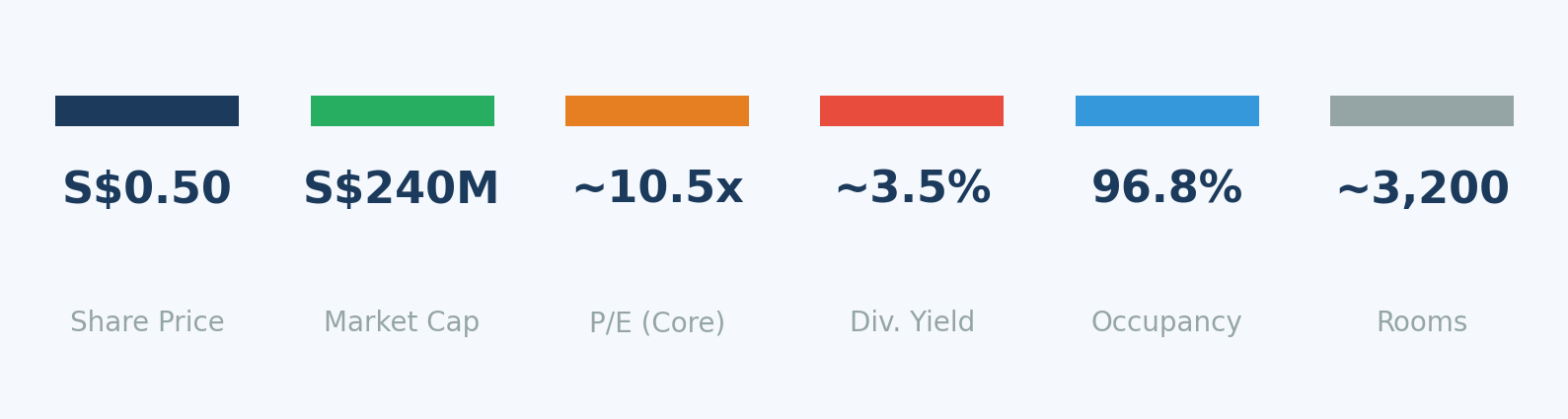

Five months ago, Coliwoo Holdings listed on the SGX Mainboard at S$0.60 per share in an 8.2x oversubscribed IPO. Today, the stock trades around S$0.50. Meanwhile, the company just posted 96.8% occupancy, 70.8% gross margins (on a pre-SFRS(I)16 basis), and grew core PATMI at a 48% CAGR over three years.

The disconnect between operational performance and share price warrants closer examination. This report walks through the full picture.

The Business: How Coliwoo Makes Money

Coliwoo acquires or leases old, underutilised buildings across Singapore, converts them into co-living spaces, and operates them. The business model combines value-add real estate repositioning with a hospitality operations platform. As of the IPO prospectus, the portfolio spanned 25 properties and 2,933 rooms across three tiers. With the completion of the S$101M Changi Business Park acquisition in Q1 FY2026, the portfolio has grown to approximately 3,200 rooms.

Leased properties (~71% of FY2024 revenue, 1,855 rooms at IPO): Coliwoo signs master leases with building owners, pays fixed rent, and captures the spread between rent cost and tenant revenue. The largest single property is 2 Mount Elizabeth Link in Orchard (411 rooms). This is the core of the business — capital-light, scalable, but exposed to lease renewal risk.

Owned properties (~26% of FY2024 revenue, 670 rooms at IPO): Higher capital intensity, better long-term economics. Includes properties across River Valley, Balestier, Beach Road, and Arab Street. Owned property occupancy improved from 73% in FY2022 to 95.5% in 1H2025.

Managed properties (~3% of FY2024 revenue, 408 rooms): Pure fee income. Includes two MOHH contracts for healthcare worker housing and — notably — two properties owned by CEO Kelvin Lim’s personal entities (classified as Interested Person Transactions).

The dual hotel/residential licensing model is worth noting. Some properties hold hotel licenses (allowing 1-night stays), while others operate under residential co-living rules (3-month minimum). This flexibility allows Coliwoo to fill short-stay gaps with tourist traffic during low seasons.

The Numbers: Strong, But Read the Fine Print

*) FY2025 revenue decline partly due to non-recurrence of one-time retrofitting income; owned rental income +23.9%

**) Reported PATMI distorted by fair value swings on investment properties

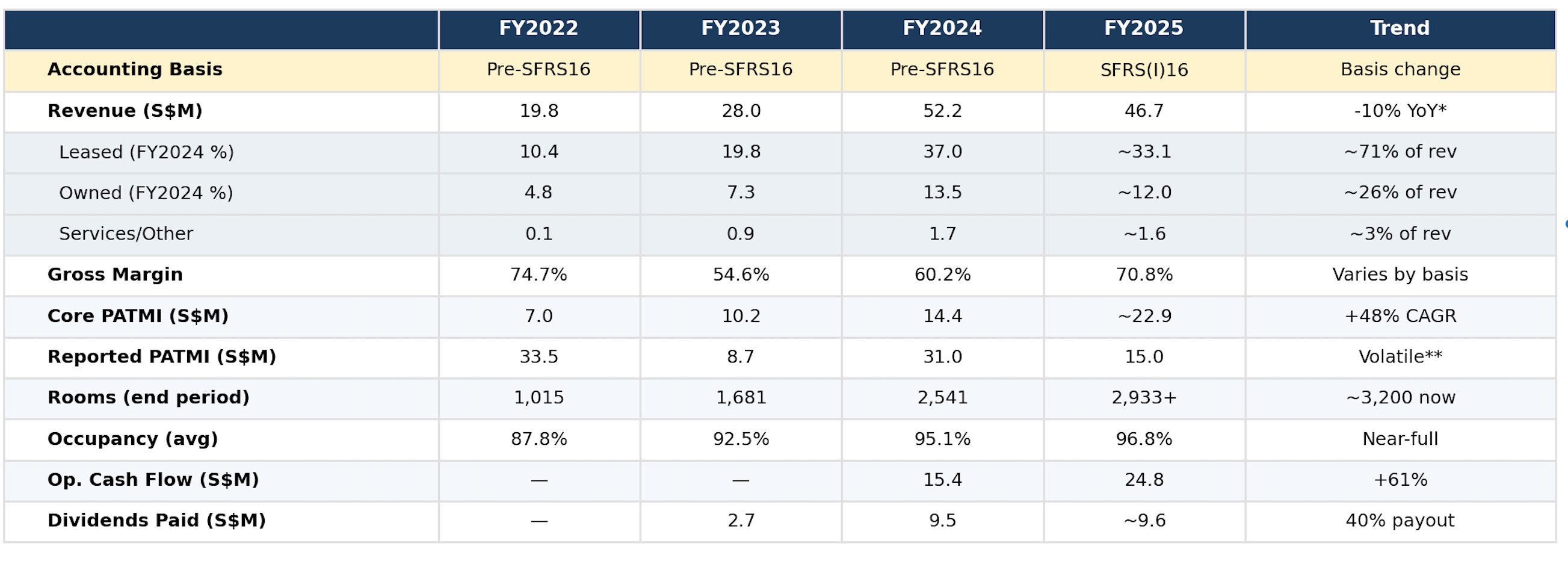

A note on accounting basis: Coliwoo’s prospectus presents FY2022-FY2024 financials on a pre-SFRS(I)16 basis, while the FY2025 annual report uses SFRS(I)16. This matters — SFRS(I)16 capitalises leases, which changes revenue recognition and margin calculations. Revenue figures and margins may not be directly comparable across periods without adjustment.

On a pre-SFRS(I)16 basis (prospectus data), revenue grew from S$19.8M in FY2022 to S$52.2M in FY2024. FY2025 revenue on an SFRS(I)16 basis was S$46.7M, though the decline partly reflects the non-recurrence of one-time retrofitting income — owned rental income actually rose 23.9%.

The metric that matters is core PATMI. Reported net profit is unreliable for Coliwoo because fair value swings on investment properties create wild distortions (S$14.9M gain in FY2024, S$7.4M loss in FY2025). Strip those out, along with IPO costs and share of associate/JV results, and the picture becomes clearer. On this core basis, management reported that FY2025 core PATMI surged 62.6% year-on-year to approximately S$22.9M. The three-year trajectory from S$7.0M (FY2022 adjusted, pre-SFRS(I)16 basis) to S$22.9M represents a 48% CAGR — though comparing across accounting bases requires caution.

Gross margins have been in the 60-75% range on a pre-SFRS(I)16 basis (74.7% in FY2022, 54.6% in FY2023, 60.2% in FY2024) and reached 70.8% in 1H2025. The FY2023 dip reflects the rapid scaling of new leased properties before they reached full occupancy. Operating cash flow jumped from S$15.4M to S$24.8M in FY2025. Working capital dynamics are favourable: tenants prepay (2-4 day receivables), while Coliwoo stretches payables to 19-25 days.

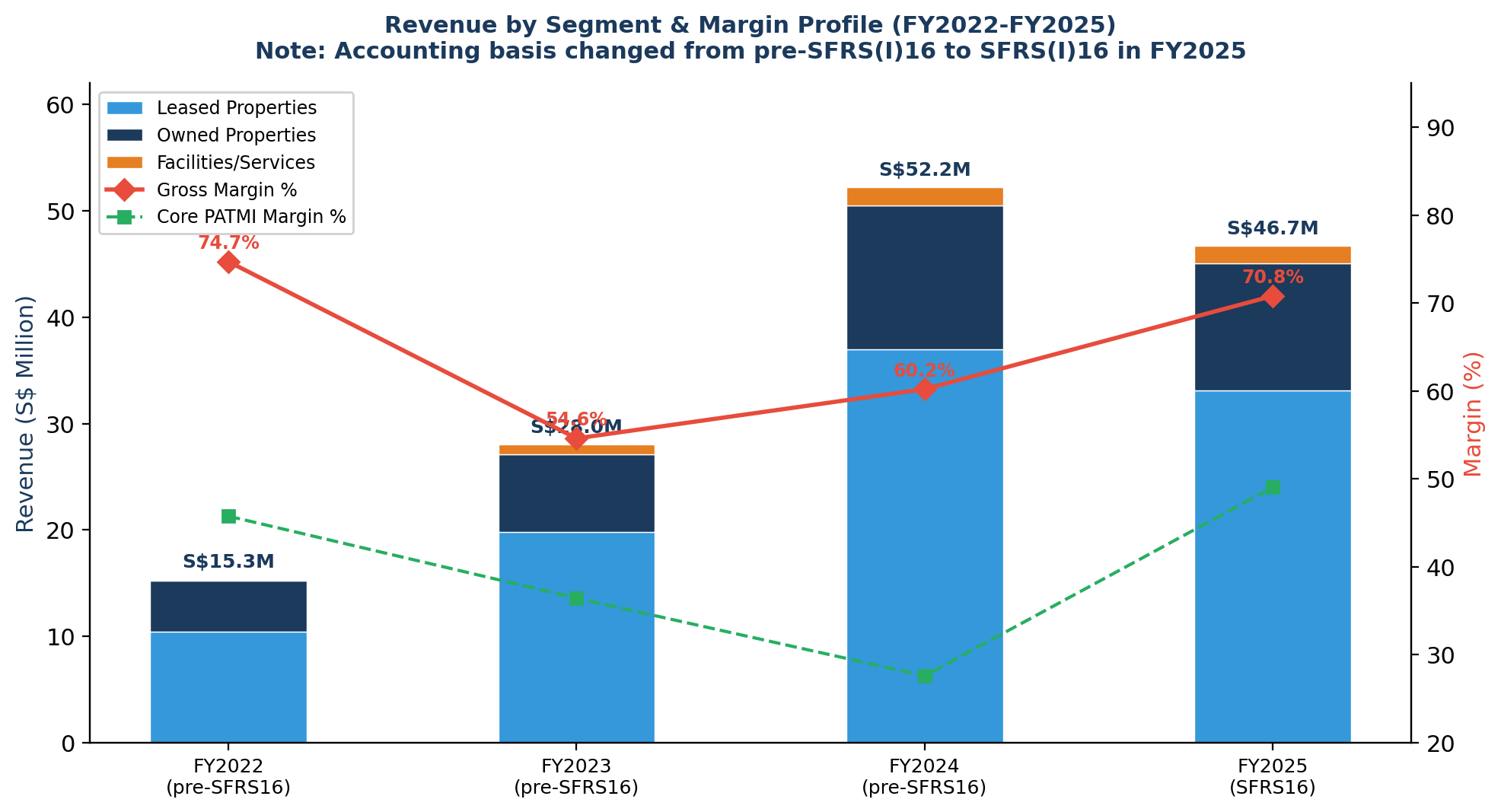

The portfolio composition has shifted over time. Leased properties accounted for roughly 80% of rooms in FY2022 but have declined to about 63% as of the IPO prospectus date, as owned and managed properties grew as a share of the total. Management has diversified away from pure leased concentration — owned properties provide better long-term economics, while managed properties offer capital-light fee income.

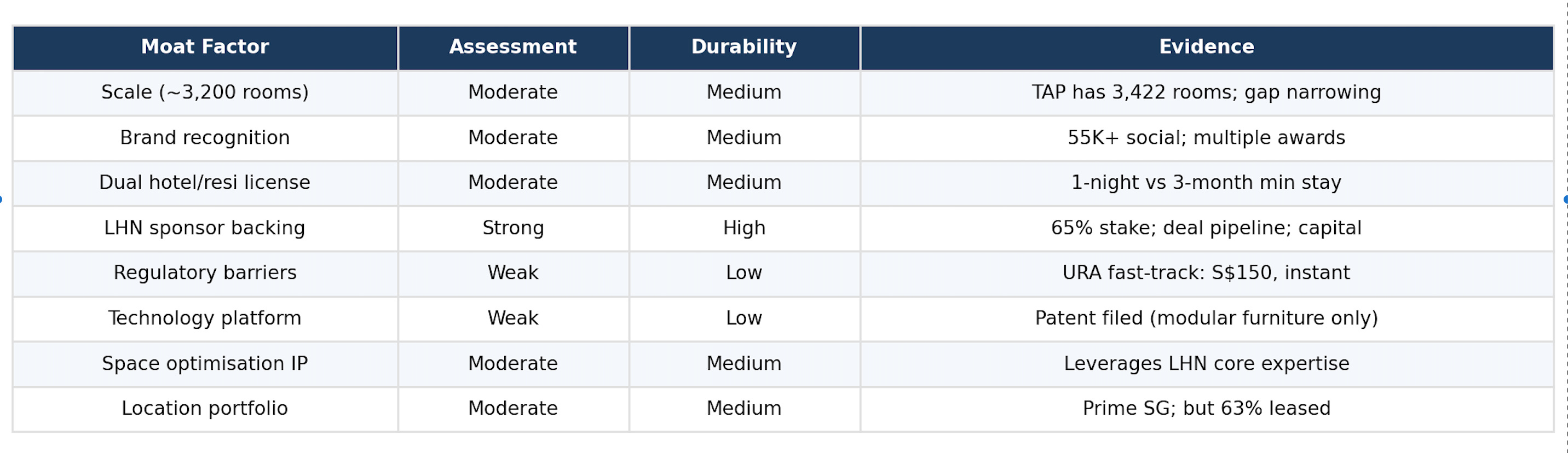

The Moat Question: What’s Defensible?

This is where most analysis of Coliwoo falls short. An honest assessment: the moat is moderate, not structural.

What IS defensible: LHN Group sponsorship is the strongest factor. LHN retains a 65% stake, provides deal pipeline, operational expertise in space optimisation, and balance sheet backing. LHN has delivered strong total shareholder returns (397% over 5 years per one December 2025 report, though an earlier February 2024 measurement put it at 161%). The combination of 25+ properties, established brand (55K+ social media followers, multiple awards), and dual licensing flexibility creates real operational advantages.

What ISN’T defensible: The regulatory moat is almost non-existent. A URA change-of-use approval through the fast-track “deemed authorised” route costs S$150 and can be instant; the standard route costs S$500 and takes about 10 working days. Any operator with capital can enter Singapore’s co-living market. The technology “platform” is operational tooling, not defensible IP.

The competitive reality: The Assembly Place (TAP.SI, listed on Catalist in January 2026) now operates more rooms — 3,422 keys across approximately 100 assets — compared to Coliwoo’s 2,933 at IPO (now approximately 3,200). Habyt has $120M in venture funding. The top 5 operators control 65% of the market, and the sector is consolidating.

Management: What the Record Shows (And Doesn’t)

Kelvin Lim founded Coliwoo in 2018 within LHN Limited, secured a Mainboard listing, and attracted cornerstone investors including Maybank AM, UOB AM, and Value Partners. The execution track record is strong. In seven years, the business grew from zero to over 3,000 rooms.

However, several aspects warrant scrutiny. The prospectus — all 800 pages of it — does not disclose Kelvin Lim’s age, education, or prior career history beyond his role at LHN. That is unusual for a Mainboard listing. He serves as Executive Chairman AND CEO, concentrating significant authority. Two managed properties are owned by his personal entities (Interested Person Transactions, though small at 57 rooms).

The parent company picture is also worth noting. LHN’s ROE is 7.9% — weak for a real estate operator. Consensus expects LHN’s EPS to decline 8.5% in FY2025. Coliwoo contributes 56% of LHN’s 1H2025 pre-tax profit — a substantial dependency. If Coliwoo’s growth slows, LHN’s financials deteriorate, which could reduce the parent’s capacity to support expansion.

Recent capital allocation has been aggressive but strategic: a S$43.9M sale-leaseback (capital recycling), S$40M JV acquisition, and the S$101M Changi Business Park deal. The 40% dividend payout policy balances returns with reinvestment. The question is whether these investments generate returns that justify the capital deployed — something that will only become clear in 12-18 months.

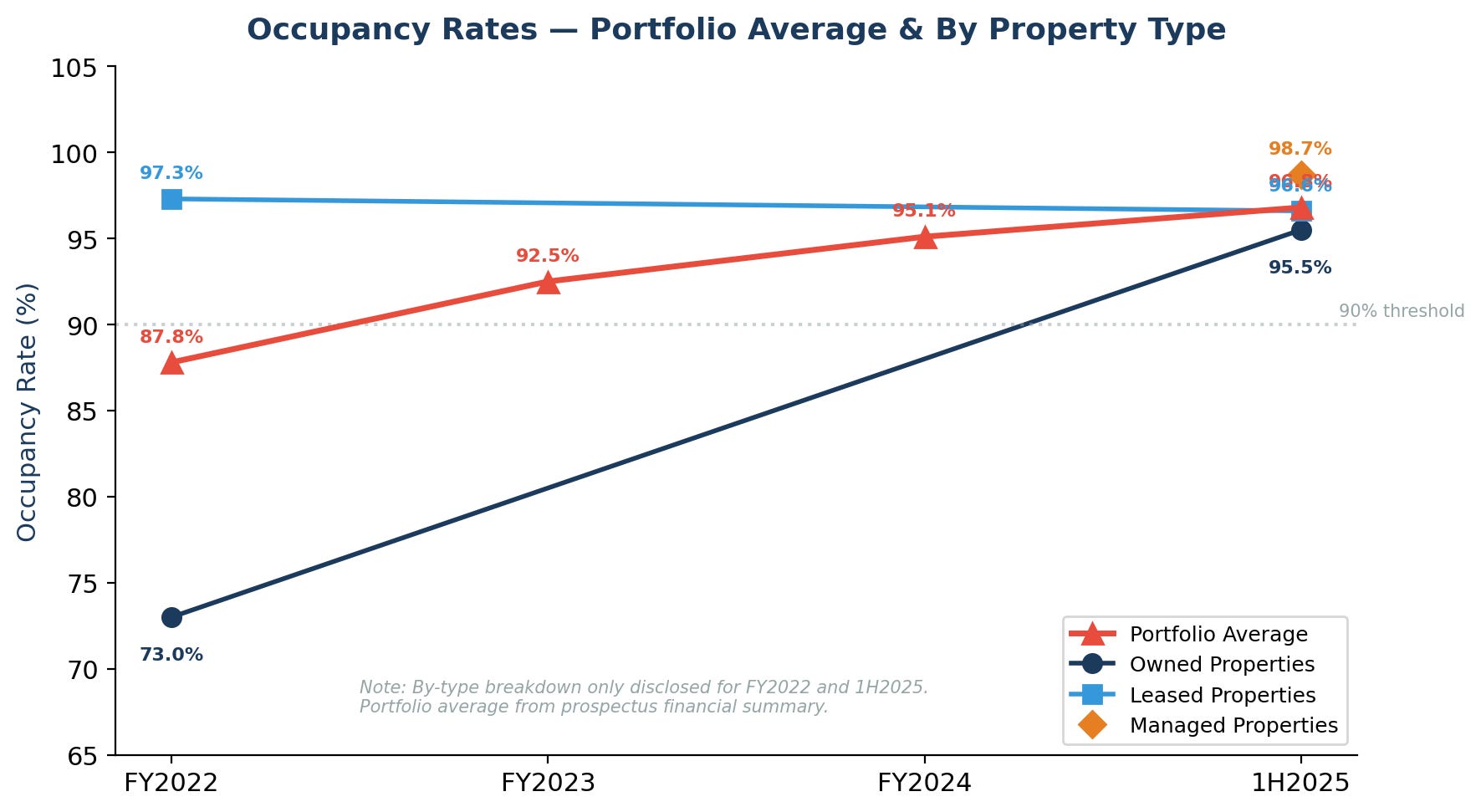

Occupancy: The Headline Number Needs Context

The 96.8% portfolio-level occupancy (as of 1H2025) is strong. The Q1 FY2026 business update reported 96.5% as of January 31, 2026.

Breaking it down by property type, the data available from the prospectus shows: Owned properties improved from 73.0% in FY2022 to 95.5% in 1H2025 — strong execution on a previously underperforming segment. Leased properties were at 97.3% in FY2022 and 96.6% in 1H2025. Managed properties run at 98.7%, largely driven by MOHH healthcare contracts with guaranteed demand. (Note: Intermediate-year occupancy breakdowns by property type are not fully disclosed in the prospectus or annual report.)

The risk is that 96.8% occupancy leaves almost no room for improvement — it can really only go sideways or down. As Coliwoo targets adding 800-1,000 rooms annually, maintaining near-full occupancy during ramp-up periods for new properties will be a challenge worth monitoring.

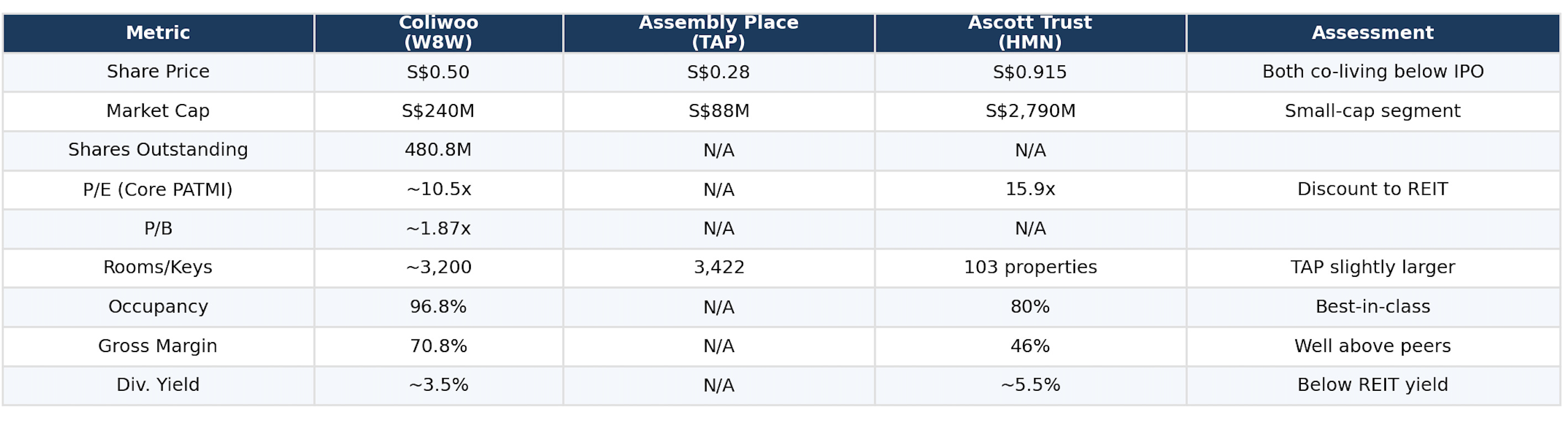

Valuation: Context Matters More Than Headline Multiples

At S$0.50 per share (480.8M shares outstanding):

Market cap: ~S$240M

P/E on FY2025 core PATMI (~S$22.9M): ~10.5x

Price/Book: ~1.87x (equity S$128.1M)

Dividend yield: ~3.5% (based on 40% payout policy)

EV/EBITDA: ~16x

The 10.5x P/E is not obviously cheap for a Singapore-listed small-cap property operator with moderate competitive moats. Both Coliwoo and Assembly Place trade below their IPO prices — the market has repriced co-living sector expectations.

A directional fair value estimate, assuming 20% core PATMI growth for 3 years followed by 10% for 2 years, a terminal growth rate of 3%, and a 10% discount rate, points to approximately S$0.55-0.60 per share. This is a rough estimate, not a rigorous DCF model, and the result is sensitive to growth assumptions. The 10-20% potential upside provides a thin margin of safety, given execution uncertainties.

The January 2026 analyst target of S$0.74 (from a single visible coverage initiation) implies roughly 48% upside from today’s price. With limited analyst coverage and the target predating several months of trading, it should be treated as one data point rather than an anchor.

Key Catalysts to Monitor

Bullish triggers: Changi Business Park occupancy ramp (250+ rooms), FY2026 core PATMI exceeding S$28M (confirming growth trajectory), any concrete regional expansion deal, continued MSCI-driven institutional interest.

Bearish triggers: Occupancy falling below 90%, non-renewal of 2 Mount Elizabeth Link lease (411 rooms = ~13% of expanded portfolio), LHN financial deterioration, or management turnover.

Assessment

Coliwoo is a well-run business in a growing market with real operational strengths. The 96.8% occupancy, strong gross margins, and 48% core PATMI CAGR over three years are notable.

But “good business” and “good investment at this price” are different questions. The moat is moderate, the competitive position is being challenged by The Assembly Place and well-funded private operators, the parent company shows earnings weakness, and the margin of safety at S$0.50 appears thin.

The bull case rests on: the 48% core PATMI CAGR continuing, Changi Business Park ramping successfully, MSCI inclusion driving institutional demand, and LHN’s deal pipeline delivering accretive acquisitions. If FY2026 core PATMI exceeds S$28M, the growth thesis strengthens considerably.

The bear case rests on: moderate moats in a consolidating market, Assembly Place’s larger portfolio, LHN’s declining earnings trajectory, and the risk that near-full occupancy cannot be sustained as the portfolio expands rapidly. Both co-living IPOs trading below issue price suggests the market is pricing in risks the bulls may be underweighting.

The co-living sector in Singapore has structural tailwinds — urbanisation, expatriate demand, housing affordability constraints. The question for Coliwoo specifically is whether operational advantages can compound into durable competitive advantages before well-funded competitors close the gap. The next 12 months will be telling.

Data sources: Coliwoo FY2025 audited annual report (PwC), IPO Prospectus dated 28 October 2025 (registered with MAS), Q1 FY2026 business update, SGX corporate announcements, market data as of April 2026. Financial figures prior to FY2025 are on a pre-SFRS(I)16 basis unless otherwise noted.

IMPORTANT DISCLAIMERS

General Disclaimer: This article is published for informational and educational purposes only. It does not constitute financial advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The views expressed are based on publicly available data from Coliwoo Holdings Ltd’s SGX filings and publicly accessible market data, and may not reflect the most current developments.

Not Licensed Financial Advice: The author is not a licensed financial adviser, and this publication is not issued by a holder of a Capital Markets Services Licence under the Securities and Futures Act 2001 of Singapore. This content does not fall within the definition of “financial advisory service” under the Financial Advisers Act 2001 of Singapore. Readers in Singapore should note that this content is exempt from the requirements of the Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication.

MAS Compliance Notice: In accordance with the Monetary Authority of Singapore’s guidelines, this publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, you should consult a licensed financial adviser who can provide advice tailored to your personal circumstances. Past performance of any security discussed herein is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author may or may not hold positions in the securities discussed. No compensation has been received from any company mentioned in this article.

The SEA Analyst, thanks for highlighting Coliwoo Holdings Limited (W8W; COLIWOO SP)

(1) "The metric that matters is core PATMI. Reported net profit is unreliable for Coliwoo because fair value swings on investment properties create wild distortions"

I think even core PATMI may overstate future recurring profits.

In FY2025, core PATMI reached SGD 23.0 mn. This included SGD 7.4 mn gains from net investment in subleases.

These gains arose because Coliwoo renewed 2 subleases. The new subleases covered the majority of the duration of Coliwoo's master lease with its landlord.

In FY2025, Coliwoo recognised the 'profits' from the subleases upfront.

Investors should note these gains are lumpy and less predictable. They rely on the timing of long-term finance subleases that Coliwoo signs.