Boring Beats Volatile: Why Kimly's 5.1% Yield and New Property Strategy Matter

Fair value for a dividend machine: how Kimly combines 5.1% yield and defensive cash generation with an early-stage property pivot, and why that matters in an economic slowdown.

There’s an old investing adage: the best businesses are often the most boring ones.

If that’s true, Kimly Limited might be one of the best businesses in Singapore. The company operates traditional coffee shops across the island’s heartland estates - the kind of neighbourhood kopitiam where aunties and uncles queue for S$3 mixed vegetable rice at 6am and zi char dinners come in at under S$10 a head. It’s not sexy. It’s not tech. But it throws off cash like a vending machine.

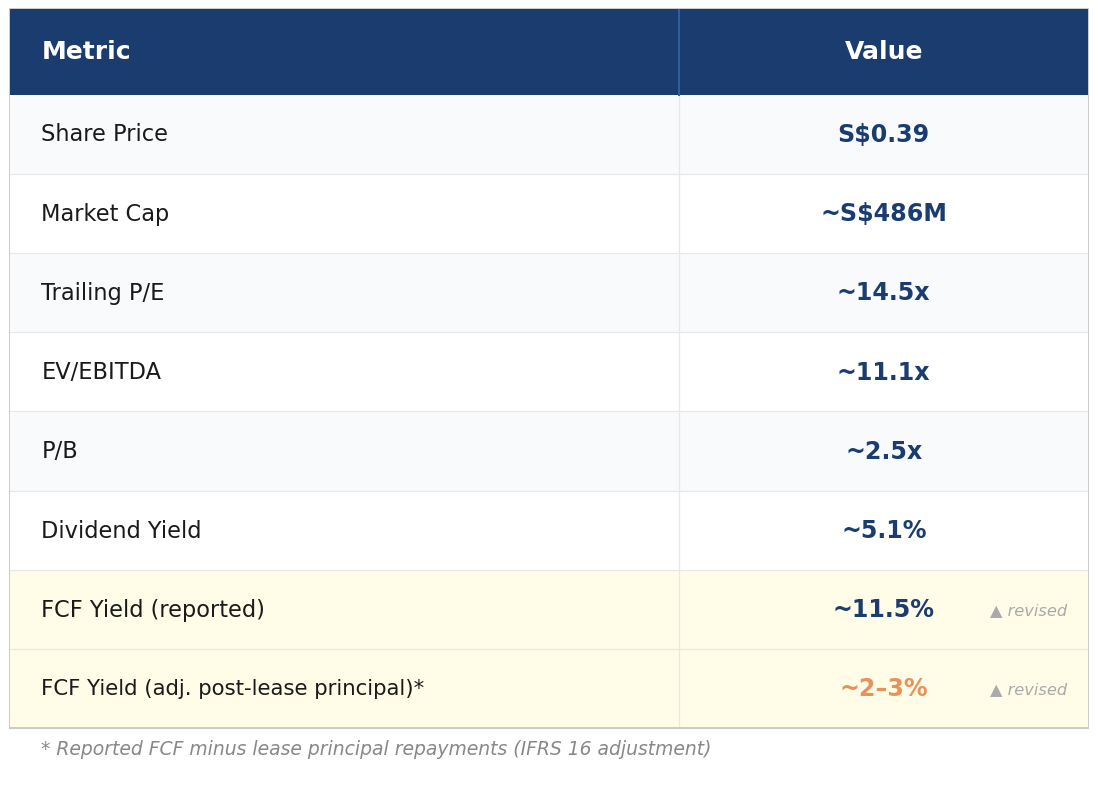

The stock currently trades at roughly S$0.39, giving it a market capitalisation of around S$486 million. It pays a 5.1% dividend yield, generates over S$85 million in annual operating cash flow, and has compounded earnings at a respectable clip since its 2017 IPO. And yet, at ~14.5x trailing earnings, it’s not priced like a compounder.

So the question is: what are you actually paying for, and is it enough?

The Origin Story: From Hawker Heritage to SGX Listing

Kimly’s story begins in the early 1990s, when founder Lim Hee Liat started managing traditional coffee shops in Singapore’s heartland HDB estates. The name “Kimly”, rendered in Chinese as 金味 (jin wei, meaning “golden flavour”), reflects the company’s roots in Singapore’s hawker and kopitiam culture, a culinary tradition so distinctive that it earned UNESCO Intangible Cultural Heritage status in 2020. [1]

For over two decades before its IPO, Kimly quietly built what would become one of the largest kopitiam networks on the island. The model was deceptively simple: lease coffee shop premises (typically from HDB), fit them out, recruit and manage food stall tenants, and operate in-house stalls selling staples like dim sum, mixed vegetable rice, and seafood zi char. By the time of its 2018 annual report, the company described itself as having “more than 25 years of experience” in the trade. [2]

The company listed on the Catalist board of the SGX-ST on 20 March 2017, raising net proceeds of S$43.5 million in its IPO. [3] At that point, Kimly operated 67 food outlets and 129 food stalls across the island, with approximately 40% of stalls open 24 hours. [2]

The IPO proceeds were earmarked for outlet expansion, central kitchen upgrades, and working capital - a disciplined deployment that, as of FY2025, has been substantially completed with S$42.8 million utilised out of S$43.5 million raised. [4]

Two pivotal moves reshaped the company after listing. In July 2018, Kimly acquired the Tonkichi and Rive Gauche businesses from Sapporo Lion, adding Japanese dining and confectionery to its portfolio. [2]

Then, in a far more consequential deal, the company acquired Tenderfresh Group in 2021, gaining a halal-certified central kitchen and a network of quick-service restaurants that opened up the Muslim dining market, roughly 15% of Singapore’s population and a fast-growing regional opportunity. [5]

By FY2025, the network had expanded to 84 food outlets, 5 halal food outlets, 142 food stalls and restaurants, and 53 halal food stalls, restaurants, and kiosks, with an occupancy rate of 97.5% across 638 managed stalls. [4]

In FY2025, the company accelerated a shift from pure operator to landlord-operator, acquiring freehold and leasehold properties to secure strategic long-term locations. While a small property rental division had existed since FY2021, the capital deployment escalated dramatically in FY2025 with S$24.1 million in acquisitions.

The Business: Three Pillars, One Ecosystem

Kimly isn’t just a coffee shop operator. It runs a vertically integrated F&B ecosystem built on three complementary divisions.

Outlet Management (40.8% of FY2025 revenue, S$131.7M) is the engine room. Kimly leases coffee shop premises from HDB or private landlords, fits them out, then sub-leases individual stalls to food hawkers. Think of it as a platform business: Kimly provides the location, infrastructure, cleaning, and management; tenants bring their food and pay rent. As of FY2025, the Group manages 68 traditional coffee shops, four industrial canteens, five Halal outlets under the Kedai Kopi brand, and two food courts. The occupancy rate across 638 stalls sits at 97.5%.

Food Retail (56.8% of revenue, S$182.8M) is where Kimly operates its own food stalls. The portfolio is impressively diverse: 49 Dim Sum stalls, 60 Mixed Vegetable Rice stalls, 28 Zi Char stalls, 3 Teochew Porridge stalls, 2 Tonkichi Japanese restaurants, and the entire Tenderfresh halal food operation (53 outlets). Supporting everything is a central kitchen network that supplies sauces, marinades, and semi-finished products.

Outlet Investment (2.4% of revenue, S$7.7M) is the strategic ace. Kimly buys freehold or long-term leasehold coffee shop properties outright. This eliminates lease renewal risk, locks in prime locations permanently, and generates steady rental yields. In FY2025, Kimly acquired two coffee shop properties for S$24.1 million (excluding prior-year prepayments), with a third acquired shortly after the balance sheet date, and this strategy is accelerating.

Signal from the data: Food Retail revenue actually declined from S$185.0M to S$182.8M in FY2025, even as total revenue grew 0.9%. Growth came entirely from Outlet Management (+S$4.5M) and Outlet Investment (+S$0.4M). For a segment that makes up 57% of revenue, this is worth watching closely.

These three divisions create a self-reinforcing flywheel. The outlet management platform generates traffic and tenant demand. The food retail stalls anchor the outlets with popular, consistent food. And the property acquisitions secure the best locations for the long term. The geographic exposure is entirely Singapore: 89 food outlets (84 under the Kimly/foodclique brands plus 5 halal Kedai Kopi outlets) distributed across the island's heartland estates, with 57 operating 24 hours daily.

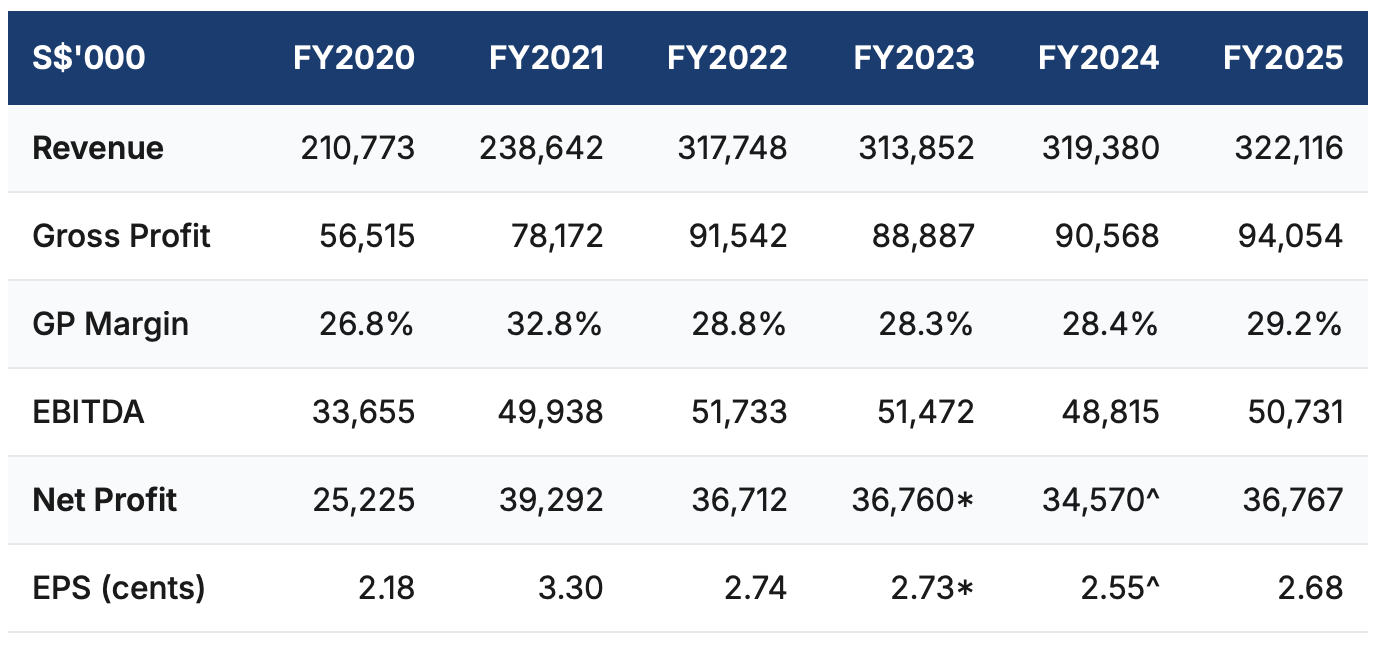

The Numbers: Boring in the Best Way

Kimly has grown revenue from S$202M in FY2018 to S$322M in FY2025, a CAGR of roughly 6.9%. But the honest story is that most of the growth came in one leap: the Tenderfresh acquisition in 2021, which pushed FY2022 revenue from S$239M to S$318M overnight. Since then, growth has been pedestrian at 1-2% annually. This is a mature, Singapore-only business. You’re not buying a growth stock.

* Excluding S$2.5M gain on disposal of Confectionery Business. ^ Excluding S$1.6M corporate income tax rebate. Net Profit figures represent Group Profit after Tax. EPS is calculated on net profit attributable to owners of the Company.

The FY2021 margins were anomalously high, likely reflecting pandemic-era government support measures and cost relief, though the annual report does not break out the exact impact. The normalised picture since FY2022 shows gross margins stabilising in the 28-29% range, with FY2025 ticking up slightly to 29.2%. EBITDA margins sit at 15-16%, and net margins hover around 11%. Margins have held up well despite relentless cost pressures from manpower, raw materials, and utilities.

ROE has trended downward from a peak of 29.5% in FY2021 to 17.3% in FY2025. This looks concerning in isolation, but it's primarily a function of the equity base growing from S$133M (FY2021) to S$192M (FY2025) through retained earnings and the Tenderfresh acquisition. A 17% ROE still comfortably exceeds any reasonable cost of equity for a consumer F&B business.

Where the Cash Goes

This is where Kimly shines - and where the FY2025 story gets interesting. Operating cash flow of S$85.3M on S$322M revenue is a 26.5% cash conversion rate. But the Group deployed over S$30 million on property acquisitions (including capitalised amounts from prior-year prepayments), S$11.4M repaying bank loans, and S$24.9M on dividends. Cash dropped from S$98.5M to S$68.1M. The balance sheet remains healthy (S$192M equity, no net debt beyond lease liabilities), but the aggressive property spending bears watching - it can’t continue at this pace indefinitely without either slowing down or re-levering.

Total dividends have grown from 0.96 cents per share in FY2018 to 2.00 cents in FY2025, with a payout ratio of approximately 75%. At S$0.39, that’s a 5.1% yield: well-covered by free cash flow even in a heavy investment year. The Board has demonstrated a clear commitment to consistent shareholder returns.

The Moat: Wider Than You’d Think

Traditional coffee shops don’t scream “competitive advantage.” But Kimly has built a quietly formidable position through several reinforcing factors.

HIGH DURABILITY: Scale and Network Density. With 89 food outlets and 195 food stalls, Kimly is one of the largest operators in Singapore. This scale provides procurement leverage, brand visibility, and operational efficiencies. Building a comparable network from scratch would take decades.

HIGH DURABILITY: Central Kitchen Infrastructure. The central kitchens supply sauces, marinades, and semi-finished food products across the network, ensuring consistency, reducing per-unit costs, and easing manpower constraints. This infrastructure took years to develop and is difficult to replicate.

MODERATE (IF EXECUTED WELL): Property Ownership Strategy (Early Stage).Owning coffee shop properties would theoretically eliminate lease renewal risk, but this strategy is unproven at Kimly. In FY2025, the company deployed S$24.1 million to acquire Block 204 Serangoon Central and 110 Yishun Ring Road, with a third property (12 Haig Road) acquired post-balance sheet. The durability of this strategy depends on: (i) actual returns on these properties exceeding the cost of capital, (ii) management’s ability to sustain capex without impairing dividends, and (iii) avoidance of overpaying for real estate. Returns data are not yet disclosed. [6]

MODERATE-HIGH: Tenant Loyalty. Decades of reliable management have built trust with food stall tenants. A 97.5% occupancy rate [4] across 638 stalls reflects this. However, the dip from the historical 98%+ benchmark warrants attention.

Worth watching: After years of high occupancy (98%+ per the FY2018 report), the rate dipped to 97.5% in FY2025. That's roughly 10 fewer occupied stalls. Management attributes this to tenant turnover and outlet renovations. If it stabilises or recovers, it's noise. If it trends toward 95%, it signals structural weakening.

MODERATE: Halal Credentials via Tenderfresh. The 2021 acquisition positioned Kimly in the growing Singapore halal market, with a certified Halal central kitchen and 53 outlets. A notable innovation is the “shared kitchen” concept at two Kedai Kopi locations, housing three Tenderfresh brands (380 Nasi Lemak, Pasta Pizza, Tenderbest) under one roof. This optimises kitchen space, reduces staffing needs, and gives customers multiple options at a single outlet. If replicable across more locations, this model could be meaningful.

Overall moat assessment: moderate to wide within Singapore’s traditional coffee shop industry, with the caveat that it’s geographically bounded to a city-state of 5.9 million people.

Growth Drivers and Headwinds

What Could Drive Upside

Network expansion of 3-5 new outlets annually continues. Recent additions include Blk 302 Ubi Avenue 1 (October 2024) and Block 727 Clementi West (July 2025), plus a joint venture at Block 206 Toa Payoh North. Based on the FY2025 Financial Review, 24 new food stalls collectively contributed approximately S$10.9 million in revenue, though per-outlet economics vary widely by location and format.

Halal segment growth is the biggest lever, but needs to prove itself. The Nasi Kari range sold over 20,000 portions since its May 2025 launch. Hawkerman partnered with Chef Eric Low to launch six regional halal dishes. Tenderfresh was invited to host an immersion visit for international delegates at the Singapore Halal International Seminar 2025. These are promising signals, but management’s own description of halal performance as “stable” rather than “growing” tempers expectations.

Property acquisitions represent a strategic shift beginning in FY2025, with S$24.1 million deployed to acquire Block 204 Serangoon Central and 110 Yishun Ring Road. The company’s rationale is to de-risk locations through ownership rather than lease agreements. However, the financial returns on these acquisitions (cap rate, internal rate of return) are not disclosed, and the company has not guided on the pace or scale of future property purchases. This unproven strategy bears close monitoring.

Operational efficiency gains from rotary ovens, self-service ordering kiosks, shared kitchen concepts [4], and central kitchen automation are designed to offset the industry’s structural manpower shortage.

What Could Go Wrong

HIGH RISK: Manpower. Singapore’s tight labour market and restrictive foreign worker policies make F&B hiring exceptionally difficult. Wage inflation is structural and ongoing.

HIGH RISK: Cost pressures. Food ingredients, utilities, and rentals continue rising. Kimly’s positioning as an affordable dining option limits pricing power.

MODERATE RISK: Geographic concentration. Kimly is 100% Singapore. A severe local downturn or policy change would impact the entire business with no offset.

MODERATE RISK: Management transition at Tenderfresh. Changes in Tenderfresh’s senior leadership, with Mr. Chee Kok Chew Gabriel appointed as Executive Officer to oversee the Tenderfresh Group (per the FY2025 annual report, p.8), introduce execution uncertainty around the halal expansion thesis.

Management and Capital Allocation

Kimly’s Board is chaired by Mr. Lau Chin Huat, a Non-Executive Independent Chairman with over 40 years in audit and advisory. The operational team includes veteran managers with 10+ years at the Group. Founder Lim Hee Liat and his concert parties hold approximately 39.9% of shares [8], with total insider ownership around 66-68% [8]. There is no evidence of recent insider selling.

The capital allocation scorecard is solid. IPO proceeds of S$43.5M have been substantially deployed (S$42.8M utilised) [4]. The Tenderfresh acquisition was transformative. Property purchases are strategically sound and funded internally. Four bank loans totalling S$11.4M were fully repaid in FY2025 [6]. And 74-75% of net profit is returned to shareholders through dividends. One latent observation: with 68% insider ownership, a cash-rich balance sheet, and the Koufu privatisation precedent (2022) [9], a take-private scenario is not far-fetched.

Valuation: Fair, Not Cheap

At 14.5x trailing P/E, Kimly trades in the middle of its historical 10-18x range. A simplified DCF using 2-3% revenue growth, 15.5-16% EBITDA margins, and an 8-9% WACC suggests fair value of S$0.42-0.46. Direct peers are limited since Koufu’s delisting, but against the broader Singapore consumer sector (17-20x P/E), Kimly trades at a discount reflecting its small-cap status and single-country exposure.

The FCF yield of 11.5% stands out. If you view Kimly as a cash flow machine with modest growth optionality, the current price arguably under-appreciates the quality of the cash generation. However, the FY2025 property acquisitions warrant scrutiny: the company deployed S$24.1 million while cash reserves fell by S$30.4 million despite positive operating cash flow, suggesting the landlord strategy is in early stages. The actual cap rate and return on these S$24M+ acquisitions are not disclosed. Investors should monitor whether the property pivot becomes accretive to earnings or merely locks up capital in lower-yielding real estate.

On the other hand, the 1-2% top-line growth caps re-rating potential. Without a catalyst to accelerate growth, the stock is likely to remain range-bound, with total returns driven primarily by dividends.

The Bottom Line

Kimly Limited is a high-quality, boring, cash-generative business trading at a fair but not bargain valuation. The investment thesis is simple: a dominant Singapore kopitiam operator with a durable moat, strong cash generation, a 5.1% dividend yield, and an evolving strategy that’s gradually shifting toward asset ownership.

After reviewing the full trail of SGX filings, the thesis is intact but has nuance. Revenue growth is anaemic (sub-1%). Food Retail, the largest segment, is actually shrinking. The Tenderfresh growth narrative needs more evidence. On the other hand, the property acquisition strategy is adding real, tangible value. The shared kitchen concept [4] is a clever operational innovation. And the massive insider ownership provides alignment and a latent privatisation option.

Bull case: Network expands to 95-100 outlets, Tenderfresh scales via shared kitchens, margins improve through automation. Revenue reaches S$360-380M by FY2028 with net profit of S$40-45M. At 16-18x P/E: S$0.51-0.65 (30-67% upside plus cumulative dividends).

Base case: Steady 1-2% growth, margins hold, dividends maintained at 2.0 cents. At 14-16x P/E: S$0.41-0.51 (5-30% upside plus 5.1% annual yield).

Bear case: Cost pressures compress earnings to S$28-30M, dividend cut to 1.5 cents. At 10-12x P/E: S$0.23-0.29 (25-40% downside).

This is not a multi-bagger candidate. The realistic total return profile is 7-12% annually (5.1% dividend plus 2-7% capital appreciation), which is attractive for a defensive, income-oriented position with a hard asset floor. For value investors who appreciate consistent cash flows, owner-operator mentality, and getting paid to wait, Kimly merits a closer look. The downside is cushioned by tangible assets and a resilient business model. The upside is capped by modest growth but sweetened by yield and optionality.

Revision History

4 May 2026 — Reader corrections incorporated

Two substantive corrections were made following reader comments. Both affect how Kimly’s cash generation should be interpreted, and neither changes the core thesis, but both matter for intellectual honesty.

1. IFRS 16 and true FCF (Cash Flow section)

The original article presented operating cash flow of S$85.3M and FCF of S$56M without flagging the IFRS 16 lease accounting effect. Under IFRS 16, when Kimly signs a new lease the ROU asset and lease liability are recognised simultaneously with no cash changing hands at inception. Lease principal repayments flow through financing cash flows, not operating cash flows, meaning reported OCF is higher than it would be under pre-IFRS 16 treatment where all rent sat as an operating expense.

2. FCF yield overstated (Valuation section)

The original article cited an FCF yield of ~11.5% as a valuation argument. A reader correctly pointed out that this figure does not account for lease principal repayments, which are a real and recurring cash obligation for a lease-heavy operator like Kimly. Once adjusted, the true FCF yield falls to approximately 2–3% in FY2025. The valuation table has been updated accordingly. The underlying investment case that is anchored on dividend sustainability (5.1% yield, well-covered by earnings) and the property acquisition strategy remains unchanged.

References

All factual claims in this article are sourced from the following publicly available documents filed with the Singapore Exchange (SGX) or published by the company:

[1] UNESCO, “Hawker culture in Singapore, community dining and culinary practices in a multicultural urban context,” Intangible Cultural Heritage, inscribed 2020.

[2] Kimly Limited, Annual Report 2018, “Corporate Profile” and “Message to Shareholders,” pp. 1-7.

[3] Kimly Limited, Annual Report 2018, Catalist listing date: 20 March 2017, p. 1.

[4] Kimly Limited, Annual Report 2025, “Corporate Profile,” “Our Businesses,” and “Message to Shareholders,” pp. 1-8.

[5] Kimly Limited, Annual Report 2021 and subsequent reports, Tenderfresh acquisition details.

[6] Kimly Limited, Annual Report 2025, “Financial Review” and “Financial Highlights,” pp. 19-24.

[7] Kimly Limited, Annual Report 2025, “Message to Shareholders — Rewarding Shareholders,” p. 8.

[8] Kimly Limited, SGX filings, substantial shareholder notifications and annual report disclosures (FY2024-FY2025).

[9] “Koufu Group announces privatisation offer at S$0.790 per share,” SGX announcement, 2022.

IMPORTANT DISCLAIMERS

General Disclaimer: This article is published for informational and educational purposes only. It does not constitute financial advice, a recommendation, or a solicitation to buy, sell, or hold any securities. The views expressed are based on publicly available data from Kimly Limited’s SGX filings and publicly accessible market data, and may not reflect the most current developments.

Not Licensed Financial Advice: The author is not a licensed financial adviser, and this publication is not issued by a holder of a Capital Markets Services Licence under the Securities and Futures Act 2001 of Singapore. This content does not fall within the definition of “financial advisory service” under the Financial Advisers Act 2001 of Singapore. Readers in Singapore should note that this content is exempt from the requirements of the Financial Advisers Act pursuant to Regulation 34 of the Financial Advisers Regulations, as it is published in a generally available publication.

MAS Compliance Notice: In accordance with the Monetary Authority of Singapore’s guidelines, this publication does not take into account the specific investment objectives, financial situation, or particular needs of any individual. Before making any investment decision, you should consult a licensed financial adviser who can provide advice tailored to your personal circumstances. Past performance of any security discussed herein is not indicative of future results.

No Warranty: While the data and analysis have been prepared in good faith from public sources believed to be reliable, no representation or warranty, express or implied, is made as to the accuracy, completeness, or timeliness of the information. The author accepts no liability for any loss arising from the use of this material.

Disclosure: The author may or may not hold positions in the securities discussed. No compensation has been received from any company mentioned in this article.

Data Sources: Kimly Limited SGX filings, public market data from SGX, Yahoo Finance, and Bloomberg as of April 2026.

(2) The reported 11.5% FCF yield overstates Kimly’s true cash generation.

11.5% is calculated from SGD 55 mn of FCF.

But additions to right-of-use (ROU) assets have not been deducted from SGD 55 mn.

For a lease-heavy operator like Kimly, those ROU additions are capex and should be deducted from operating cash flow when estimating FCF.

Additions to ROU represent the cost of acquiring operating rights over coffee shop sites.

However, the cash flow statement fails to show them as capex because it is immediately offset by financing inflow from lease liabilities.

"A lease is an investing transaction, where a company buys a fixed asset, and a financing transaction, where the company raises debt.”

Once the adjustment is made, true FCF yield likely falls to ~2% in FY2025.

The SEA Analyst,

(1) What is your assessment of management?

Some time ago, I was also interested in Kimly Limited (1D0; KMLY SP).

But I passed after this news: "Ex-chairman, director of coffee shop chain Kimly fined for not disclosing stake in acquisition of company" [1]

DPP Suhas Malhotra said the case involves "an intentional and blatant refusal to comply with the disclosure obligations which apply to all publicly listed companies in Singapore".

On Lim's conduct, Mr Malhotra said this was "an unabashed choice by Lim to not disclose his interest in ASC, in contravention of the law".

"That the executive chairman of a public company can treat his company's obligations in such a cavalier manner is troubling, to say the least," he said.

[1] https://www.channelnewsasia.com/singapore/kimly-ex-chairman-director-fined-not-disclosing-stake-coffee-shop-chain-2501866